Advertisement

- United States

- /

- Industrials

- /

- NasdaqGS:HON

Is Honeywell International a Bargain After Clean Energy Expansion Headlines?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Honeywell International is trading at a fair price? You are not alone, as plenty of investors are closely watching its valuation story unfold.

- Honeywell’s stock has seen some ups and downs lately, finishing flat over the past week, down 3.4% this month, and losing 13.1% so far this year. This might indicate shifting market expectations and changes in risk appetite.

- Several recent analyst upgrades and growing discussion of industrial automation trends have attracted increased investor interest. In addition, headlines about Honeywell’s planned expansion into clean energy and smart building solutions are helping shape the narrative around long-term opportunity.

- When it comes to valuation, Honeywell receives a score of 4 out of 6 based on key metrics. However, understanding value goes far beyond a single number. Let’s explore the different ways Honeywell’s price can be assessed, and an even more complete perspective will be provided at the end of this article.

Find out why Honeywell International's -7.1% return over the last year is lagging behind its peers.

Approach 1: Honeywell International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and then discounting them to their present value. This enables investors to assess whether the current stock price reflects the true worth of the business.

Honeywell International generated Free Cash Flow of $6.29 Billion over the last twelve months. Analyst estimates anticipate gradual growth, with Free Cash Flow projected to reach $6.84 Billion by 2028. Typically, analysts provide outlooks for up to five years. Additional years used in the calculation are extrapolated by Simply Wall St, extending the forecast to ten years. These extended projections show Honeywell’s Free Cash Flow continuing to increase, providing confidence in the company’s long-term earning ability.

Based on this two-stage DCF approach, Honeywell’s intrinsic value per share is calculated at $221.03. This is roughly 11.3% above the current market price, suggesting the stock is undervalued according to this method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Honeywell International is undervalued by 11.3%. Track this in your watchlist or portfolio, or discover 894 more undervalued stocks based on cash flows.

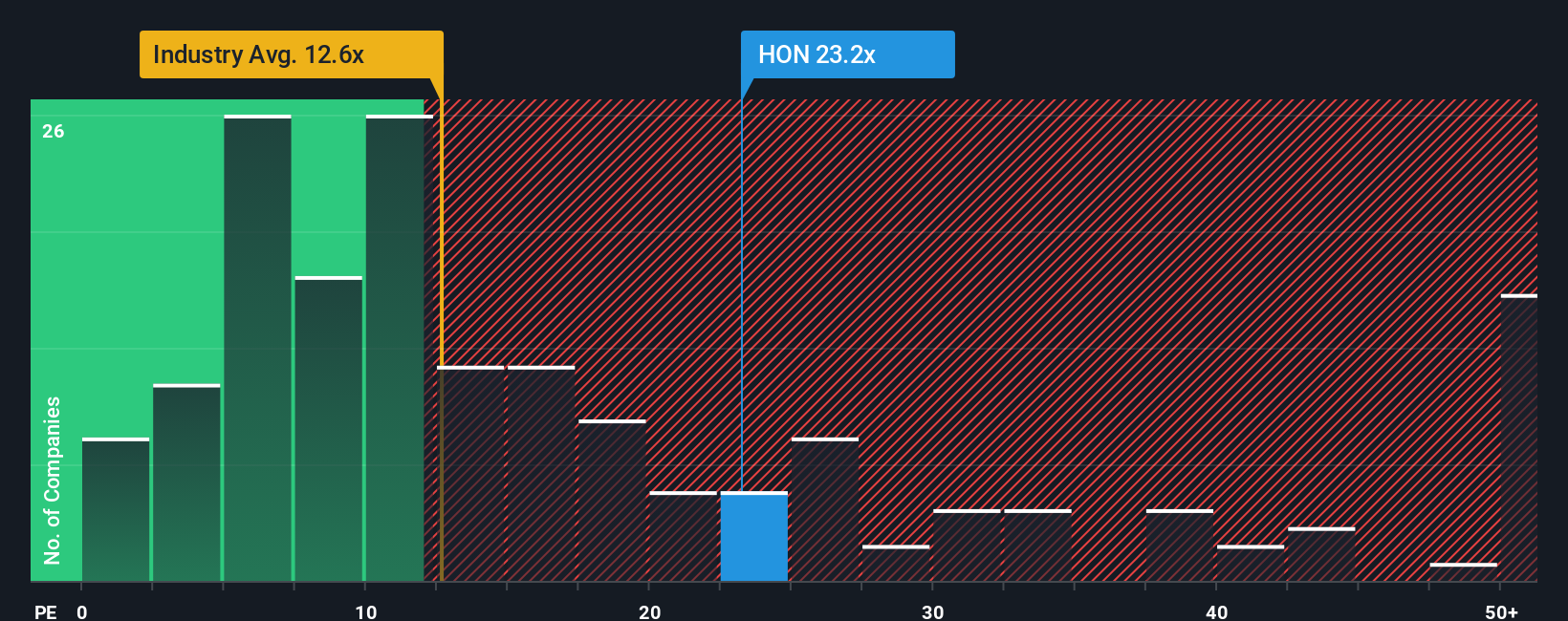

Approach 2: Honeywell International Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used valuation tools for profitable companies like Honeywell International because it directly compares a company’s market price to its earnings power. This is particularly useful for established businesses that generate consistent profits, and it helps investors understand what they are paying for each dollar of earnings.

It’s important to keep in mind that a "normal" or "fair" PE ratio isn’t set in stone. Factors such as expected earnings growth, profitability, market risks, and company size all influence what level of PE makes sense for a particular business. Fast-growing or less risky firms often command higher PE ratios than mature or more volatile peers.

Currently, Honeywell trades at a PE ratio of 20.3x, which is higher than the Industrials industry average of 12.7x but lower than the peer group average of 28.5x. To provide a clearer picture, Simply Wall St also calculates a proprietary “Fair Ratio” based on specific fundamentals, including Honeywell’s earnings growth outlook, risk profile, margins, and scale. For Honeywell, the Fair Ratio stands at 27.0x.

Instead of using only comparisons against peers or industry medians, the Fair Ratio offers a more tailored benchmark that reflects what investors might reasonably expect after factoring in Honeywell’s unique strengths and risks. This makes it a more comprehensive valuation check for long-term decision making.

Comparing the Fair Ratio of 27.0x to Honeywell’s actual PE of 20.3x suggests the stock is currently trading below its fair value according to this method.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1417 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Honeywell International Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story and perspective behind Honeywell International. It is where you connect your own beliefs about the company’s future (like estimates for revenue, earnings, and margins) to a fair value, all grounded in your understanding of its business trends and opportunities.

Narratives simplify investing by linking the company’s big-picture story to a financial forecast, and ultimately to what you believe is a fair share price, so you can move beyond stock tips and numbers and truly invest based on your own conviction. On Simply Wall St’s platform (inside the Community page, used by millions of investors), Narratives make it easy to compare your view to others, see updates as new news or results come in, and instantly see if Honeywell’s current price looks high or low compared to your assumptions.

This approach helps you decide whether to buy or sell by providing a clear comparison between your calculated Fair Value and the current market price. In addition, Narratives update in real time with fresh data, so your insights stay relevant. For example, some Honeywell International Narratives forecast a Fair Value as high as $290, while others see a much more modest target around $203, highlighting how perspectives and opportunity can vary widely between investors.

Do you think there's more to the story for Honeywell International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Honeywell International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HON

Honeywell International

Engages in the aerospace technologies, industrial automation, building automation, and energy and sustainable solutions businesses in the United States, Europe, and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor