Advertisement

- United States

- /

- Banks

- /

- NYSE:BKU

Regional Bank Credit Quality Concerns Could Be a Game Changer for BankUnited (BKU)

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, disclosures from regional lenders Zions Bancorp and Western Alliance Bancorp about significant loan charge-offs and collateral issues have raised industry-wide concerns about deteriorating loan quality.

- This development has intensified investor scrutiny of credit risk in regional banks, putting a spotlight on institutions like BankUnited that share similar lending exposures.

- We'll explore how renewed credit quality fears could affect BankUnited's investment narrative and its outlook for earnings growth and risk management.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

BankUnited Investment Narrative Recap

To be a shareholder in BankUnited today, you likely need to believe that its strong deposit growth, geographic expansion, and investments in fee-based business lines will outweigh ongoing concerns about loan quality associated with its commercial real estate portfolio. The recent news from other regional lenders has undoubtedly intensified short-term focus on credit risk, but so far, it hasn’t signaled a material shift in BankUnited’s core earnings trajectory or key risk/catalyst profile. Of the company’s recent announcements, the planned opening of a new Tampa, Florida office stands out in the context of current industry concerns, as it furthers BankUnited’s push into high-growth markets. This expansion supports long-term growth catalysts through new loan and deposit opportunities, even as short-term caution lingers over credit quality and the office CRE portfolio. However, even with continued expansion, investors should watch for signs that credit quality deterioration in office real estate could...

Read the full narrative on BankUnited (it's free!)

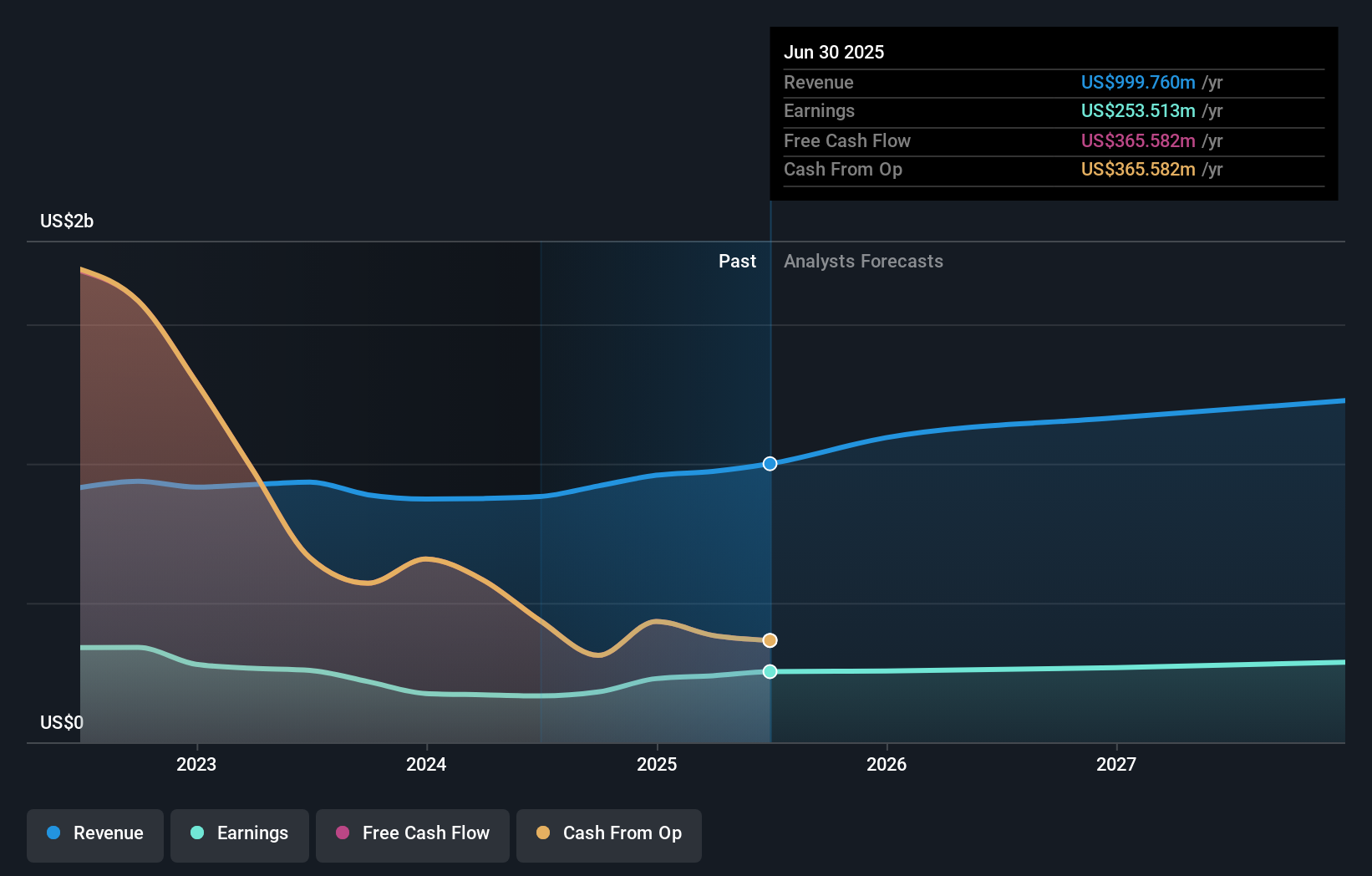

BankUnited's narrative projects $1.3 billion revenue and $291.8 million earnings by 2028. This requires 8.9% yearly revenue growth and a $38.3 million earnings increase from the current $253.5 million.

Uncover how BankUnited's forecasts yield a $43.03 fair value, a 19% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s single fair value estimate for BankUnited is US$43.03, reflecting a tight consensus among retail investors. In light of renewed industry credit quality concerns, it remains important to consider how risks around commercial real estate loan performance might play a growing role in shaping outcomes for BankUnited and its shareholders.

Explore another fair value estimate on BankUnited - why the stock might be worth as much as 19% more than the current price!

Build Your Own BankUnited Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your BankUnited research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free BankUnited research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BankUnited's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BankUnited might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BKU

BankUnited

Operates as the bank holding company for BankUnited, a national banking association that provides a range of banking services in the United States.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets