Advertisement

- Hong Kong

- /

- Personal Products

- /

- SEHK:2367

Asian Market Value Stock Picks For Potential Capital Appreciation

Simply Wall St

Reviewed by Simply Wall St

As the Asian markets navigate a landscape marked by mixed performances and economic shifts, investors are closely watching for opportunities amid easing U.S.-China trade tensions and Japan's record stock market highs. In this context, identifying undervalued stocks with strong fundamentals can offer potential for capital appreciation, especially as regional economies adapt to evolving global conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xi'an International Medical Investment (SZSE:000516) | CN¥4.76 | CN¥9.38 | 49.3% |

| Visional (TSE:4194) | ¥9984.00 | ¥19579.10 | 49% |

| New Zealand King Salmon Investments (NZSE:NZK) | NZ$0.195 | NZ$0.39 | 49.5% |

| Meitu (SEHK:1357) | HK$8.80 | HK$17.19 | 48.8% |

| LianChuang Electronic TechnologyLtd (SZSE:002036) | CN¥10.08 | CN¥19.99 | 49.6% |

| Insource (TSE:6200) | ¥845.00 | ¥1665.99 | 49.3% |

| IbidenLtd (TSE:4062) | ¥13855.00 | ¥27366.14 | 49.4% |

| Guoquan Food (Shanghai) (SEHK:2517) | HK$4.00 | HK$7.97 | 49.8% |

| Chongqing Baiya Sanitary Products (SZSE:003006) | CN¥22.33 | CN¥44.01 | 49.3% |

| Alibaba Health Information Technology (SEHK:241) | HK$5.73 | HK$11.23 | 49% |

We're going to check out a few of the best picks from our screener tool.

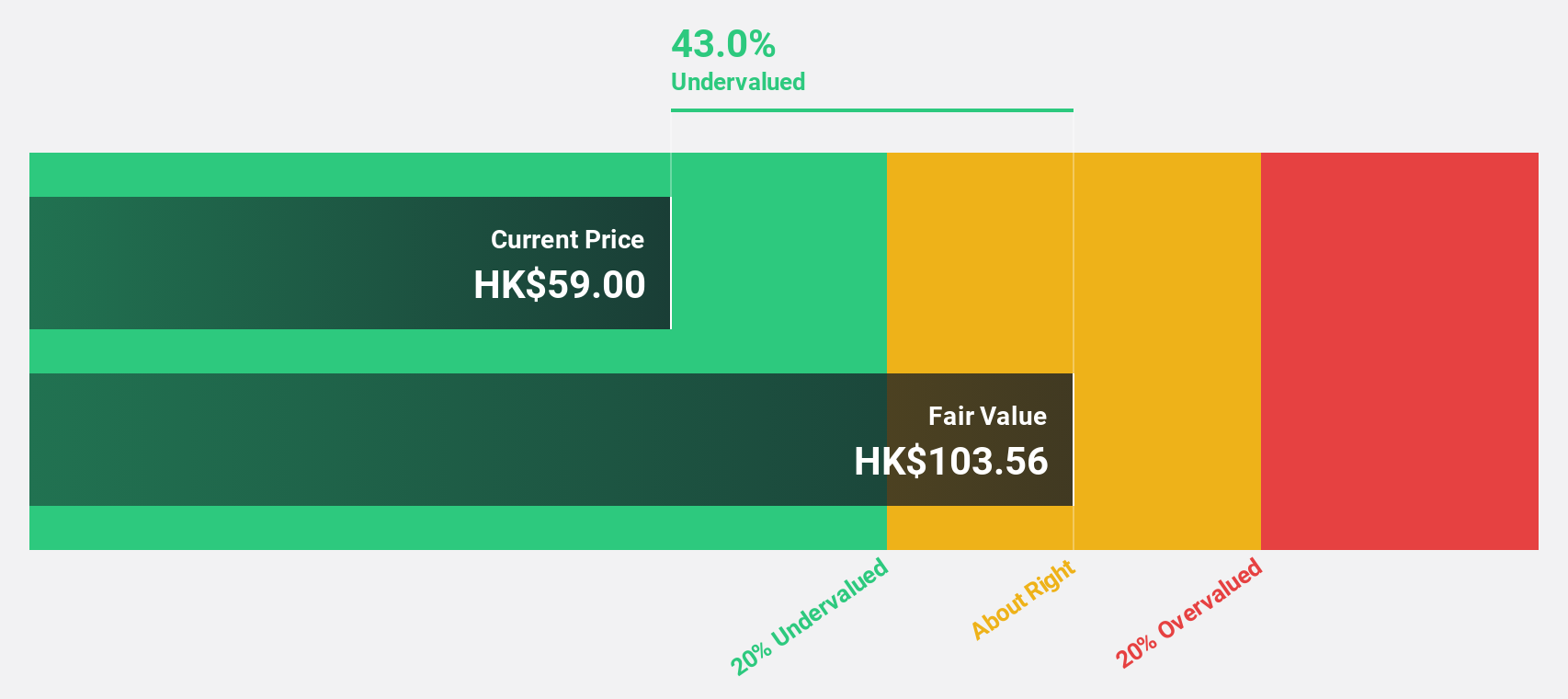

Giant Biogene Holding (SEHK:2367)

Overview: Giant Biogene Holding Co., Ltd. is an investment holding company that designs, develops, manufactures, and sells skin treatment products featuring recombinant collagen in the People's Republic of China, with a market cap of HK$40.87 billion.

Operations: The company's revenue primarily comes from its Personal Products segment, which generated CN¥6.11 billion.

Estimated Discount To Fair Value: 41.8%

Giant Biogene Holding appears undervalued, trading at 41.8% below its estimated fair value of HK$65.51, with a current price of HK$38.16. Recent earnings growth of 27.9% and projected annual profit growth of 17.1% outpace the Hong Kong market average, highlighting strong cash flow potential despite slower revenue growth forecasts at 18.2%. Analysts agree on an expected price rise by 83.4%, reinforcing its relative value compared to peers and industry standards.

- Our comprehensive growth report raises the possibility that Giant Biogene Holding is poised for substantial financial growth.

- Unlock comprehensive insights into our analysis of Giant Biogene Holding stock in this financial health report.

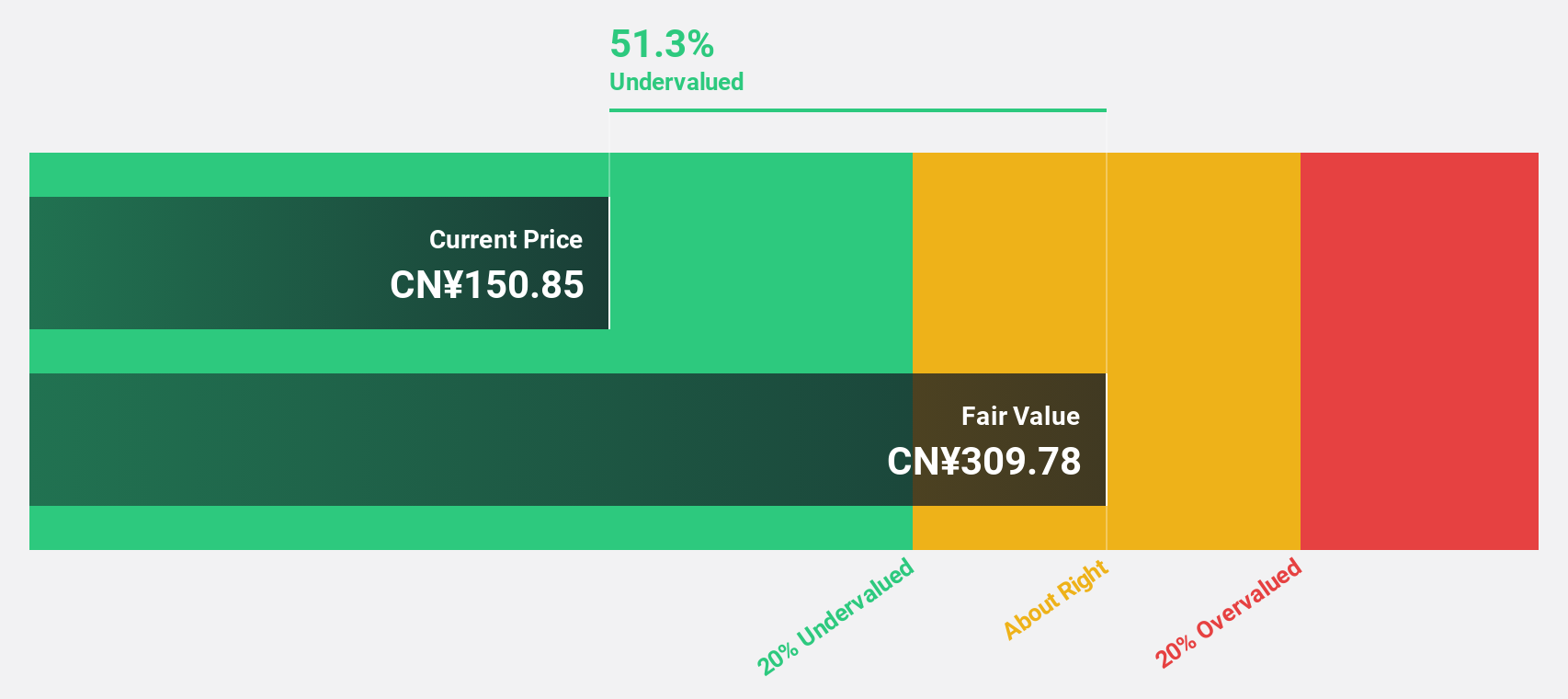

Xi'an NovaStar Tech (SZSE:301589)

Overview: Xi'an NovaStar Tech Co., Ltd. designs and develops LED display control solutions both in China and internationally, with a market cap of CN¥15.67 billion.

Operations: The company's revenue is primarily derived from the Video Image Display Control Industry, totaling CN¥3.32 billion.

Estimated Discount To Fair Value: 43.1%

Xi'an NovaStar Tech is trading at 43.1% below its estimated fair value of CNY 304.2, with a current price of CNY 173, highlighting its undervaluation based on cash flows. Despite recent net income declines, earnings are forecast to grow significantly at 29.3% annually, outpacing the Chinese market average and indicating strong future cash flow potential. However, return on equity is expected to be relatively low at 18% in three years.

- The growth report we've compiled suggests that Xi'an NovaStar Tech's future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Xi'an NovaStar Tech.

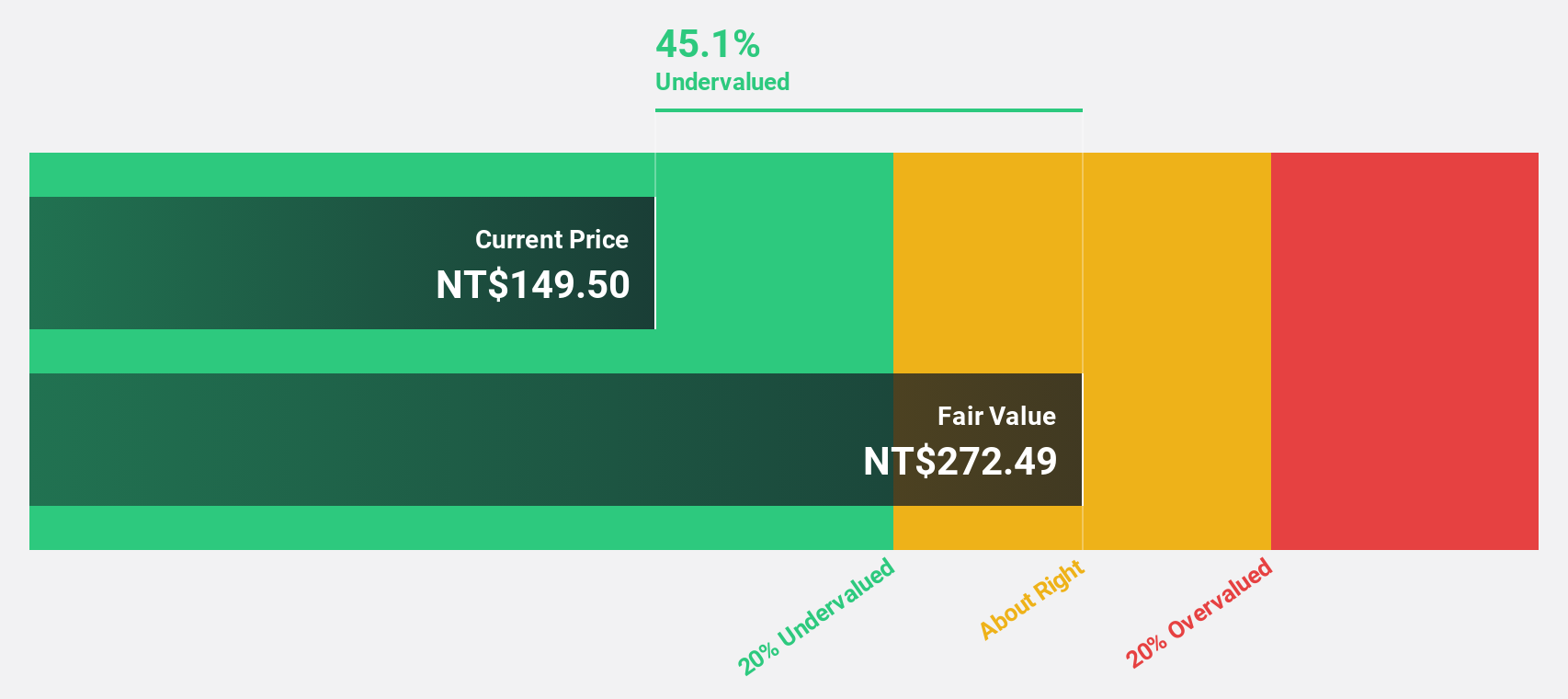

WT Microelectronics (TWSE:3036)

Overview: WT Microelectronics Co., Ltd. develops and sells electronic and communication components across the United States, Taiwan, China, and other international markets with a market cap of NT$172.73 billion.

Operations: The company's revenue segments include electronic and communication components sales in the United States, Taiwan, China, and other international markets.

Estimated Discount To Fair Value: 43.8%

WT Microelectronics is trading at NT$154, significantly below its estimated fair value of NT$274.12, highlighting its undervaluation based on cash flows. Recent earnings reports show strong performance with net income for Q3 2025 at NT$3.82 billion, up from NT$2.84 billion the previous year. Earnings are projected to grow significantly by 26.9% annually, surpassing Taiwan's market average growth rate and indicating robust future cash flow potential despite high debt levels and modest return on equity forecasts of 16.7%.

- Insights from our recent growth report point to a promising forecast for WT Microelectronics' business outlook.

- Dive into the specifics of WT Microelectronics here with our thorough financial health report.

Key Takeaways

- Unlock more gems! Our Undervalued Asian Stocks Based On Cash Flows screener has unearthed 276 more companies for you to explore.Click here to unveil our expertly curated list of 279 Undervalued Asian Stocks Based On Cash Flows.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2367

Giant Biogene Holding

An investment holding company, designs, develops, manufactures, and sells skin treatment products with recombinant collagen in the People’s Republic of China.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor