- United States

- /

- Electrical

- /

- NasdaqGS:ENVX

Enovix (NasdaqGS:ENVX) Unveils AI-1: Revolutionary Silicon-Anode Smartphone Battery Platform

Reviewed by Simply Wall St

Enovix (NasdaqGS:ENVX) recently saw an impressive 90% price increase over the last quarter, coinciding with its launch of the AI-1TM platform, a next-gen battery solution designed to enhance energy storage for smartphones. This development aligns with the technology sector's strength, driven by the S&P 500 and Nasdaq Composite's recent record highs, reflecting a robust market backdrop. The share repurchase program, announced on July 2, may have bolstered shareholder value, while broader market dynamics, including tariff discussions and tech sector volatility, contributed to fluctuations, yet maintained an upward trajectory in contrast to some tech stocks facing challenges.

The recent surge in Enovix's share price, attributed to the launch of the AI-1 platform, may signal investor optimism about the company’s future potential. This momentum aligns with the positive growth narrative, particularly with its strategic expansion into defense and smart eyewear markets forecasted to unlock new revenue streams. The share price jump, particularly impressive against the backdrop of recent tech sector volatility, underscores its positioning within a robust market context. Enovix's total shareholder return over the past three years was 22.47%, offering a longer-term perspective, though it underperformed compared to certain industry peers and market benchmarks over the past year.

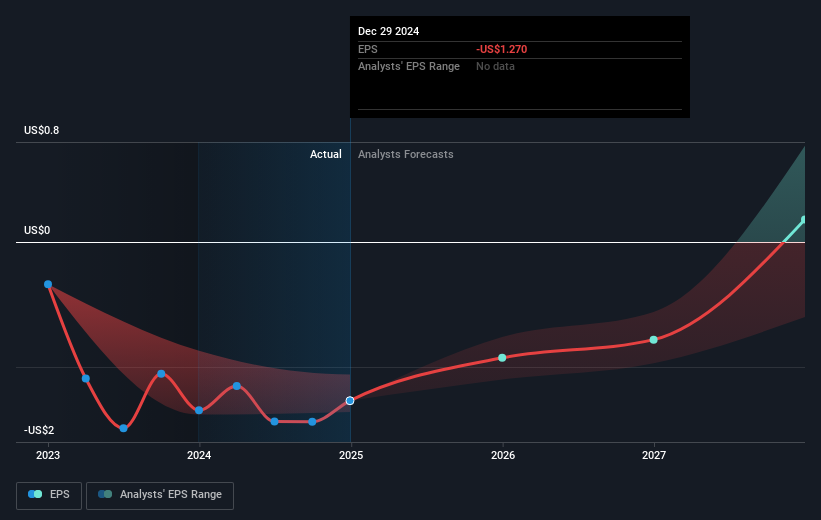

Enovix's focus on next-gen battery solutions is expected to have a significant impact on future revenue and earnings forecasts. Analysts anticipate a substantial increase in revenue at 171.2% annually over three years, although the company's path to profitability remains challenging, with ongoing EBITDA and EPS losses. If the company’s profit margins align with the industry average, it could see improved earnings and return on equity by 2028. Despite the increase in share price, there's still a significant gap when compared to the analyst consensus price target of US$26.91, suggesting possible upside potential. However, risks such as delays in high-volume production and customer qualification pose challenges to these optimistic projections.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enovix might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ENVX

Enovix

Designs, develops, and manufactures lithium-ion battery cells in the United States and internationally.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives