Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:6789

VisEra Technologies Company Ltd. Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

Shareholders might have noticed that VisEra Technologies Company Ltd. (TWSE:6789) filed its second-quarter result this time last week. The early response was not positive, with shares down 3.8% to NT$304 in the past week. Revenues were NT$2.5b, approximately in line with whatthe analysts expected, although statutory earnings per share (EPS) crushed expectations, coming in at NT$1.33, an impressive 42% ahead of estimates. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on VisEra Technologies after the latest results.

See our latest analysis for VisEra Technologies

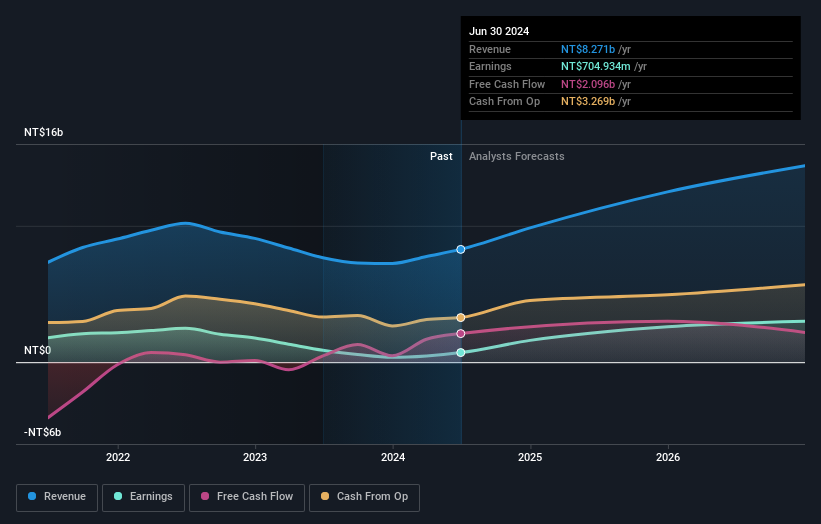

Taking into account the latest results, the current consensus from VisEra Technologies' two analysts is for revenues of NT$9.85b in 2024. This would reflect a meaningful 19% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to shoot up 127% to NT$5.06. Before this earnings report, the analysts had been forecasting revenues of NT$10.4b and earnings per share (EPS) of NT$4.84 in 2024. So it's pretty clear that while sentiment around revenues has declined following the latest results, the analysts are now more bullish on the company's earnings power.

The consensus price target fell 8.1% to NT$370, with the analysts signalling that the weaker revenue outlook was a more powerful indicator than the upgraded EPS forecasts.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. For example, we noticed that VisEra Technologies' rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 42% growth to the end of 2024 on an annualised basis. That is well above its historical decline of 4.7% a year over the past three years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 16% annually. Not only are VisEra Technologies' revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards VisEra Technologies following these results. They also downgraded VisEra Technologies' revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. Still, earnings are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for VisEra Technologies going out as far as 2026, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 1 warning sign for VisEra Technologies you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6789

VisEra Technologies

Manufactures and sells electronic spare parts in Taiwan, rest of Asia, Europe, and the United States.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor