Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:8150

ChipMOS TECHNOLOGIES INC.'s (TWSE:8150) Dismal Stock Performance Reflects Weak Fundamentals

ChipMOS TECHNOLOGIES (TWSE:8150) has had a rough month with its share price down 11%. To decide if this trend could continue, we decided to look at its weak fundamentals as they shape the long-term market trends. Particularly, we will be paying attention to ChipMOS TECHNOLOGIES' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for ChipMOS TECHNOLOGIES

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for ChipMOS TECHNOLOGIES is:

8.4% = NT$2.1b ÷ NT$25b (Based on the trailing twelve months to March 2024).

The 'return' is the yearly profit. That means that for every NT$1 worth of shareholders' equity, the company generated NT$0.08 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

ChipMOS TECHNOLOGIES' Earnings Growth And 8.4% ROE

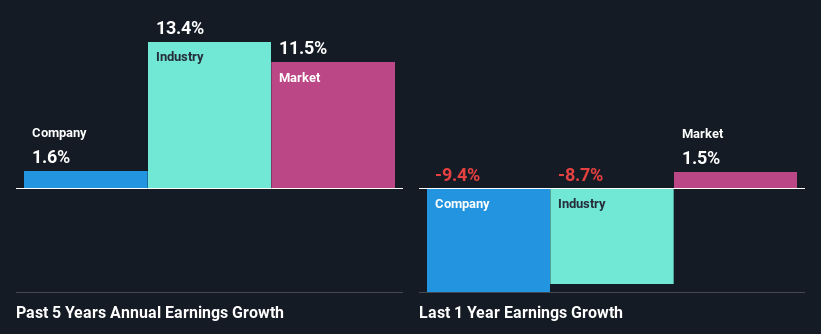

On the face of it, ChipMOS TECHNOLOGIES' ROE is not much to talk about. A quick further study shows that the company's ROE doesn't compare favorably to the industry average of 11% either. Therefore, ChipMOS TECHNOLOGIES' flat earnings over the past five years can possibly be explained by the low ROE amongst other factors.

We then compared ChipMOS TECHNOLOGIES' net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 13% in the same 5-year period, which is a bit concerning.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if ChipMOS TECHNOLOGIES is trading on a high P/E or a low P/E, relative to its industry.

Is ChipMOS TECHNOLOGIES Efficiently Re-investing Its Profits?

With a high three-year median payout ratio of 61% (implying that the company keeps only 39% of its income) of its business to reinvest into its business), most of ChipMOS TECHNOLOGIES' profits are being paid to shareholders, which explains the absence of growth in earnings.

In addition, ChipMOS TECHNOLOGIES has been paying dividends over a period of nine years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth.

Conclusion

On the whole, ChipMOS TECHNOLOGIES' performance is quite a big let-down. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:8150

ChipMOS TECHNOLOGIES

Engages in the research and development, manufacture, and sale of integrated circuits, and related assembly and testing services in Taiwan, Japan, the People’s Republic of China, Singapore, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor