Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:FNCB

Is Now The Time To Put FNCB Bancorp (NASDAQ:FNCB) On Your Watchlist?

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in FNCB Bancorp (NASDAQ:FNCB). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

View our latest analysis for FNCB Bancorp

How Fast Is FNCB Bancorp Growing?

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. It's no surprise, then, that I like to invest in companies with EPS growth. FNCB Bancorp managed to grow EPS by 7.8% per year, over three years. That might not be particularly high growth, but it does show that per-share earnings are moving steadily in the right direction.

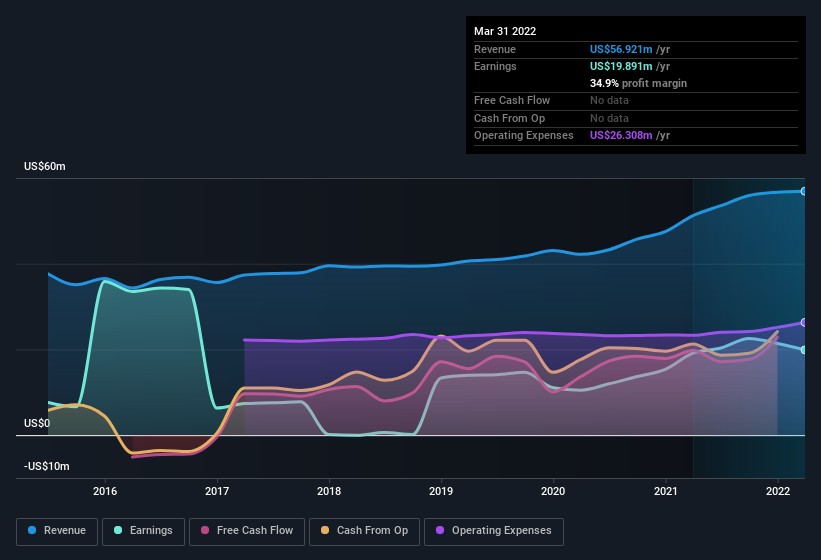

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). I note that FNCB Bancorp's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. While we note FNCB Bancorp's EBIT margins were flat over the last year, revenue grew by a solid 11% to US$57m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

FNCB Bancorp isn't a huge company, given its market capitalization of US$163m. That makes it extra important to check on its balance sheet strength.

Are FNCB Bancorp Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

In the last year insider at FNCB Bancorp were both selling and buying shares; but happily, as a group they spent US$60k more on stock, than they netted from selling it. On balance, that's a good sign. It is also worth noting that it was Independent Director William Bracey who made the biggest single purchase, worth US$95k, paying US$8.00 per share.

The good news, alongside the insider buying, for FNCB Bancorp bulls is that insiders (collectively) have a meaningful investment in the stock. To be specific, they have US$30m worth of shares. That's a lot of money, and no small incentive to work hard. That amounts to 18% of the company, demonstrating a degree of high-level alignment with shareholders.

While insiders are apparently happy to hold and accumulate shares, that is just part of the pretty picture. The cherry on top is that the CEO, Jerry Champi is paid comparatively modestly to CEOs at similar sized companies. I discovered that the median total compensation for the CEOs of companies like FNCB Bancorp with market caps between US$100m and US$400m is about US$1.5m.

FNCB Bancorp offered total compensation worth US$820k to its CEO in the year to . That comes in below the average for similar sized companies, and seems pretty reasonable to me. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. I'd also argue reasonable pay levels attest to good decision making more generally.

Is FNCB Bancorp Worth Keeping An Eye On?

As I already mentioned, FNCB Bancorp is a growing business, which is what I like to see. Better yet, insiders are significant shareholders, and have been buying more shares. That makes the company a prime candidate for my watchlist - and arguably a research priority. However, before you get too excited we've discovered 1 warning sign for FNCB Bancorp that you should be aware of.

As a growth investor I do like to see insider buying. But FNCB Bancorp isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:FNCB

FNCB Bancorp

Operates as the bank holding company for FNCB Bank that provides retail and commercial banking services to individuals, businesses, local governments, and municipalities in the United States.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor