Advertisement

- United States

- /

- Machinery

- /

- NasdaqCM:HIHO

Why It Might Not Make Sense To Buy Highway Holdings Limited (NASDAQ:HIHO) For Its Upcoming Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Highway Holdings Limited (NASDAQ:HIHO) is about to trade ex-dividend in the next three days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. This means that investors who purchase Highway Holdings' shares on or after the 12th of December will not receive the dividend, which will be paid on the 24th of December.

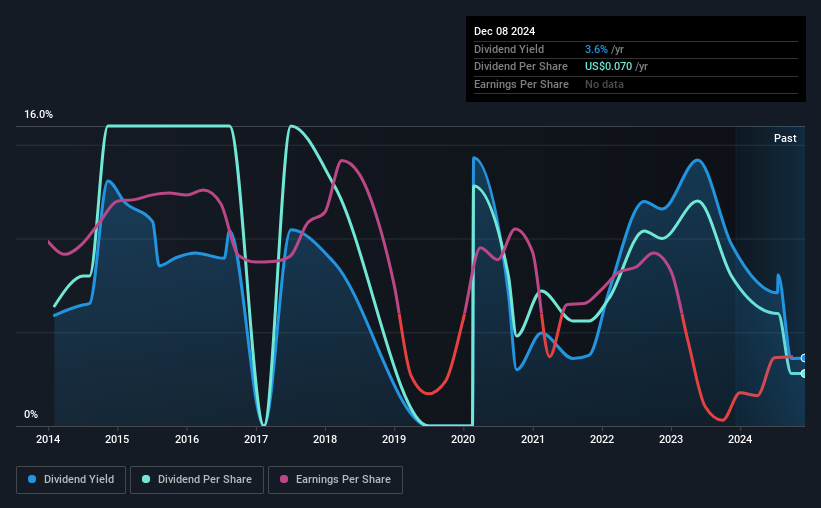

The company's next dividend payment will be US$0.05 per share. Last year, in total, the company distributed US$0.07 to shareholders. Calculating the last year's worth of payments shows that Highway Holdings has a trailing yield of 3.6% on the current share price of US$1.93. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Highway Holdings can afford its dividend, and if the dividend could grow.

See our latest analysis for Highway Holdings

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Highway Holdings lost money last year, so the fact that it's paying a dividend is certainly disconcerting. There might be a good reason for this, but we'd want to look into it further before getting comfortable. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If Highway Holdings didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out an unsustainably high 207% of its free cash flow as dividends over the past 12 months, which is worrying. Unless there were something in the business we're not grasping, this could signal a risk that the dividend may have to be cut in the future.

Highway Holdings does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Click here to see how much of its profit Highway Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Highway Holdings was unprofitable last year and, unfortunately, the general trend suggests its earnings have been in decline over the last five years, making us wonder if the dividend is sustainable at all.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Highway Holdings's dividend payments per share have declined at 7.9% per year on average over the past 10 years, which is uninspiring. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Remember, you can always get a snapshot of Highway Holdings's financial health, by checking our visualisation of its financial health, here.

To Sum It Up

Is Highway Holdings worth buying for its dividend? We're a bit uncomfortable with it paying a dividend while being loss-making, especially given that the dividend was not well covered by free cash flow. Bottom line: Highway Holdings has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

With that in mind though, if the poor dividend characteristics of Highway Holdings don't faze you, it's worth being mindful of the risks involved with this business. To help with this, we've discovered 3 warning signs for Highway Holdings that you should be aware of before investing in their shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Highway Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:HIHO

Highway Holdings

Manufactures and sells metal, plastic, electric, and electronic parts and components, subassemblies, and finished products in Hong Kong, China, Europe, and North America.

Flawless balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor