Advertisement

- United States

- /

- Auto Components

- /

- NYSE:LCII

LCI Industries (LCII) Is Up 12.9% After Strong Q3 Earnings, Raised Guidance and Major Buyback

Simply Wall St

Reviewed by Sasha Jovanovic

- LCI Industries recently reported its third quarter results, posting year-over-year increases in sales to US$1.04 billion and net income to US$62.49 million, while also completing a buyback of more than 1.05 million shares for US$100 million and raising sales guidance for October 2025.

- The combination of robust earnings growth, upbeat forward guidance, and substantial share repurchases highlights both operational momentum and management’s confidence in future prospects.

- We'll examine how LCI Industries' improving earnings and aggressive buyback activity could influence its long-term investment narrative.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

LCI Industries Investment Narrative Recap

To be a shareholder in LCI Industries, you need to believe in the long-term potential of the RV and outdoor recreation market, as well as the company’s ability to grow through both cycles and ongoing product innovation. The recent third quarter results, with strong sales and net income growth, an aggressive buyback, and raised sales guidance, support the case for near-term momentum. However, these positive updates do not fully address the risk that continued softness in RV demand or shifts in consumer preferences could pressure growth if retail demand does not normalize quickly.

Among all the latest announcements, the company’s updated sales guidance for October 2025, projecting a 15% year-over-year increase to about US$380 million, stands out. This forecast is especially relevant as it suggests management expects stronger retail activity and potentially improved dealer restocking, which directly ties into one of the largest short-term catalysts for the business. For shareholders, such upbeat guidance is encouraging and could be seen as a timely response to market headwinds.

Yet, what investors should not overlook is that, despite these operational wins, there is still a material risk tied to the RV cycle and...

Read the full narrative on LCI Industries (it's free!)

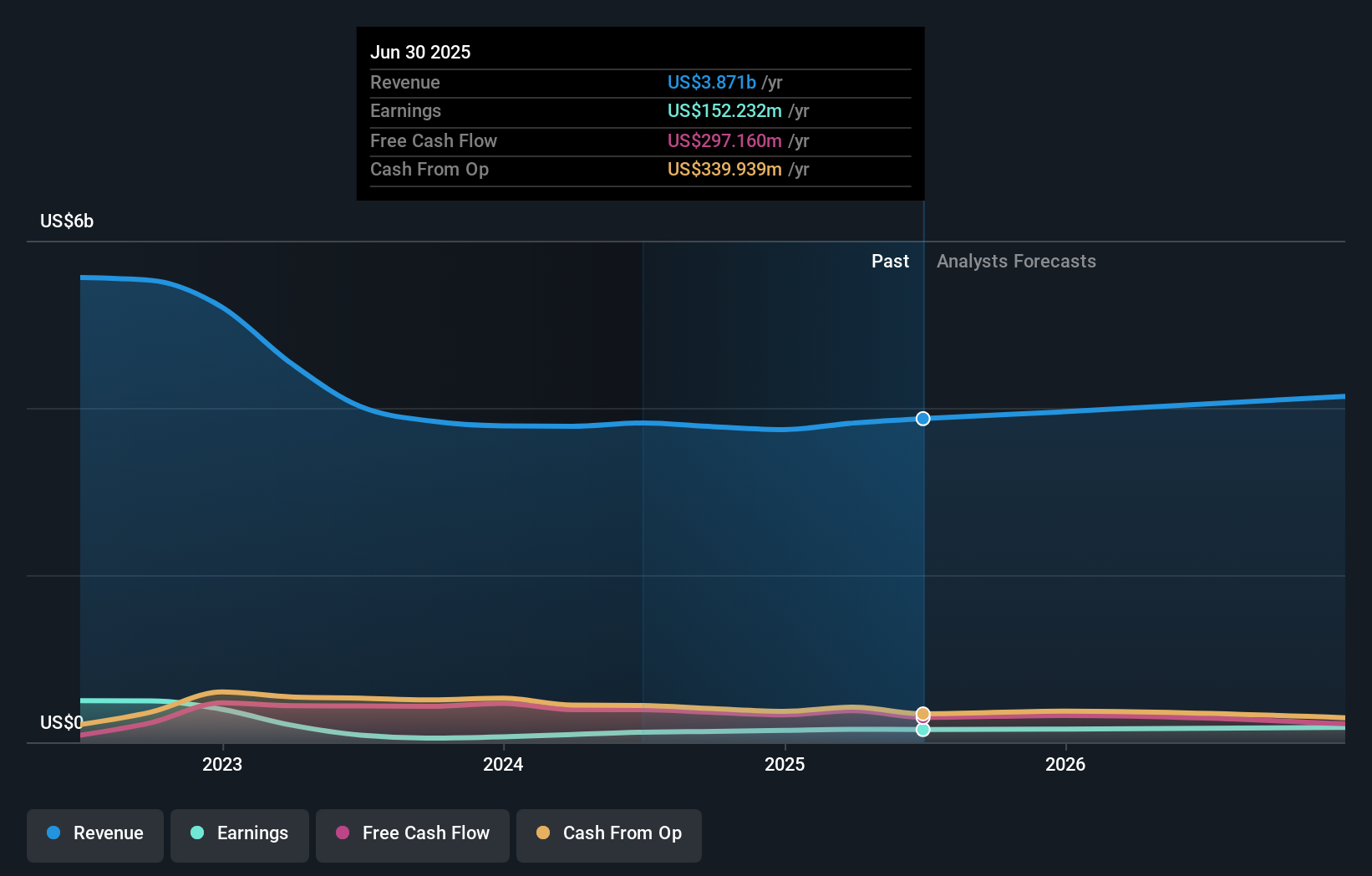

LCI Industries' narrative projects $4.4 billion revenue and $206.6 million earnings by 2028. This requires 4.5% yearly revenue growth and a $54.4 million earnings increase from $152.2 million currently.

Uncover how LCI Industries' forecasts yield a $109.78 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members see fair value for LCI Industries ranging from US$89.04 to US$109.78, based on two independent forecasts. While profit growth looks healthy, ongoing RV market reliance means future performance could still surprise, opinions really do vary, so compare these views for yourself.

Explore 2 other fair value estimates on LCI Industries - why the stock might be worth as much as $109.78!

Build Your Own LCI Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your LCI Industries research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free LCI Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate LCI Industries' overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LCII

LCI Industries

Manufactures and supplies engineered components for the manufacturers of recreational vehicles (RVs) and adjacent industries in the United States and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor