- Taiwan

- /

- Semiconductors

- /

- TWSE:2338

There May Be Reason For Hope In Taiwan Mask's (TWSE:2338) Disappointing Earnings

Soft earnings didn't appear to concern Taiwan Mask Corporation's (TWSE:2338) shareholders over the last week. We did some digging, and we believe the earnings are stronger than they seem.

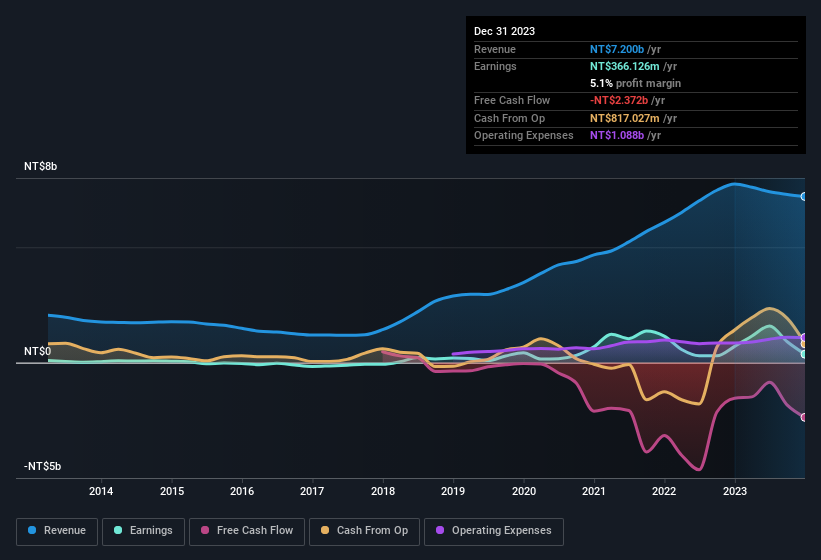

Check out our latest analysis for Taiwan Mask

Examining Cashflow Against Taiwan Mask's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to December 2023, Taiwan Mask recorded an accrual ratio of 0.20. Unfortunately, that means its free cash flow fell significantly short of its reported profits. In the last twelve months it actually had negative free cash flow, with an outflow of NT$2.4b despite its profit of NT$366.1m, mentioned above. We also note that Taiwan Mask's free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of NT$2.4b. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Taiwan Mask.

How Do Unusual Items Influence Profit?

Taiwan Mask's profit suffered from unusual items, which reduced profit by NT$94m in the last twelve months. In the case where this was a non-cash charge it would have made it easier to have high cash conversion, so it's surprising that the accrual ratio tells a different story. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Taiwan Mask to produce a higher profit next year, all else being equal.

Our Take On Taiwan Mask's Profit Performance

Taiwan Mask saw unusual items weigh on its profit, which should have made it easier to show high cash conversion, which it did not do, according to its accrual ratio. Given the contrasting considerations, we don't have a strong view as to whether Taiwan Mask's profits are an apt reflection of its underlying potential for profit. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Case in point: We've spotted 5 warning signs for Taiwan Mask you should be mindful of and 2 of these don't sit too well with us.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you're looking to trade Taiwan Mask, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Taiwan Mask might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2338

Taiwan Mask

Engages in the research, development, manufacturing, and sales of photomasks and integrated circuits for the semiconductor industry.

Second-rate dividend payer low.

Market Insights

Community Narratives