Advertisement

- United States

- /

- Banks

- /

- NYSE:LOB

Earnings Miss and Rising Charge-Offs Might Change The Case For Investing In Live Oak Bancshares (LOB)

Simply Wall St

Reviewed by Sasha Jovanovic

- In October 2025, Live Oak Bancshares reported third-quarter results with net interest income rising to US$115.49 million and net income of US$26.52 million, but earnings per share missed analyst forecasts and the company disclosed much higher net charge-offs year-on-year.

- While core banking metrics such as loan and deposit growth remain strong, the sharp increase in net charge-offs raises new questions about credit quality and risk management trends.

- We'll explore how the earnings miss and elevated charge-offs could influence the company’s digital-first growth ambitions going forward.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Live Oak Bancshares Investment Narrative Recap

To be a shareholder of Live Oak Bancshares, you have to believe in the company’s capacity to sustain rapid digital banking and small business lending growth, despite sector-specific risks. The most important short-term catalyst, ongoing expansion in loan and deposit volumes, is tested by this quarter’s sharp rise in net charge-offs, which materially increases credit quality concerns and could dampen confidence in near-term profitability and risk management.

Among recent developments, the Q3 2025 earnings announcement stands out. Despite showing robust loan and deposit growth, the simultaneous surge in net charge-offs and a miss on earnings per share has cast a spotlight on the delicate balance between aggressive lending expansion and rising credit risk, both of which are key to the company’s digital-first ambitions.

By contrast, investors should be aware of the sudden spike in bad loans and what this could mean for...

Read the full narrative on Live Oak Bancshares (it's free!)

Live Oak Bancshares is projected to reach $1.1 billion in revenue and $328.0 million in earnings by 2028. This outlook assumes annual revenue growth of 37.6% and an earnings increase of $271.9 million from the current $56.1 million.

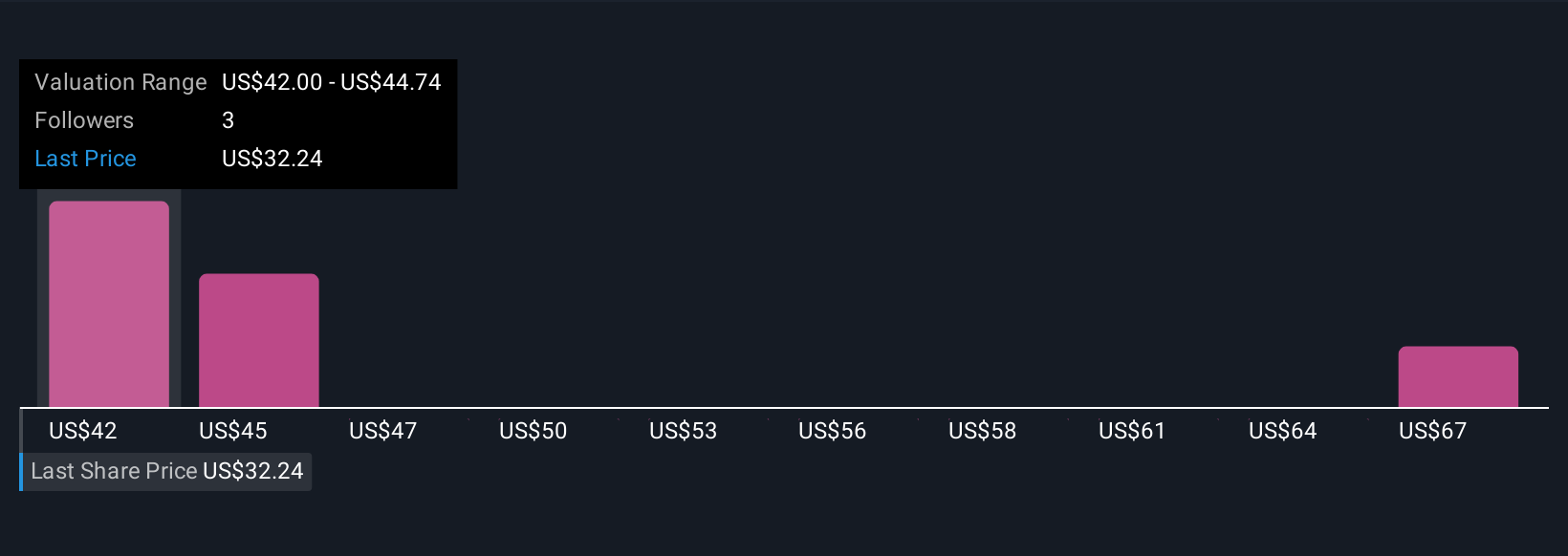

Uncover how Live Oak Bancshares' forecasts yield a $42.00 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community users provide three fair value estimates for Live Oak Bancshares, ranging from US$42 to US$69.40. While you consider these broad valuations, keep in mind that rising net charge-offs could influence future earnings quality and risk perception, offering several perspectives worth weighing before making your own assessment.

Explore 3 other fair value estimates on Live Oak Bancshares - why the stock might be worth just $42.00!

Build Your Own Live Oak Bancshares Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Live Oak Bancshares research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Live Oak Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Live Oak Bancshares' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LOB

Live Oak Bancshares

Operates as the bank holding company for Live Oak Banking Company that provides various banking products and services in the United States.

High growth potential and good value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor