- United States

- /

- Aerospace & Defense

- /

- NasdaqGS:KTOS

Kratos Defense & Security Solutions (KTOS): Valuation Check After New Analyst Coverage and Expansion Moves

Reviewed by Simply Wall St

Kratos Defense & Security Solutions (KTOS) is back in the spotlight after fresh analyst coverage and a string of new facilities, moves that together sharpen the market’s focus on its long term growth runway.

See our latest analysis for Kratos Defense & Security Solutions.

Those new facilities and upbeat coverage are landing against a backdrop where the $71.4 share price has cooled from recent highs, with a negative 90 day share price return but an eye catching three year total shareholder return above 650 percent. This suggests that momentum has paused rather than broken.

If these moves in defense tech have your attention, it could be a good moment to scan other potential winners across aerospace and defense stocks and see what else fits your strategy.

With analysts lifting targets well above the current price and with Kratos still posting rapid revenue and earnings growth, the question now is whether this recent pullback offers a fresh buying window or if markets already reflect that future upside.

Most Popular Narrative: 29% Undervalued

With Kratos last closing at $71.40 against a narrative fair value a little above $100, the valuation debate is firmly back on center stage.

Strategic wins on generational programs (e.g., Poseidon, MACH-TB, Prometheus, GEK), ongoing facility expansions, and deepening partnerships with primes and government agencies are creating a strong multi-year visibility into revenue and cash flow growth. As these large-scale awards transition into full-rate production, Kratos is set to leverage operational scale for improved net margin, increasing the company's earnings power and long-term intrinsic value.

Want to see how this ambitious roadmap turns into a triple digit fair value? The analysis focuses on earnings projections and a profit margin reset. Curious which long term cash flow assumptions make that possible? Dive into the full narrative to see the detailed framework behind this view.

Result: Fair Value of $100.56 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this optimistic path could be derailed if big-ticket defense programs slip, or if heavy upfront investment squeezes margins and delays meaningful cash generation.

Find out about the key risks to this Kratos Defense & Security Solutions narrative.

Another Angle on Valuation

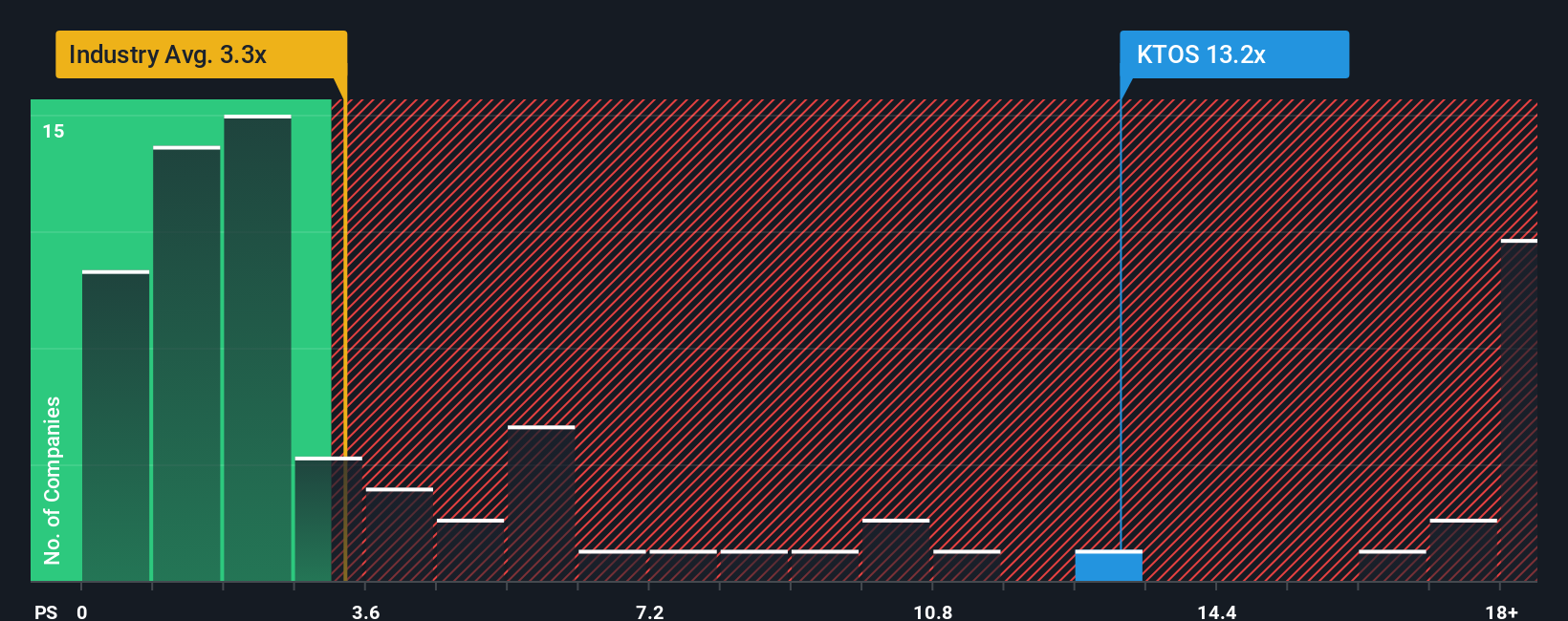

Look past the narrative fair value and the picture gets trickier. On sales, Kratos trades at about 9.4 times revenue, versus roughly 3 times for the wider US defense sector and a fair ratio near 2.6. That rich gap signals real execution risk if growth ever cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Kratos Defense & Security Solutions Narrative

If you see things differently or want to dig into the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your Kratos Defense & Security Solutions research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

Before you move on, line up your next opportunities with targeted stock ideas from the Simply Wall Street Screener, so potential winners do not slip past you.

- Capitalize on mispriced opportunities by scanning these 916 undervalued stocks based on cash flows that pair strong cash flows with attractive entry points.

- Explore the next wave of intelligent automation by targeting these 24 AI penny stocks positioned at the heart of AI innovation.

- Assess potential income streams by reviewing these 13 dividend stocks with yields > 3% that combine dividend payments with underlying business fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kratos Defense & Security Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:KTOS

Kratos Defense & Security Solutions

A technology company, provides technology, products, and system and software for the defense, national security, and commercial markets in the United States, other North America, the Asia Pacific, the Middle East, Europe, and Internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion