Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:TCBK

TriCo Bancshares' (NASDAQ:TCBK) Upcoming Dividend Will Be Larger Than Last Year's

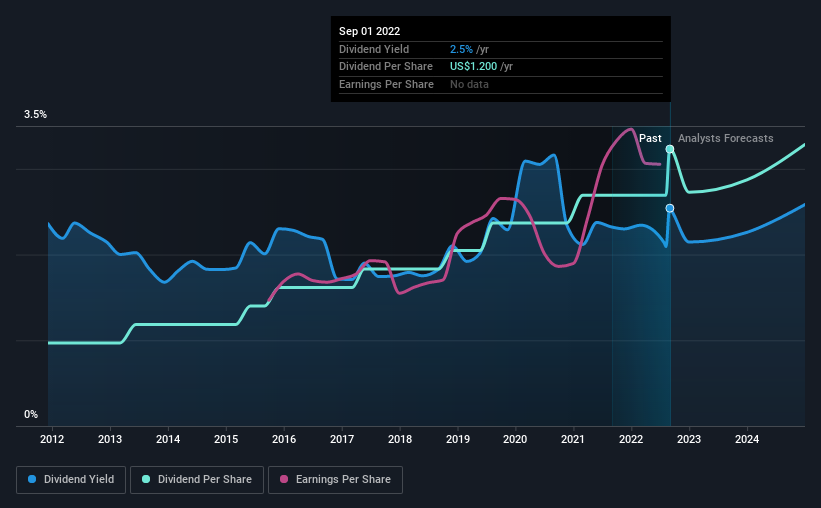

TriCo Bancshares (NASDAQ:TCBK) will increase its dividend from last year's comparable payment on the 23rd of September to $0.30. Based on this payment, the dividend yield for the company will be 2.5%, which is fairly typical for the industry.

See our latest analysis for TriCo Bancshares

TriCo Bancshares' Payment Expected To Have Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable.

Having distributed dividends for at least 10 years, TriCo Bancshares has a long history of paying out a part of its earnings to shareholders. Past distributions do not necessarily guarantee future ones, but TriCo Bancshares' payout ratio of 29% is a good sign as this means that earnings decently cover dividends.

Over the next 3 years, EPS is forecast to expand by 31.8%. The future payout ratio could be 25% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

TriCo Bancshares Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. The dividend has gone from an annual total of $0.36 in 2012 to the most recent total annual payment of $1.20. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Has Growth Potential

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that TriCo Bancshares has grown earnings per share at 7.9% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for TriCo Bancshares' prospects of growing its dividend payments in the future.

An additional note is that the company has been raising capital by issuing stock equal to 12% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

TriCo Bancshares Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for TriCo Bancshares that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if TriCo Bancshares might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TCBK

TriCo Bancshares

Operates as a bank holding company for Tri Counties Bank that provides commercial banking services to individual and corporate customers.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor