- United States

- /

- Banks

- /

- NasdaqGM:HIFS

Investors more bullish on Hingham Institution for Savings (NASDAQ:HIFS) this week as stock ascends 9.9%, despite earnings trending downwards over past year

If you want to compound wealth in the stock market, you can do so by buying an index fund. But investors can boost returns by picking market-beating companies to own shares in. For example, the Hingham Institution for Savings (NASDAQ:HIFS) share price is up 40% in the last 1 year, clearly besting the market return of around 31% (not including dividends). So that should have shareholders smiling. Unfortunately the longer term returns are not so good, with the stock falling 23% in the last three years.

After a strong gain in the past week, it's worth seeing if longer term returns have been driven by improving fundamentals.

View our latest analysis for Hingham Institution for Savings

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Over the last twelve months, Hingham Institution for Savings actually shrank its EPS by 48%.

Given the share price gain, we doubt the market is measuring progress with EPS. Indeed, when EPS is declining but the share price is up, it often means the market is considering other factors.

We doubt the modest 1.0% dividend yield is doing much to support the share price. Hingham Institution for Savings' revenue actually dropped 34% over last year. So using a snapshot of key business metrics doesn't give us a good picture of why the market is bidding up the stock.

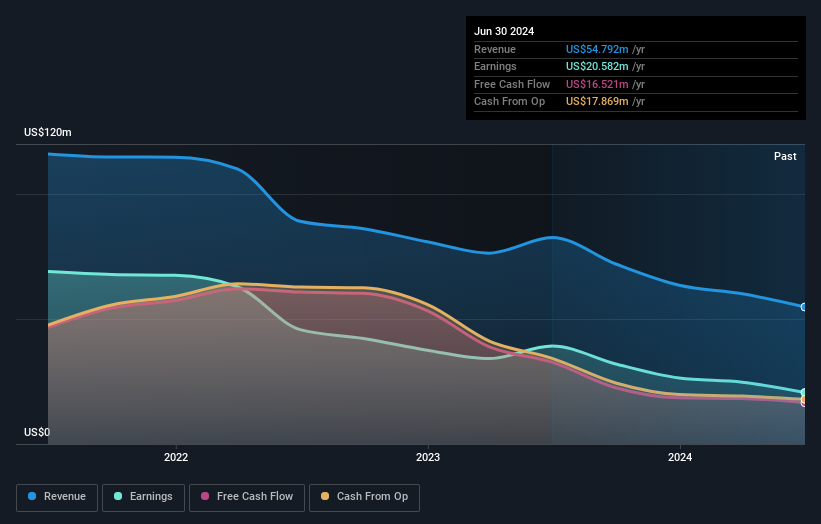

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. This free interactive report on Hingham Institution for Savings' earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

A Different Perspective

It's nice to see that Hingham Institution for Savings shareholders have received a total shareholder return of 42% over the last year. And that does include the dividend. That gain is better than the annual TSR over five years, which is 8%. Therefore it seems like sentiment around the company has been positive lately. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. It's always interesting to track share price performance over the longer term. But to understand Hingham Institution for Savings better, we need to consider many other factors. To that end, you should learn about the 2 warning signs we've spotted with Hingham Institution for Savings (including 1 which doesn't sit too well with us) .

Hingham Institution for Savings is not the only stock insiders are buying. So take a peek at this free list of small cap companies at attractive valuations which insiders have been buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hingham Institution for Savings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:HIFS

Hingham Institution for Savings

Provides various financial products and services to individuals and small businesses in the United States.

Excellent balance sheet and slightly overvalued.