Advertisement

- United States

- /

- Banks

- /

- NasdaqCM:BFC

Is It Smart To Buy Bank First Corporation (NASDAQ:BFC) Before It Goes Ex-Dividend?

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Bank First Corporation (NASDAQ:BFC) is about to go ex-dividend in just 3 days. Ex-dividend means that investors that purchase the stock on or after the 22nd of December will not receive this dividend, which will be paid on the 6th of January.

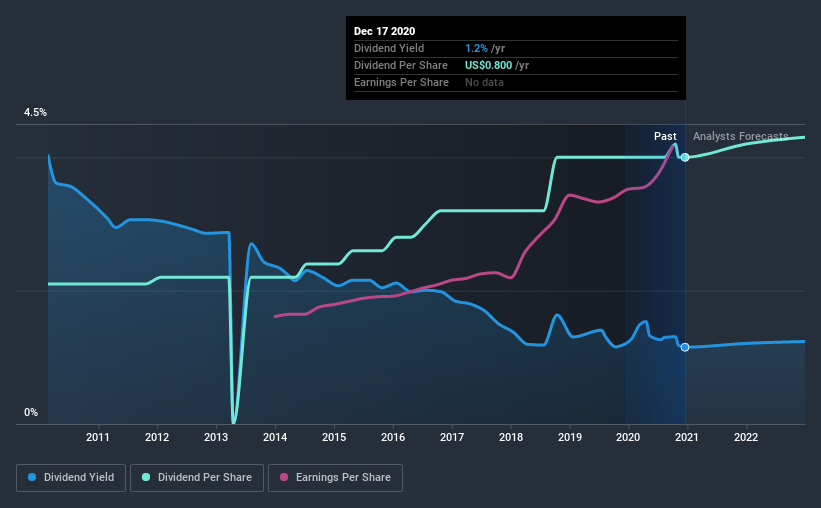

Bank First's next dividend payment will be US$0.21 per share, and in the last 12 months, the company paid a total of US$0.84 per share. Last year's total dividend payments show that Bank First has a trailing yield of 1.2% on the current share price of $69.48. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Bank First

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Bank First paid out just 17% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, Bank First's earnings per share have been growing at 18% a year for the past five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Bank First has delivered an average of 6.7% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Should investors buy Bank First for the upcoming dividend? Typically, companies that are growing rapidly and paying out a low fraction of earnings are keeping the profits for reinvestment in the business. This is one of the most attractive investment combinations under this analysis, as it can create substantial value for investors over the long run. In summary, Bank First appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

While it's tempting to invest in Bank First for the dividends alone, you should always be mindful of the risks involved. For example, we've found 3 warning signs for Bank First (1 shouldn't be ignored!) that deserve your attention before investing in the shares.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Bank First, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bank First might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqCM:BFC

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor