Beacon Financial (BBT) shares have seen a steady decline over the past month, slipping nearly 7%. Investors are weighing this trend alongside the company’s recent annual figures, which show strong growth in both revenue and net income.

Beacon Financial’s slide over the past month highlights a clear shift in momentum, with a 1-month share price return of -6.92%. While share price has lost ground in 2024, this comes right after a strong year of financial growth. Investors are left to weigh whether the recent pullback signals a buying opportunity or just a pause in the rally.

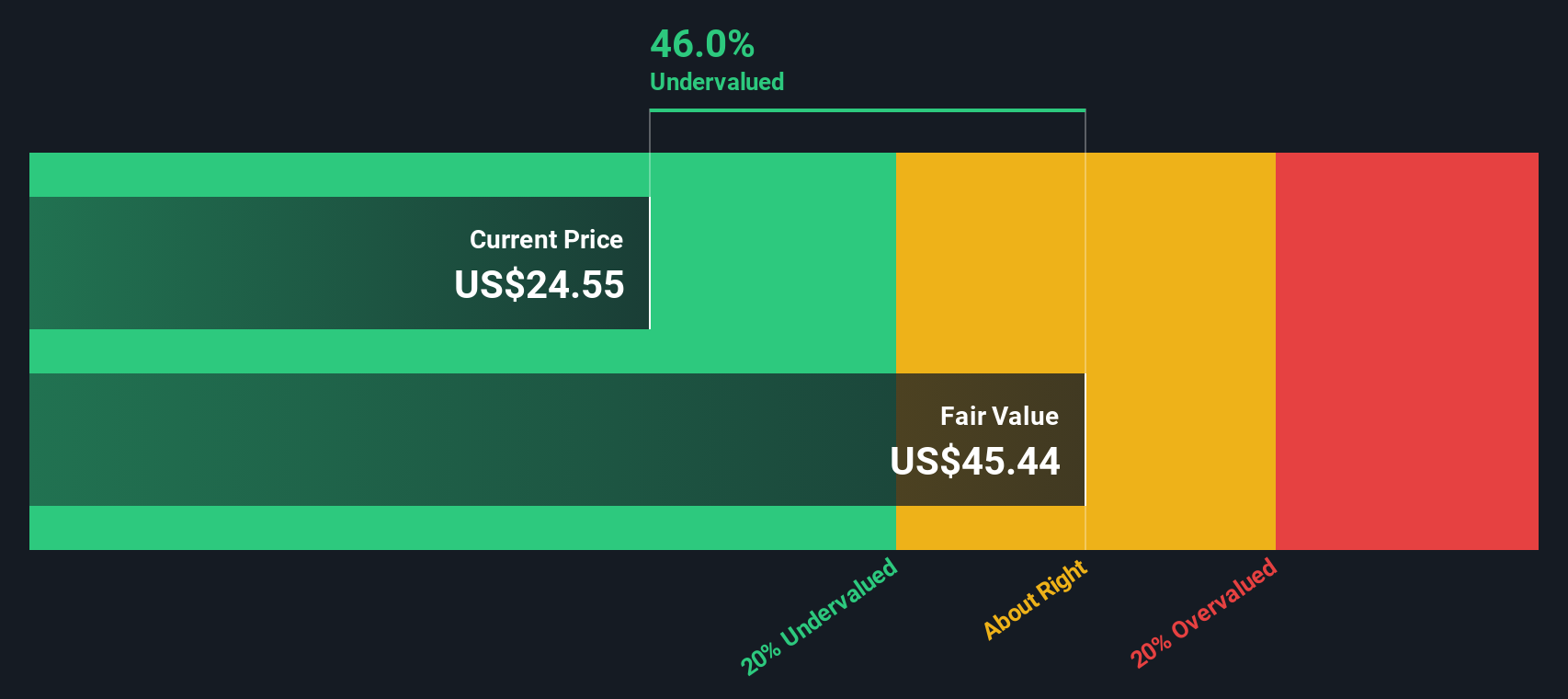

With strong earnings but a declining share price, is Beacon Financial now trading below its true value? Or is the recent dip simply reflecting that the market has already priced in its future growth prospects?

Advertisement

Price-to-Earnings of 24.9x: Is it justified?

Beacon Financial’s shares currently trade at a price-to-earnings (P/E) ratio of 24.9x, which is significantly higher than what is typical in the banking sector. At a last close price of $23.27, the stock appears expensive relative to both its peers and the industry standard.

The price-to-earnings ratio compares a company’s current share price to its per-share earnings. For banks, this multiple is widely used since profits are a key driver of value and banking earnings can be relatively stable. A higher P/E typically signals that investors expect stronger growth or quality, while a lower ratio might indicate caution or weak prospects.

Beacon Financial’s P/E ratio far exceeds the US Banks industry average of 11.6x and even the peer group average of 16x. While this could suggest the market is pricing in strong future earnings growth or unique strengths, it also means expectations are elevated. In contrast, compared to an estimated fair price-to-earnings ratio of 49.2x, the market’s current pricing is much more conservative, hinting that there may be upside if projected growth is realized.

The SWS DCF model takes a different approach, focusing on future cash flows rather than just earnings multiples. According to this method, Beacon Financial’s current share price is about 5.6% below our fair value estimate. That suggests the stock could be undervalued if its growth continues. But does this signal a true bargain or just reflect optimism in forecasts?

If you’re looking to take a hands-on approach, you can dig into the underlying numbers and craft your own perspective in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Beacon Financial.

Looking for more investment ideas?

Don’t miss out on high-potential stocks and hidden gems. The market is moving fast, and now is the time to take charge of your next smart move.

Seize the chance to find companies making waves in artificial intelligence with these 24 AI penny stocks that stand out for their innovation and momentum.

Unlock the power of stable income by checking out these 20 dividend stocks with yields > 3% offering robust yields and consistent returns for income-focused investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beacon Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.