Advertisement

- United States

- /

- Electrical

- /

- NasdaqGS:POWL

Powell Industries, Inc. Just Missed Earnings And Its EPS Looked Sad - But Analysts Have Updated Their Models

Powell Industries, Inc. (NASDAQ:POWL) shares fell 5.2% to US$39.13 in the week since its latest quarterly results. Statutory earnings per share fell badly short of expectations, coming in at US$0.24, some 23% below analyst forecasts, although revenues were okay, approximately in line with analyst estimates at US$134m. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether analysts have changed their mind on Powell Industries after the latest results.

Check out our latest analysis for Powell Industries

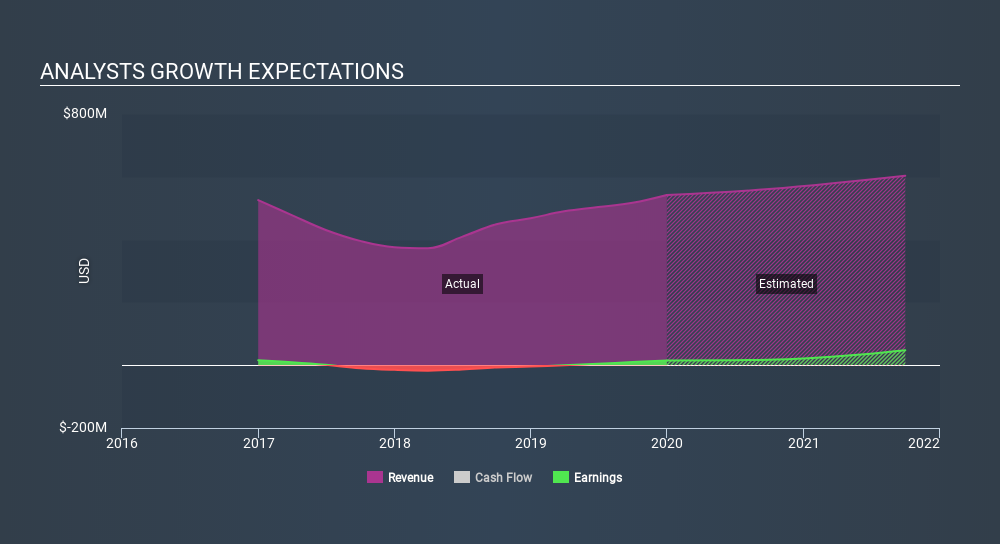

After the latest results, the two analysts covering Powell Industries are now predicting revenues of US$560.8m in 2020. If met, this would reflect a reasonable 3.5% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to ascend 12% to US$1.48. Before this earnings report, analysts had been forecasting revenues of US$587.4m and earnings per share (EPS) of US$1.82 in 2020. Analysts seem less optimistic after the recent results, reducing their sales forecasts and making a substantial drop in earnings per share forecasts.

Analysts made no major changes to their price target of US$46.00, suggesting the downgrades are not expected to have a long-term impact on Powell Industries's valuation.

In addition, we can look to Powell Industries's past performance and see whether business is expected to improve, and if the company is expected to perform better than wider market. For example, we noticed that Powell Industries's rate of growth is expected to accelerate meaningfully, with revenues forecast to grow at 3.5%, well above its historical decline of 8.2% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the market are forecast to see their revenue grow 2.7% per year. Although Powell Industries's revenues are expected to improve, it seems that analysts are also expecting it to grow faster than the wider market.

The Bottom Line

The biggest concern with the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Powell Industries. Unfortunately analysts also downgraded their revenue estimates, although industry data suggests that Powell Industries's revenues are expected to grow faster than the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for Powell Industries going out as far as 2021, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:POWL

Powell Industries

Designs, develops, manufactures, sells, and services custom-engineered equipment and systems.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor