TriCo Bancshares (TCBK) stock has seen some interesting shifts over the past month, with shares dipping about 4%. Investors are eyeing those moves and weighing the company’s track record against broader banking sector trends.

Despite some recent selling pressure, TriCo Bancshares is still holding up over the long run. Its 1-year total shareholder return sits at 5.7%, and share price returns have been more modest with only a slight gain since the beginning of the year. After a strong 7-day share price rebound of just over 5%, the momentum looks like it could be turning around for now, especially as the stock continues to recover ground from this month's dip.

But with TriCo Bancshares trading at a notable discount to analyst price targets and boasting steady earnings growth, is this a case of an undervalued opportunity waiting to be seized, or is the market already considering its future potential?

Advertisement

Price-to-Earnings of 12.6x: Is it justified?

TriCo Bancshares currently trades at a price-to-earnings (P/E) ratio of 12.6x, which gives investors perspective on how the market values its profitability relative to peers. With a recent closing price of $43.26, this multiple signals the market is putting a premium on TCBK's earnings compared to broader benchmarks.

The P/E ratio measures the price investors are willing to pay for each dollar of the company’s earnings over the last twelve months. For banks, this metric serves as a common yardstick for comparing relative value within the financial sector, especially where stable earnings matter.

Right now, TriCo Bancshares trades at a higher P/E than both the estimated fair price-to-earnings ratio of 11.3x and the US Banks industry average of 11.2x. This suggests the market could be optimistic about TCBK's earnings outlook, or possibly overpricing its future potential compared to its sector. For reference, the peer group average is higher at 13.6x, so TCBK is not among the most expensive. Investors should be mindful of where sentiment may shift if performance diverges from expectations.

However, potential risks remain, including unexpected shifts in interest rates or weaker earnings growth. Either of these factors could impact future investor sentiment.

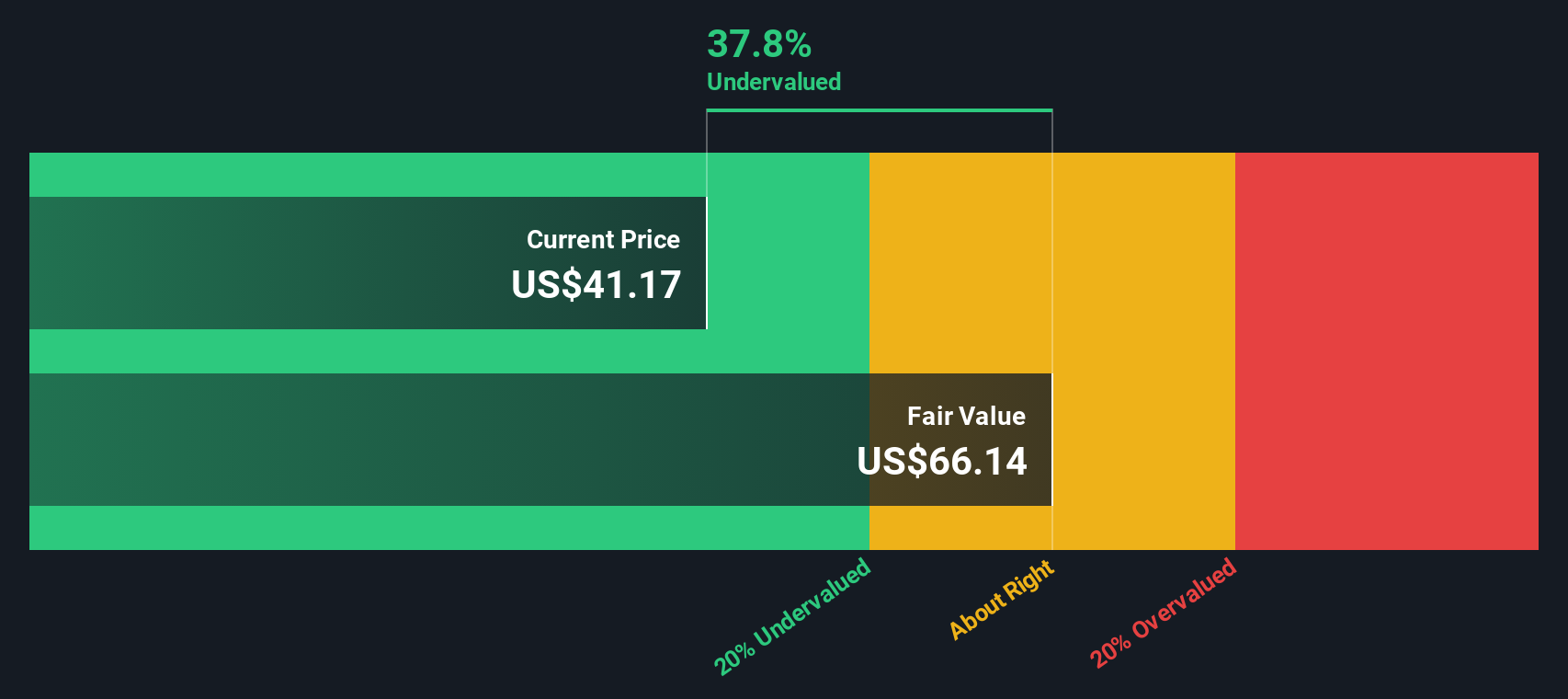

Looking at TriCo Bancshares through the lens of our DCF model tells a very different story. The SWS DCF model estimates a fair value of $71.31 per share, meaning the current stock price trades at a sizable 39.3% discount. This approach suggests there could be significant upside that the P/E ratio does not capture. Which method will prove most accurate as markets evolve?

If you want a different perspective or prefer digging into the numbers yourself, it's easy to build your own view of TriCo Bancshares in just a few minutes, Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding TriCo Bancshares.

Looking for more investment ideas?

Give yourself a key advantage by uncovering bold opportunities others may be missing. Use the Simply Wall Street Screener and stay ahead of the crowd with these handpicked ideas:

Tap into the artificial intelligence boom and pinpoint tomorrow’s innovators through these 27 AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TriCo Bancshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.