Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Innolux Corporation (TWSE:3481) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Innolux

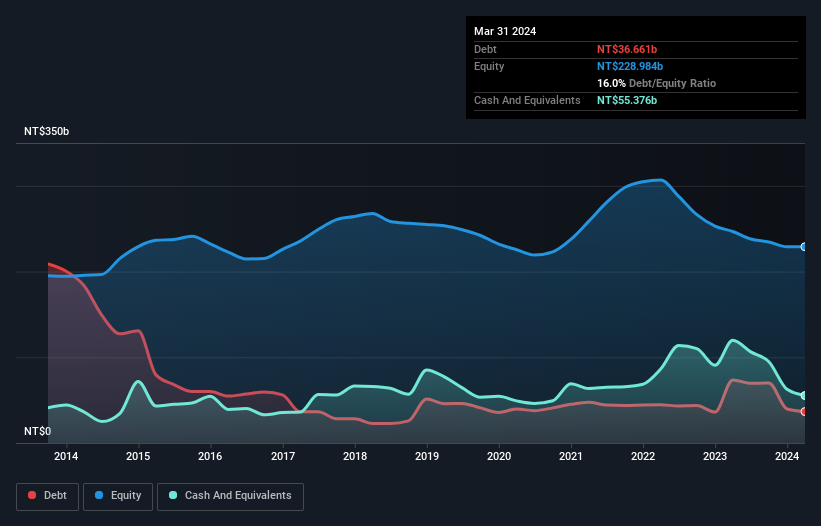

How Much Debt Does Innolux Carry?

As you can see below, Innolux had NT$36.7b of debt at March 2024, down from NT$73.6b a year prior. But it also has NT$55.4b in cash to offset that, meaning it has NT$18.7b net cash.

How Healthy Is Innolux's Balance Sheet?

According to the last reported balance sheet, Innolux had liabilities of NT$84.4b due within 12 months, and liabilities of NT$37.6b due beyond 12 months. On the other hand, it had cash of NT$55.4b and NT$32.5b worth of receivables due within a year. So it has liabilities totalling NT$34.1b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Innolux is worth NT$143.5b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Innolux also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Innolux can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Innolux wasn't profitable at an EBIT level, but managed to grow its revenue by 8.6%, to NT$217b. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Innolux?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Innolux lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of NT$9.2b and booked a NT$15b accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of NT$18.7b. That means it could keep spending at its current rate for more than two years. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for Innolux (1 shouldn't be ignored!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:3481

Innolux

Provides electronic components in Taiwan, Hong Kong, the United States, Europe, China, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor