Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:6515

Exploring Suzhou Tianmai Thermal Technology And 2 Other Undiscovered Gems With Strong Potential

Simply Wall St

Reviewed by Simply Wall St

In a week marked by broad-based gains across major U.S. stock indexes, smaller-cap indices have notably outperformed their larger counterparts, signaling renewed investor interest in under-the-radar opportunities. As the market continues to navigate geopolitical tensions and economic indicators like jobless claims and home sales point toward underlying strength, identifying stocks with strong potential becomes crucial for investors seeking growth. In this context, exploring companies such as Suzhou Tianmai Thermal Technology can reveal promising prospects that align with current market dynamics.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Hubei Three Gorges Tourism Group | 11.32% | -9.98% | 7.95% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Uchida Yoko | 3.31% | 7.02% | 14.81% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Innovana Thinklabs | 6.09% | 12.62% | 20.18% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

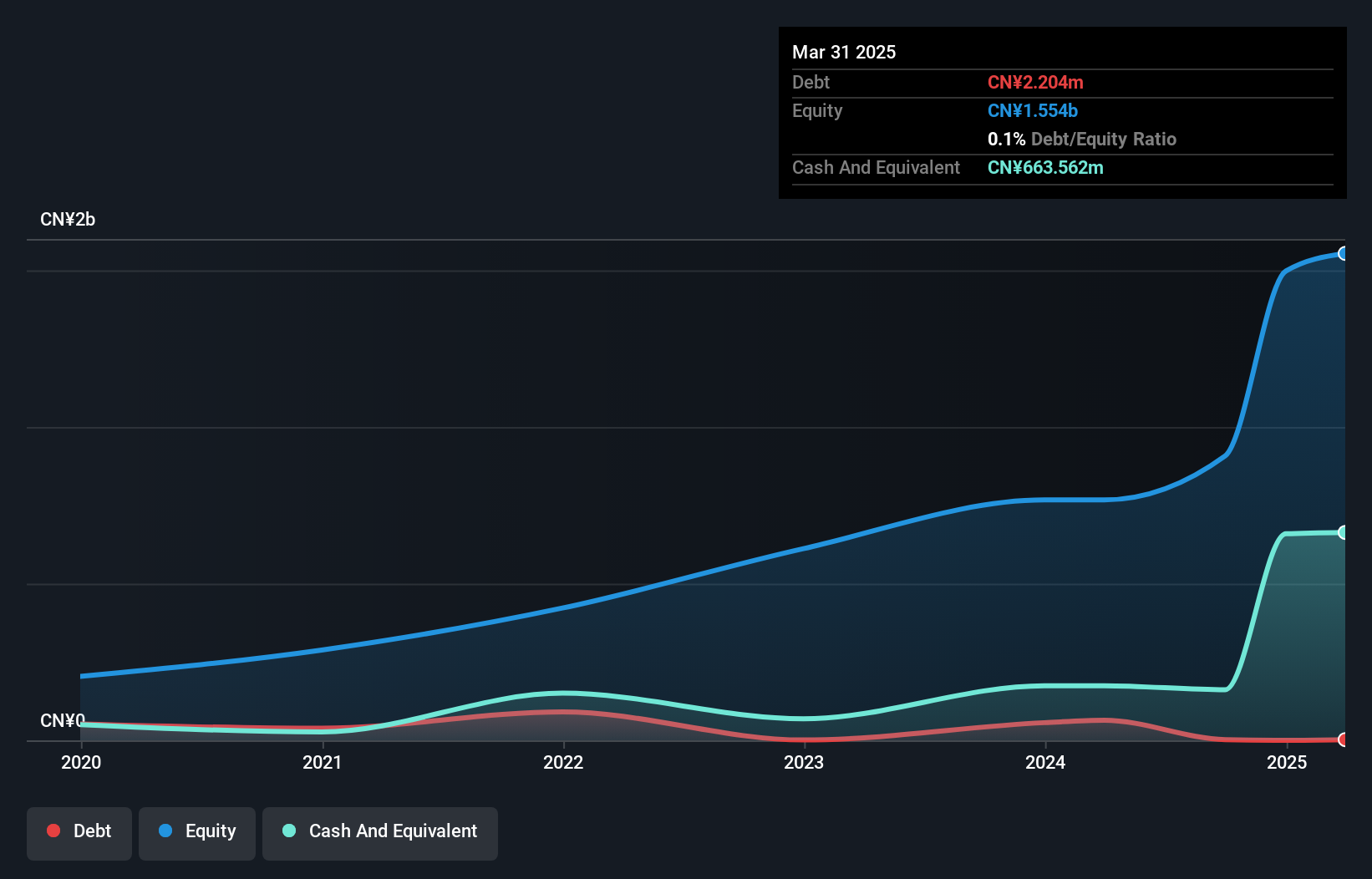

Suzhou Tianmai Thermal Technology (SZSE:301626)

Simply Wall St Value Rating: ★★★★★★

Overview: Suzhou Tianmai Thermal Technology Co., Ltd. specializes in the production of thermal management solutions and electronic components, with a market capitalization of CN¥12.61 billion.

Operations: The company generates revenue primarily from electronic components and parts, amounting to CN¥939.63 million.

Suzhou Tianmai Thermal Technology, a nimble player in its industry, has shown promising growth with earnings rising 28.7% over the past year, outpacing the broader electronics sector's 1.8%. Recent financials reveal net income for the nine months ending September 2024 at CNY 140.4 million, up from CNY 108.31 million last year, while basic earnings per share improved to CNY 1.62 from CNY 1.25. The company recently completed an IPO raising approximately CNY 613 million and was added to key indices like the Shenzhen Stock Exchange Composite Index, indicating increased market recognition and potential for further expansion.

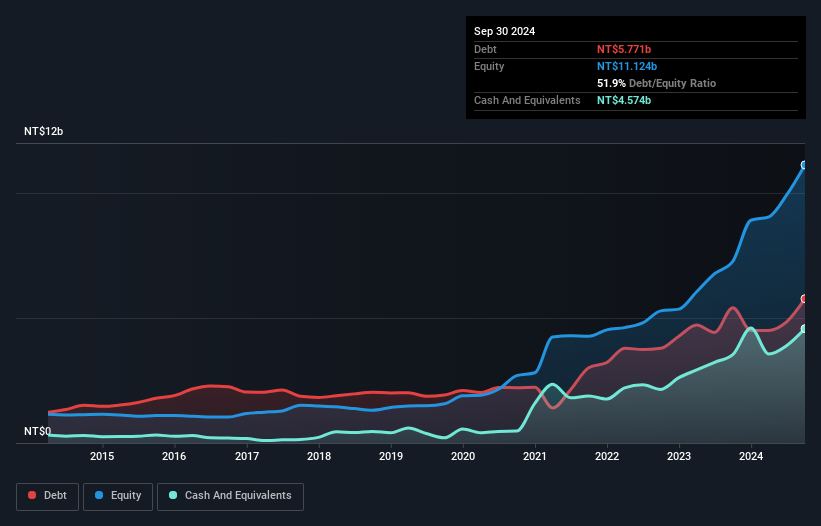

Gudeng Precision Industrial (TPEX:3680)

Simply Wall St Value Rating: ★★★★★☆

Overview: Gudeng Precision Industrial Co., Ltd. offers technology services on a global scale and has a market capitalization of NT$47.88 billion.

Operations: The company's revenue model is primarily driven by its technology services offered globally. Gross profit margin has shown variability, with recent figures indicating a trend worth noting. Operating costs and expenses play a significant role in shaping the overall financial performance.

Gudeng Precision Industrial has shown impressive growth, with earnings surging 31.9% in the past year, outpacing the semiconductor industry's 6%. The company reported third-quarter sales of TWD 1.89 billion, a significant jump from TWD 1.34 billion last year, while net income more than doubled to TWD 415 million from TWD 171 million. This performance is bolstered by a satisfactory net debt to equity ratio of just 7.5%, reflecting strong financial health and reduced leverage over five years from a high of 122.6%. Despite shareholder dilution recently, Gudeng's quality earnings and profitability offer promising potential in its sector.

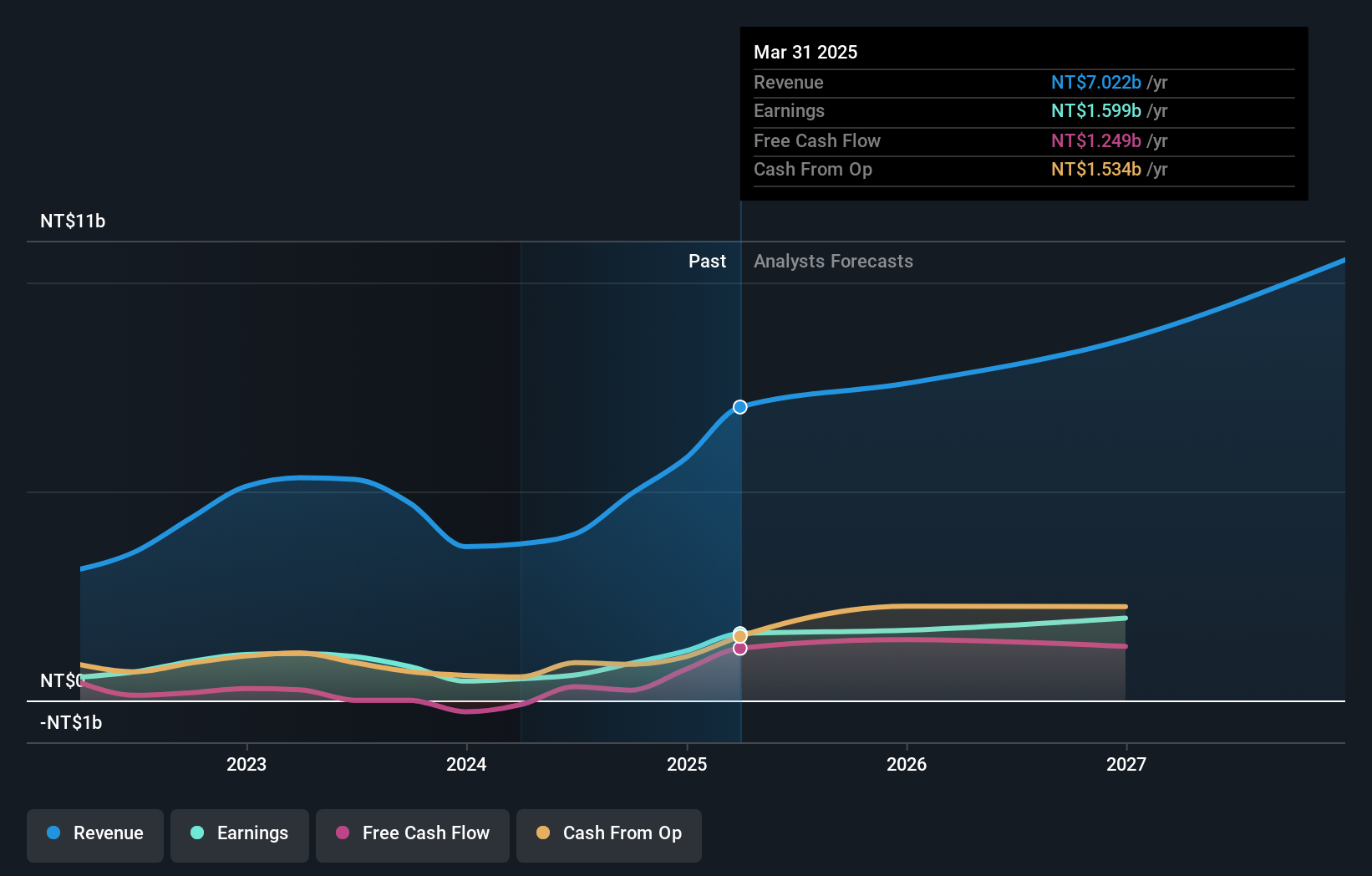

WinWay Technology (TWSE:6515)

Simply Wall St Value Rating: ★★★★★☆

Overview: WinWay Technology Co., Ltd. operates in the design, processing, and sale of optoelectronic product test fixtures and integrated circuit test interfaces across various regions including Taiwan, the Americas, China, Asia, Europe, and Canada with a market cap of NT$45.90 billion.

Operations: WinWay generates revenue primarily through the sale of optoelectronic product test fixtures and integrated circuit test interfaces. The company's net profit margin is a key financial metric to consider, reflecting its profitability after accounting for all expenses.

WinWay Technology, a nimble player in the semiconductor space, has shown impressive financial strides. Over the past year, earnings surged by 9.4%, outpacing industry growth of 6%. Its debt to equity ratio rose from 4.5% to 19.1% over five years, indicating increased leverage yet manageable due to higher cash reserves than total debt. Recently reported Q3 sales hit TWD 1,930 million compared to TWD 984 million last year with net income jumping from TWD 127 million to TWD 404 million. The company is expanding its footprint with a USD $2 million investment in Malaysia, aiming for stronger regional service delivery and customer engagement.

- Get an in-depth perspective on WinWay Technology's performance by reading our health report here.

Understand WinWay Technology's track record by examining our Past report.

Turning Ideas Into Actions

- Navigate through the entire inventory of 4629 Undiscovered Gems With Strong Fundamentals here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WinWay Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6515

WinWay Technology

Designs, processes, and sells optoelectronic product test fixtures, integrated circuit test interfaces, and fixtures and their components in Taiwan, the Americas, China, Asia, Europe, and Canada.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor