- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:3512

Huang Long DevelopmentLtd (GTSM:3512) Takes On Some Risk With Its Use Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Huang Long Development Co.,Ltd. (GTSM:3512) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Huang Long DevelopmentLtd

How Much Debt Does Huang Long DevelopmentLtd Carry?

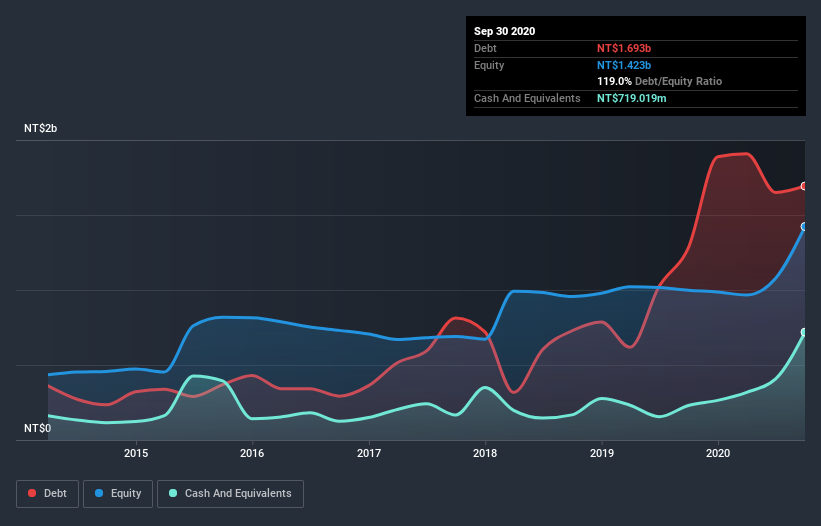

The image below, which you can click on for greater detail, shows that at September 2020 Huang Long DevelopmentLtd had debt of NT$1.69b, up from NT$1.28b in one year. On the flip side, it has NT$719.0m in cash leading to net debt of about NT$974.2m.

How Strong Is Huang Long DevelopmentLtd's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Huang Long DevelopmentLtd had liabilities of NT$3.09b due within 12 months and liabilities of NT$28.9m due beyond that. Offsetting these obligations, it had cash of NT$719.0m as well as receivables valued at NT$387.6m due within 12 months. So its liabilities total NT$2.01b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of NT$2.56b, so it does suggest shareholders should keep an eye on Huang Long DevelopmentLtd's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Strangely Huang Long DevelopmentLtd has a sky high EBITDA ratio of 6.7, implying high debt, but a strong interest coverage of 35.1. This means that unless the company has access to very cheap debt, that interest expense will likely grow in the future. Notably, Huang Long DevelopmentLtd's EBIT launched higher than Elon Musk, gaining a whopping 215% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is Huang Long DevelopmentLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last two years, Huang Long DevelopmentLtd burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

While Huang Long DevelopmentLtd's conversion of EBIT to free cash flow has us nervous. To wit both its interest cover and EBIT growth rate were encouraging signs. Taking the abovementioned factors together we do think Huang Long DevelopmentLtd's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example Huang Long DevelopmentLtd has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade Huang Long DevelopmentLtd, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Huang Long DevelopmentLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:3512

Huang Long DevelopmentLtd

Produces and sells of electronic components and heatsinks in Taiwan, Mainland China, and internationally.

Medium-low risk with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)