If you have been tracking Winnebago Industries (NYSE:WGO), two headlines this week might be prompting a fresh look at its shares. The company just announced a 3% bump to its quarterly dividend along with an overhaul of its executive leadership structure, introducing new group leader roles and broader responsibilities across its core segments. Management says these moves are designed to position Winnebago for its next phase of growth in the premium outdoor recreation market. For investors wondering whether these signals should prompt action, both the dividend hike and changes in the executive team seem intended to reinforce stability while preparing for potential expansion.

This update comes after a year that required resilience from shareholders. Despite leadership’s positive tone, Winnebago’s stock is down 38% over the last year, with losses extending across multiple timeframes. Shares did see a mid-summer lift, rising nearly 15% over the month, which may reflect renewed hope for a turnaround as the new leadership structure and dividend boost take effect. Still, market momentum has mostly lagged behind peers and the broader indexes. Recent events, from softer recreational vehicle demand to shifting consumer confidence, have kept investors cautious on the sector even as the company works to reset expectations.

With management signaling its readiness for growth and a freshly raised dividend, the question remains whether the market is still overlooking value here or if the recent uptick is simply pricing in optimistic expectations.

Advertisement

Most Popular Narrative: 4.8% Undervalued

According to community narrative, Winnebago Industries is seen as moderately undervalued, with analysts expecting future growth and margin improvements to support a higher fair value than today's price.

The successful launch and ramp-up of the Grand Design Motorhome Lineage lineup, including new models like the Series M Class C, Series F Super C Coach, and Series VT Class B, is expected to boost future revenues and market share in the motorized RV segment. The strategic transformation of Winnebago Towables under new leadership, with a focus on innovative pricing and product strategies, aims to increase market share and drive revenue growth in the competitive towables market.

Curious about what is fueling this valuation? There is a bold projection at the heart of this narrative, hinging on ambitious growth and a future earnings turnaround rarely seen in this sector. Want to know which financial milestones and strategic bets could propel Winnebago well above the current price? The details might surprise you.

However, persistent inflationary pressures and cautious consumer demand could challenge Winnebago’s growth. These factors may potentially limit both revenue gains and any turnaround in sentiment.

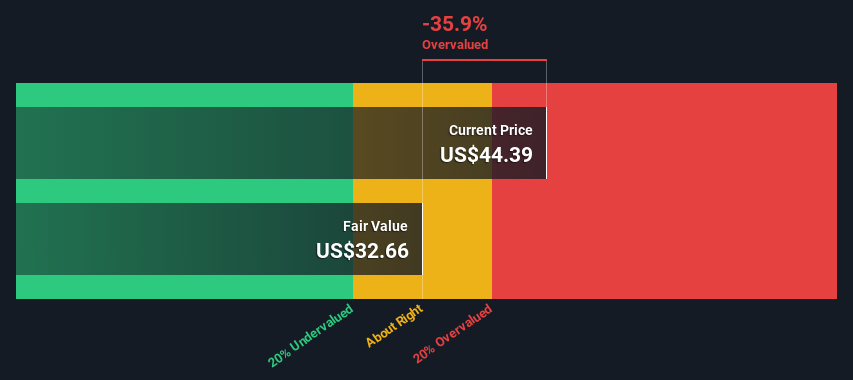

But when stepping back from analyst price targets, our DCF model offers a very different perspective and evaluates Winnebago's future cash flows in a less favorable light. In fact, this approach suggests the stock is significantly overvalued at the moment. Which perspective will the market adopt as new information comes to light?

If you see things differently or want to dig deeper into the numbers, you can build your own perspective in just a few minutes: do it your way.

A great starting point for your Winnebago Industries research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more timely stock ideas?

Don’t let your next opportunity slip past you. The Simply Wall Street Screener unlocks hidden gems and smart investment angles for every type of investor. Give yourself an edge in today’s market by using these tools to uncover what others might overlook:

Boost your passive income and secure your future by targeting companies with yields above 3% through this selection of dividend stocks with yields > 3%.

Jump ahead in the tech evolution by spotting top players among the most promising AI penny stocks in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Winnebago Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.