Advertisement

- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:3659

Is Bison Electronics (GTSM:3659) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Bison Electronics Inc. (GTSM:3659) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Bison Electronics

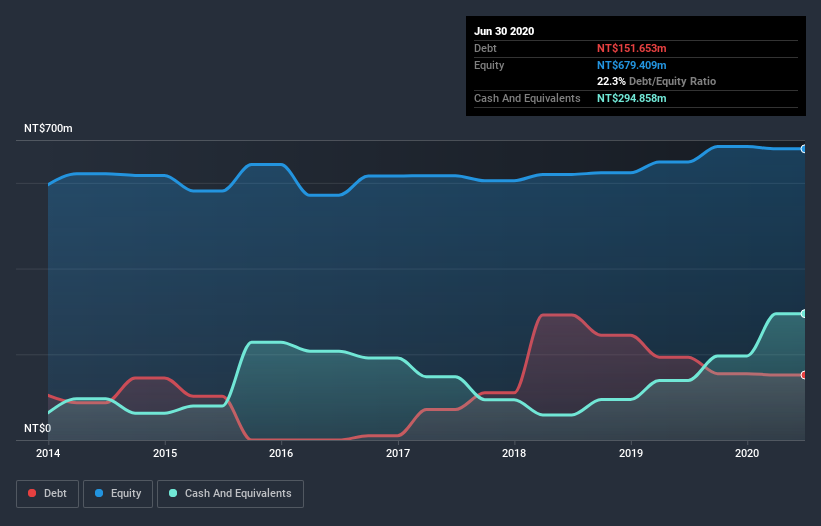

What Is Bison Electronics's Debt?

As you can see below, Bison Electronics had NT$151.7m of debt at June 2020, down from NT$193.3m a year prior. But on the other hand it also has NT$294.9m in cash, leading to a NT$143.2m net cash position.

How Healthy Is Bison Electronics's Balance Sheet?

We can see from the most recent balance sheet that Bison Electronics had liabilities of NT$575.7m falling due within a year, and liabilities of NT$163.0m due beyond that. Offsetting these obligations, it had cash of NT$294.9m as well as receivables valued at NT$392.4m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by NT$51.4m.

Since publicly traded Bison Electronics shares are worth a total of NT$664.2m, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Bison Electronics boasts net cash, so it's fair to say it does not have a heavy debt load!

Better yet, Bison Electronics grew its EBIT by 103% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Bison Electronics's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Bison Electronics has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Bison Electronics produced sturdy free cash flow equating to 55% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Bison Electronics has NT$143.2m in net cash. And we liked the look of last year's 103% year-on-year EBIT growth. So we don't think Bison Electronics's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - Bison Electronics has 2 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Bison Electronics, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bison Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:3659

Bison Electronics

Together with its subsidiary, Kunshan BaiChuang Optoelectronics Co., Ltd, engages in the sale of camera modules to computer manufacturers in Mainland China, Taiwan, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$471.5% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9718.0% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.250.9% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KL

Klim on Minera Alamos ·

Minera Alamos: Proven Earnings With Growth Still To Prove

Fair Value:CA$8.120.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KL

Klim on Zoomd Technologies ·

Zoomd: A Recovery Trade, Not A Growth Story

Fair Value:CA$1.2165.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

122 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9718.0% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative