Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:6515

WinWay Technology's (TWSE:6515) Shareholders Will Receive A Smaller Dividend Than Last Year

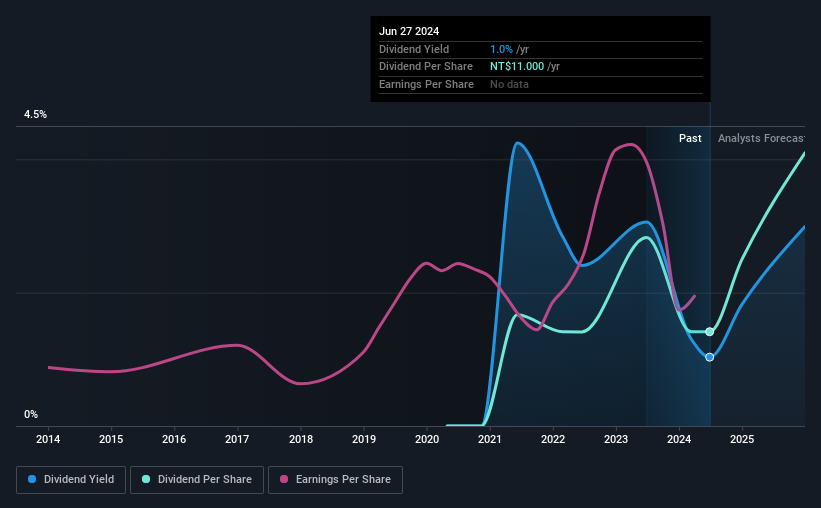

WinWay Technology Co., Ltd. (TWSE:6515) has announced that on 15th of August, it will be paying a dividend ofNT$11.00, which a reduction from last year's comparable dividend. This payment takes the dividend yield to 1.0%, which only provides a modest boost to overall returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that WinWay Technology's stock price has increased by 48% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

View our latest analysis for WinWay Technology

WinWay Technology's Payment Has Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. The last dividend made up quite a large portion of free cash flows, and this was made worse by the lack of free cash flows. Generally, we think that this would be a risky long term practice.

The next year is set to see EPS grow by 44.7%. Assuming the dividend continues along recent trends, we think the payout ratio could be 57% by next year, which is in a pretty sustainable range.

WinWay Technology's Dividend Has Lacked Consistency

Looking back, the dividend has been unstable but with a relatively short history, we think it may be a bit early to draw conclusions about long term dividend sustainability. Since 2021, the dividend has gone from NT$12.98 total annually to NT$11.00. This works out to be a decline of approximately 5.4% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

The Dividend Has Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. WinWay Technology has seen EPS rising for the last five years, at 5.4% per annum. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

In Summary

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. While WinWay Technology is earning enough to cover the payments, the cash flows are lacking. We don't think WinWay Technology is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, WinWay Technology has 3 warning signs (and 1 which is potentially serious) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if WinWay Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6515

WinWay Technology

Designs, processes, and sells optoelectronic product test fixtures, integrated circuit test interfaces, and fixtures and their components in Taiwan, the Americas, China, Asia, Europe, and Canada.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor