Advertisement

- United States

- /

- Trade Distributors

- /

- NasdaqGS:FTAI

Could FTAI Aviation's (FTAI) Engine Exchange Deal with Finnair Reveal Its Edge in Fleet Support?

Simply Wall St

Reviewed by Sasha Jovanovic

- Finnair Plc recently announced a multi-year Perpetual Power Agreement with FTAI Aviation Ltd., under which FTAI will provide engine exchanges to optimize maintenance flexibility, cost predictability, and fleet reliability.

- This partnership leverages FTAI’s Perpetual Power Program, designed to offer airlines tailored solutions that reduce costly shop visits and ensure guaranteed engine availability through in-house maintenance capabilities.

- We'll explore how the Finnair partnership spotlights FTAI's innovative fleet solutions and what it means for the company's investment narrative.

The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

FTAI Aviation Investment Narrative Recap

Shareholders in FTAI Aviation need to believe in the sustained demand for mid-life engine maintenance and the value of the company’s asset-light, vertically integrated model. The recent Finnair agreement underlines FTAI’s position in flexible, recurring-revenue engine services, but does not materially alter the most significant near-term catalyst, continued adoption of FTAI’s Maintenance, Repair, and Exchange programs amidst industry-wide shop visit delays. Concentration risk in legacy engine platforms remains the most immediate business challenge, as any rapid shift in airline technology or fleet modernization could pressure recurring revenues.

The most relevant recent announcement is FTAI’s inclusion in both the Russell 1000 Growth and Russell Midcap Growth benchmarks as of June 2025. This signals increasing institutional recognition and potential index-driven inflows, which could interact positively with customer wins like Finnair, reinforcing the narrative around market share gains and scale as catalysts for future earnings momentum.

Yet, in contrast to the headlines, investors also need to consider the risk of rapid technology shifts undermining demand for FTAI’s core engine platforms...

Read the full narrative on FTAI Aviation (it's free!)

FTAI Aviation's outlook anticipates $3.7 billion in revenue and $1.1 billion in earnings by 2028. This assumes annual revenue growth of 19.8% and a $683.5 million increase in earnings from the current $416.5 million level.

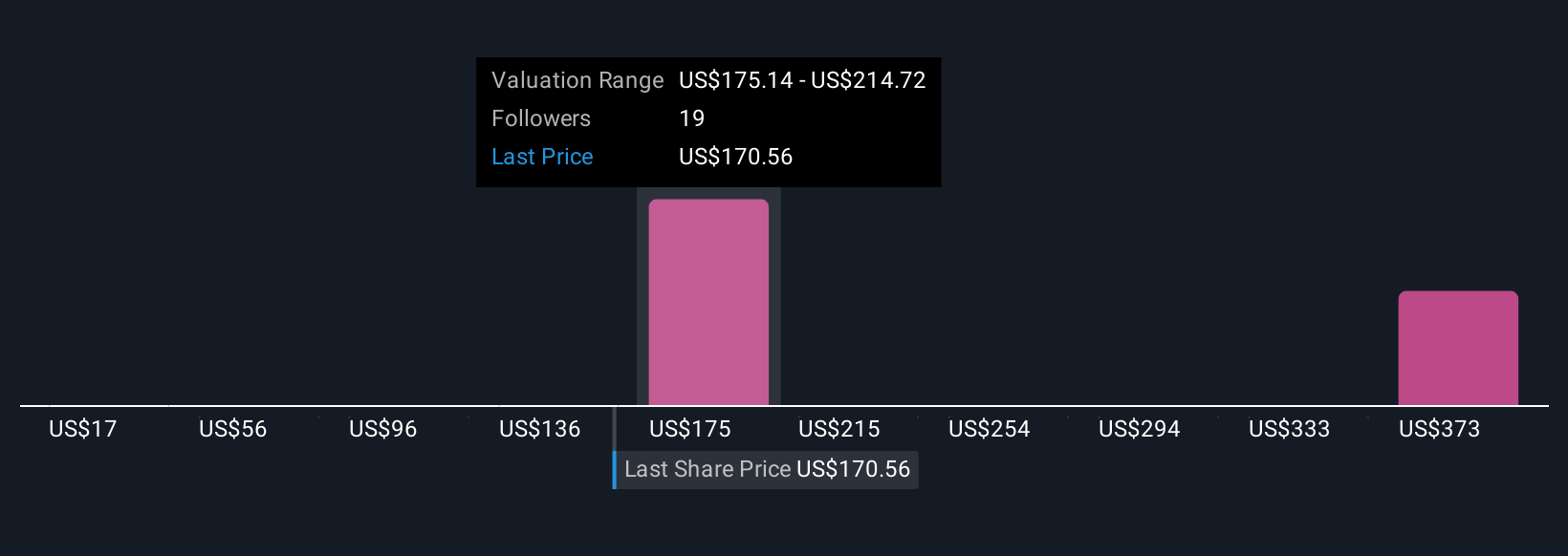

Uncover how FTAI Aviation's forecasts yield a $214.20 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community range from US$16.83 to US$214.20, reflecting wide differences in outlook. With such varied perspectives, and persistent concentration risk in aging engine platforms, readers can compare alternative frameworks to assess future business durability.

Explore 4 other fair value estimates on FTAI Aviation - why the stock might be worth less than half the current price!

Build Your Own FTAI Aviation Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your FTAI Aviation research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FTAI

FTAI Aviation

Owns, acquires, and sells aviation equipment for the transportation of goods and people worldwide.

High growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor