Nicolet Bankshares (NIC) shares have held steady this week with minor fluctuations, giving investors a snapshot of how regional banks are navigating today’s market landscape. The stock’s recent behavior invites a closer look at its overall performance.

Over the past year, Nicolet Bankshares has quietly posted a 0.46% total shareholder return, suggesting steady momentum even as its recent share price has seen only minor movement. As markets weigh shifting risk and growth prospects, the longer-term view still signals gradual confidence in the company's position.

Yet with shares trading at a discount to some analyst targets and a moderate valuation, the real question remains: is the market underestimating Nicolet Bankshares’ future potential, or is everything already baked into the price?

Advertisement

Price-to-Earnings of 14.6x: Is it justified?

Nicolet Bankshares shares closed at $133.57, trading at a price-to-earnings ratio of 14.6x. This sits below the peer average, hinting at potential value relative to other regional banks.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay for each dollar of the company’s earnings and provides insight into market expectations for future profit growth. For a bank like Nicolet, this is a central indicator of market sentiment and sector confidence.

Currently, Nicolet Bankshares’ P/E is lower than the average among its peers (18.6x). This suggests the market may be discounting the company’s future outlook. However, when compared to the estimated fair P/E ratio of 11.5x, the stock actually looks somewhat expensive, indicating that investors might be pricing in higher-than-justified growth or quality expectations.

The level the market could move toward, guided by fair-value regression models, is the fair P/E ratio of 11.5x. This benchmark serves as a potential anchor for future valuation adjustments.

However, slowing revenue growth and modest net income gains could present challenges. This may prompt investors to reassess the company's near-term prospects.

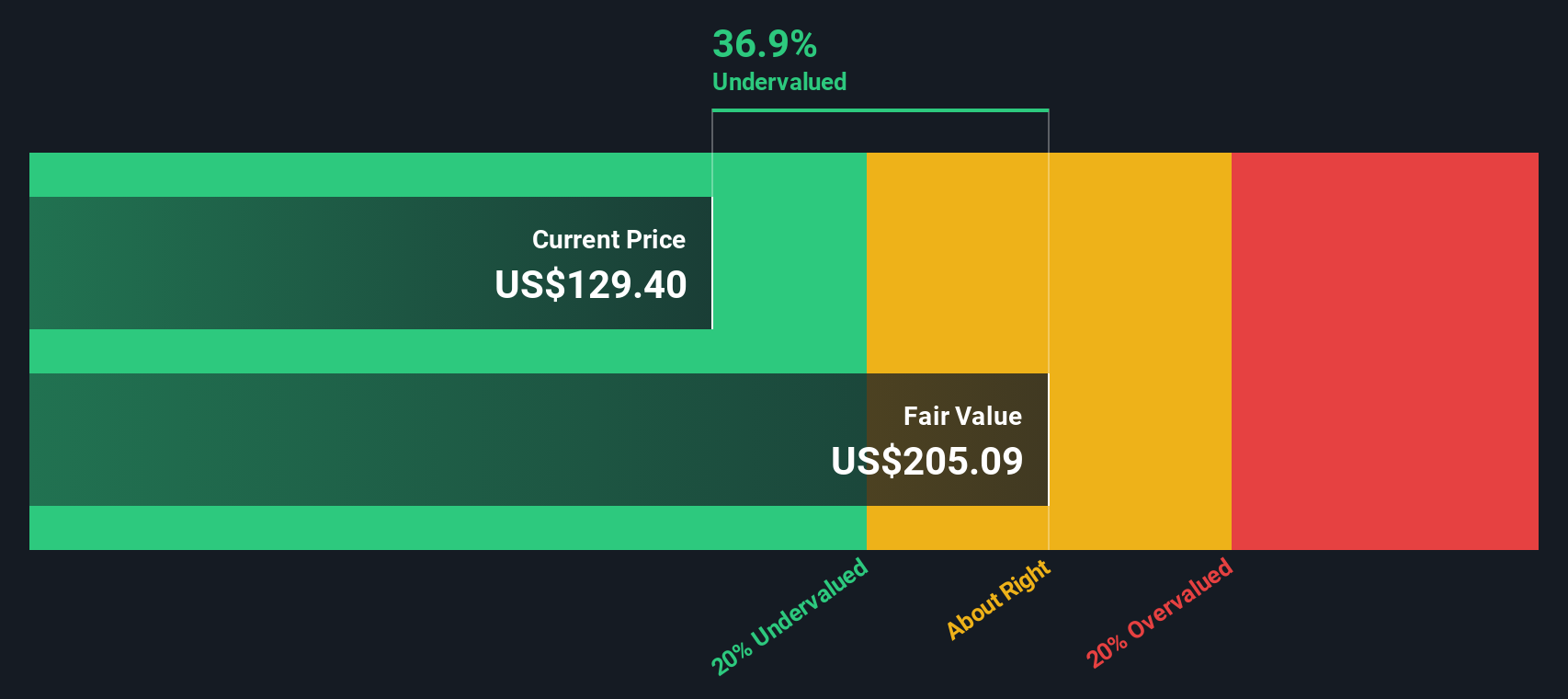

Switching perspectives, the SWS DCF model paints a much more optimistic picture for Nicolet Bankshares. According to this approach, the shares are trading about 34% below their estimated fair value. Could the market be missing this deeper value, or is the risk profile higher than it seems?

If you see things differently or want to dig into the numbers yourself, you can craft your own take on Nicolet Bankshares in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nicolet Bankshares.

Looking for more investment ideas?

Don’t wait on opportunities. Propel your investing goals forward with a range of hand-picked stock ideas using Simply Wall Street’s powerful screener tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nicolet Bankshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Operates as the bank holding company for Nicolet National Bank that provides banking products and services for businesses and individuals in Wisconsin, Michigan, and Minnesota.