ServisFirst Bancshares (SFBS) shares have shown some movement this week, trading just above $71. With recent performance still lagging over the year, investors may be evaluating whether now presents a favorable entry point.

ServisFirst Bancshares' recent bump in share price this week offers a small relief after an extended period of weaker momentum. Despite today’s slight uptick, the stock is still working to recover from its 1-year total shareholder return of -26%, signaling that long-term performance has lagged even as new investors watch for signs of renewed strength.

The question now is whether ServisFirst Bancshares is trading below its intrinsic value and offering investors a bargain, or if the recent price already reflects expectations for the company’s future growth potential and recovery.

Advertisement

Most Popular Narrative: 17.2% Undervalued

ServisFirst Bancshares’ most followed narrative points to a fair value substantially above the last close of $71.76, suggesting upside potential. With market sentiment still hesitant, all eyes are on the drivers behind such a sizable fair value gap.

Expansion of commercial lending teams and ongoing hiring in key Southeastern markets positions the company to capitalize on robust population and business growth in the Sun Belt. This supports above-average organic loan and deposit growth, which is likely to drive top-line revenue and long-term earnings growth.

Do you want to know what’s fueling this optimistic valuation? The secret sauce is a bold prediction of record loan and revenue expansion, matched with ambitious margin and growth assumptions not typically seen in regional banks. Find out what quantitative leaps back up this narrative, and why consensus might be betting on a strong turnaround in underlying performance.

However, persistent challenges in commercial real estate and ongoing deposit growth pressures may undermine the optimistic outlook for ServisFirst’s recovery narrative.

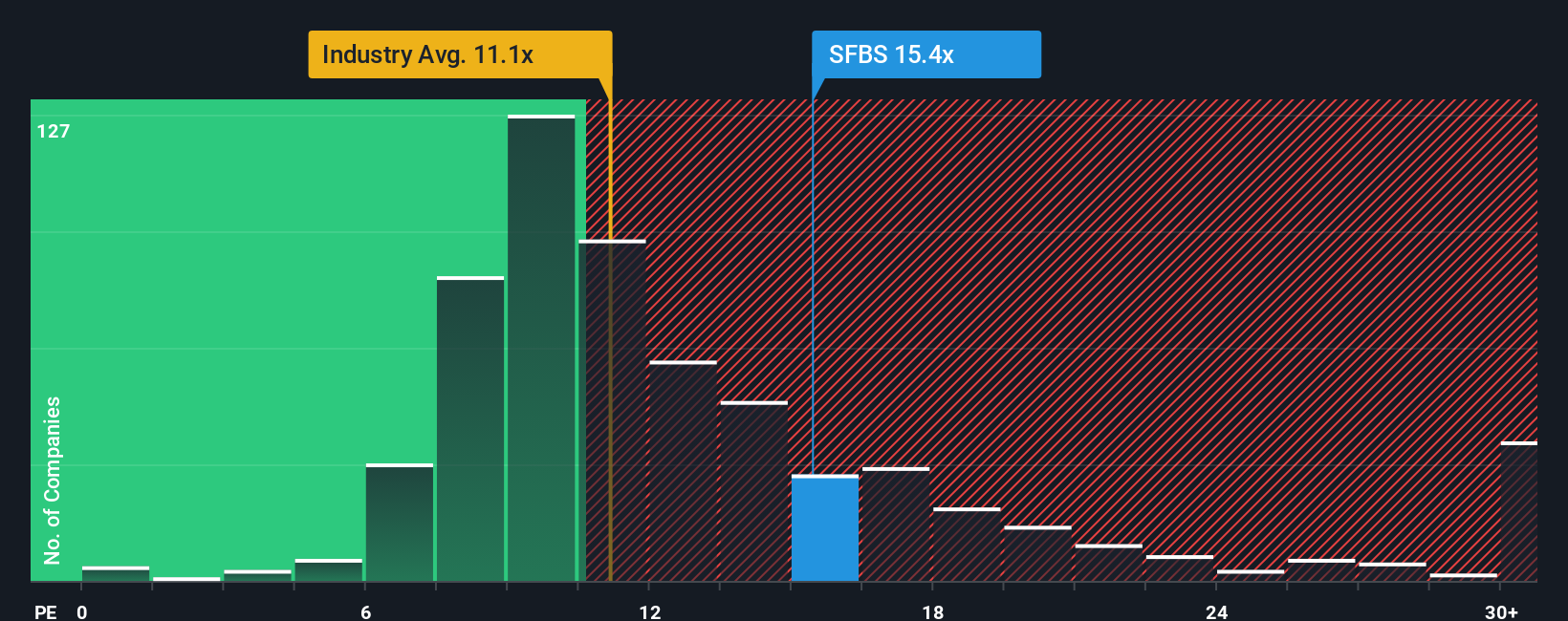

Looking at price-to-earnings, ServisFirst trades at 15.4x, which is higher than both the US Banks industry average of 11.1x and its own fair ratio of 13.3x. This suggests shares might be on the expensive side compared to peers and market expectations, adding a note of caution. Does this higher multiple signal confidence in a turnaround, or could it mean limited room for upside?

If you have a different perspective or want to analyze the numbers firsthand, dive into the data and craft your own story. It takes just a few minutes. Do it your way

A great starting point for your ServisFirst Bancshares research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Ready to unlock the full potential of your portfolio? Stay ahead of the curve and jump on emerging trends before the crowd by checking out these hand-picked opportunities:

Capture the momentum of cutting-edge innovation using these 25 AI penny stocks, which are accelerating real change and showing promise in tomorrow’s markets.

Boost your returns with these 883 undervalued stocks based on cash flows, identified by smart algorithms as offering compelling value and providing growth opportunities that others might overlook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks