Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:WABC

Westamerica Bancorporation (WABC): Evaluating Valuation After Fed Comments Boost Banking Sector Optimism

Simply Wall St

Reviewed by Simply Wall St

Westamerica Bancorporation (WABC) shares climbed after the New York Federal Reserve President signaled there could be more interest rate adjustments ahead. This raised hopes for a December rate cut among investors and sent banking stocks higher.

See our latest analysis for Westamerica Bancorporation.

Westamerica Bancorporation’s shares have rebounded alongside other banks on hopes of interest rate relief, but that jump follows months of pressure. Its 1-year total shareholder return is down 15.1%, and momentum has lagged despite occasional rallies. The recent uptick hints that investors are readjusting risk expectations, though longer-term performance remains subdued.

If shifting sentiment in the banking sector has you curious, now’s a great moment to broaden your portfolio and discover fast growing stocks with high insider ownership

But with shares still well below their one-year highs despite a recent bounce, investors are left wondering if Westamerica Bancorporation is undervalued at current levels or if the market is already anticipating a turnaround in growth.

Price-to-Earnings of 9.9x: Is it justified?

Westamerica Bancorporation trades at a price-to-earnings (P/E) ratio of 9.9x, placing it well below the peer group and sector averages. This suggests the stock may be undervalued relative to other banks, especially when considering the recent market price of $47.65.

The P/E ratio measures how much investors are paying for each dollar of company earnings. For banks like WABC, this gauge helps investors decide if the valuation reflects profitability and future expectations. A lower multiple could indicate a bargain if earnings are consistent or growing.

Compared to both its peers (P/E of 15.1x) and the banks industry average (P/E of 11.2x), WABC’s valuation appears notably more conservative. However, when measured against its estimated fair P/E ratio of 7.3x, the stock screens as somewhat expensive by this metric. This difference highlights possible market caution or reflects anticipated challenges ahead. Investors should watch if the market moves closer to that lower fair ratio over time.

Explore the SWS fair ratio for Westamerica Bancorporation

Result: Price-to-Earnings of 9.9x (UNDERVALUED relative to peers, OVERVALUED relative to fair ratio)

However, declining annual revenue and net income growth could signal ongoing challenges. This makes a swift recovery for Westamerica Bancorporation less certain.

Find out about the key risks to this Westamerica Bancorporation narrative.

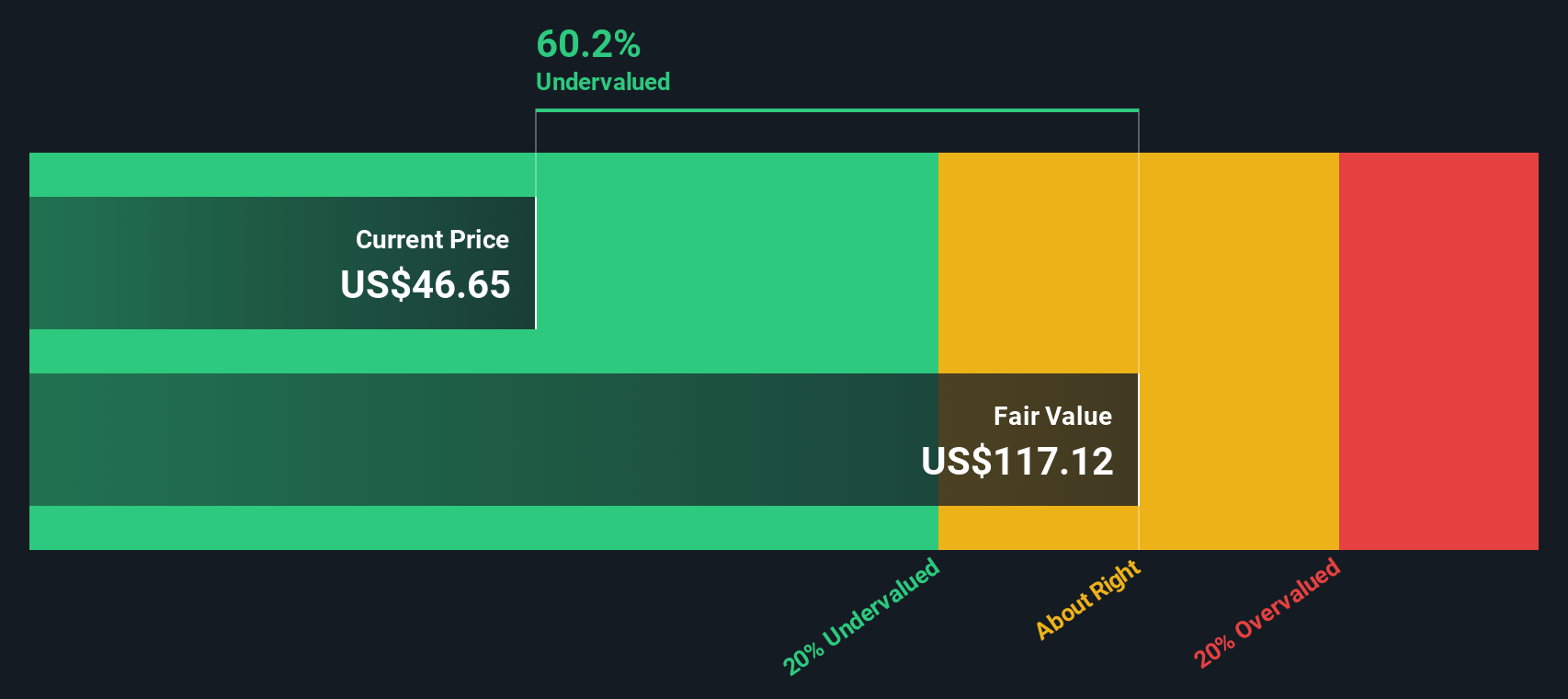

Another View: Our DCF Model Says Undervalued

While the price-to-earnings ratio paints a mixed picture, the SWS DCF model comes to a very different conclusion. It estimates Westamerica Bancorporation’s fair value at $115.68, far above the current price. This suggests an undervalued opportunity. Could the market be missing something significant here?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Westamerica Bancorporation for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 926 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Westamerica Bancorporation Narrative

If you have a different perspective or want to dig into the numbers yourself, you can build your own view in just a few minutes. Do it your way

A great starting point for your Westamerica Bancorporation research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t miss out on high-potential stocks that others may be overlooking. Use these powerful screeners to uncover your next winning investment before the crowd catches on.

- Boost your income potential by choosing from these 15 dividend stocks with yields > 3%, which offers reliable yields above 3%.

- Catch emerging tech opportunities by reviewing these 26 AI penny stocks, which harness artificial intelligence for rapid growth.

- Maximize value by targeting these 926 undervalued stocks based on cash flows, featuring strong fundamentals and attractive pricing right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Westamerica Bancorporation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WABC

Westamerica Bancorporation

Operates as a bank holding company for the Westamerica Bank that provides various banking products and services to individual and commercial customers in the United States.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor