Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:CATC

Increases to CEO Compensation Might Be Put On Hold For Now at Cambridge Bancorp (NASDAQ:CATC)

Performance at Cambridge Bancorp (NASDAQ:CATC) has been reasonably good and CEO Denis Sheahan has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 17 May 2021. However, some shareholders may still want to keep CEO compensation within reason.

See our latest analysis for Cambridge Bancorp

Comparing Cambridge Bancorp's CEO Compensation With the industry

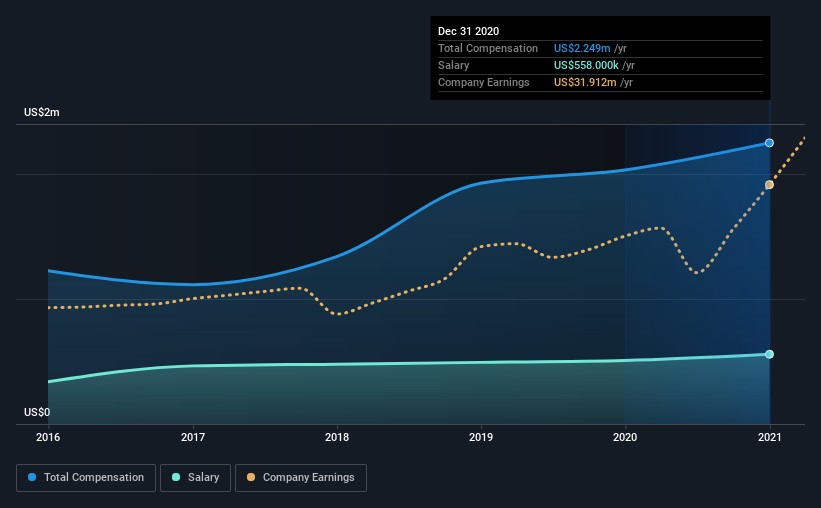

Our data indicates that Cambridge Bancorp has a market capitalization of US$604m, and total annual CEO compensation was reported as US$2.2m for the year to December 2020. That's a notable increase of 11% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$558k.

In comparison with other companies in the industry with market capitalizations ranging from US$400m to US$1.6b, the reported median CEO total compensation was US$1.5m. Accordingly, our analysis reveals that Cambridge Bancorp pays Denis Sheahan north of the industry median. Moreover, Denis Sheahan also holds US$3.2m worth of Cambridge Bancorp stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$558k | US$508k | 25% |

| Other | US$1.7m | US$1.5m | 75% |

| Total Compensation | US$2.2m | US$2.0m | 100% |

On an industry level, roughly 42% of total compensation represents salary and 58% is other remuneration. It's interesting to note that Cambridge Bancorp allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Cambridge Bancorp's Growth Numbers

Cambridge Bancorp's earnings per share (EPS) grew 13% per year over the last three years. In the last year, its revenue is up 32%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Cambridge Bancorp Been A Good Investment?

Cambridge Bancorp has generated a total shareholder return of 8.2% over three years, so most shareholders wouldn't be too disappointed. Although, there's always room to improve. Accordingly, a proposal to increase CEO remuneration without seeing an improvement in shareholder returns might not be met favorably by most shareholders.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Cambridge Bancorp that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you decide to trade Cambridge Bancorp, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:CATC

Cambridge Bancorp

Operates as the bank holding company for Cambridge Trust Company that engages in the provision of commercial and consumer banking, and investment management and trust services.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor