Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:SFNC

The Bull Case For Simmons First National (SFNC) Could Change Following Q3 Securities Sale Loss

Simply Wall St

Reviewed by Sasha Jovanovic

- Simmons First National Corp recently reported a significant net loss for Q3 2025, primarily resulting from a substantial loss on the sale of securities as disclosed in its Form 10-Q filing.

- This development highlights ongoing efforts to offset profit pressures by reducing interest expense and increasing the company’s focus on credit risk management in a challenging operating landscape.

- We’ll examine how this setback in securities sales may influence Simmons First National’s broader investment narrative and forward-looking growth assumptions.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Simmons First National Investment Narrative Recap

For shareholders of Simmons First National, the long-term case relies on confidence in the bank’s ability to generate future loan and deposit growth, leverage digital banking investments, and manage credit quality through economic cycles. The recent Q3 2025 net loss, driven by a one-off loss on the sale of securities, may weigh on near-term sentiment, but does not appear to materially alter the core catalyst: returning to sustained profitability as revenue continues to recover; the biggest risk remains ongoing credit quality challenges within specific loan categories.

A particularly relevant announcement was the Q3 2025 earnings release, which highlighted not only the securities-related loss but also a continued increase in net interest income as interest expense declined. This underscores management’s current emphasis on operational efficiency and credit risk management while navigating the evolving banking environment and pursuing future profitability targets.

However, investors should be aware that despite efforts to strengthen credit oversight, the uptick in net charge-offs reported in Q3 could signal...

Read the full narrative on Simmons First National (it's free!)

Simmons First National's narrative projects $1.3 billion revenue and $354.8 million earnings by 2028. This requires 19.7% yearly revenue growth and a $194.6 million earnings increase from $160.2 million.

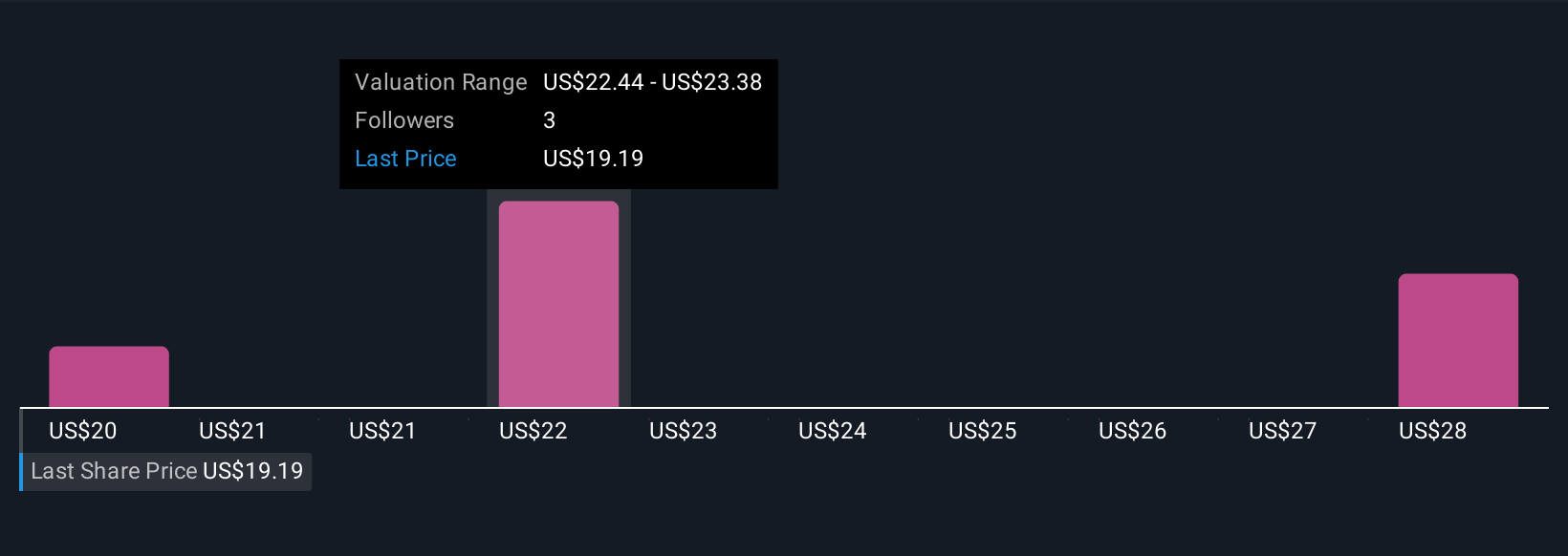

Uncover how Simmons First National's forecasts yield a $22.80 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have shared three separate fair value estimates for Simmons First National, ranging from US$17.02 to US$29.22 per share. While some anticipate rising revenue growth, concerns about sustained credit quality could affect future performance, so consider exploring diverse viewpoints in your own research.

Explore 3 other fair value estimates on Simmons First National - why the stock might be worth as much as 63% more than the current price!

Build Your Own Simmons First National Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Simmons First National research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Simmons First National research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Simmons First National's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SFNC

Simmons First National

Operates as the bank holding company for Simmons Bank that provides banking and other financial products and services to individuals and businesses.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor