- Taiwan

- /

- Semiconductors

- /

- TPEX:3402

Undiscovered Gems To Explore In January 2025

Reviewed by Simply Wall St

As the global markets navigate mixed performances and economic indicators signal caution, small-cap stocks continue to attract attention with their potential for growth amidst broader market fluctuations. With indices like the Russell 2000 showing resilience, investors might find opportunities in lesser-known companies that demonstrate strong fundamentals and adaptability to current economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Mendelson Infrastructures & Industries | 32.64% | 6.72% | 15.39% | ★★★★★★ |

| Payton Industries | NA | 9.27% | 15.41% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

We'll examine a selection from our screener results.

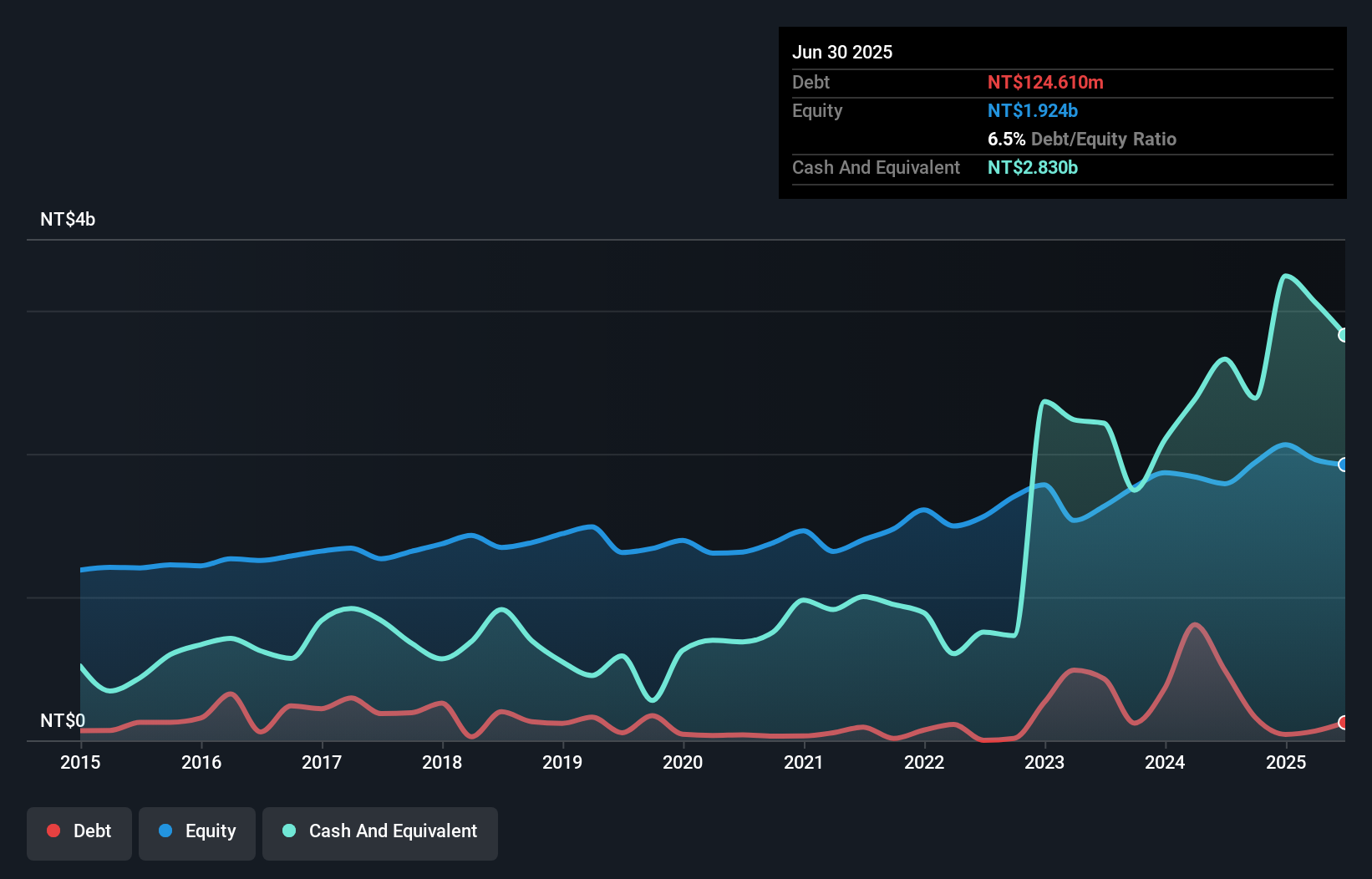

Wholetech System Hitech (TPEX:3402)

Simply Wall St Value Rating: ★★★★★★

Overview: Wholetech System Hitech Limited offers system integration services across Taiwan, China, and Singapore with a market capitalization of NT$8.33 billion.

Operations: Wholetech System Hitech generates revenue primarily from its equipment and construction segments, with the latter contributing significantly more at NT$4.77 billion compared to NT$723.40 million for equipment.

Wholetech System Hitech is gaining traction with impressive earnings growth of 26.1% over the past year, outpacing the semiconductor industry's 5.9%. The company has effectively reduced its debt to equity ratio from 12.8% to 8.3% in five years, signaling a healthier balance sheet. Recent earnings reveal net income for Q3 at TWD 128.79 million, up from TWD 113.4 million the previous year, while sales jumped to TWD 1,403.73 million from TWD 1,082.38 million a year ago; basic EPS increased to TWD 1.76 from TWD 1.55 last year, indicating robust financial health and potential for further growth.

- Take a closer look at Wholetech System Hitech's potential here in our health report.

Evaluate Wholetech System Hitech's historical performance by accessing our past performance report.

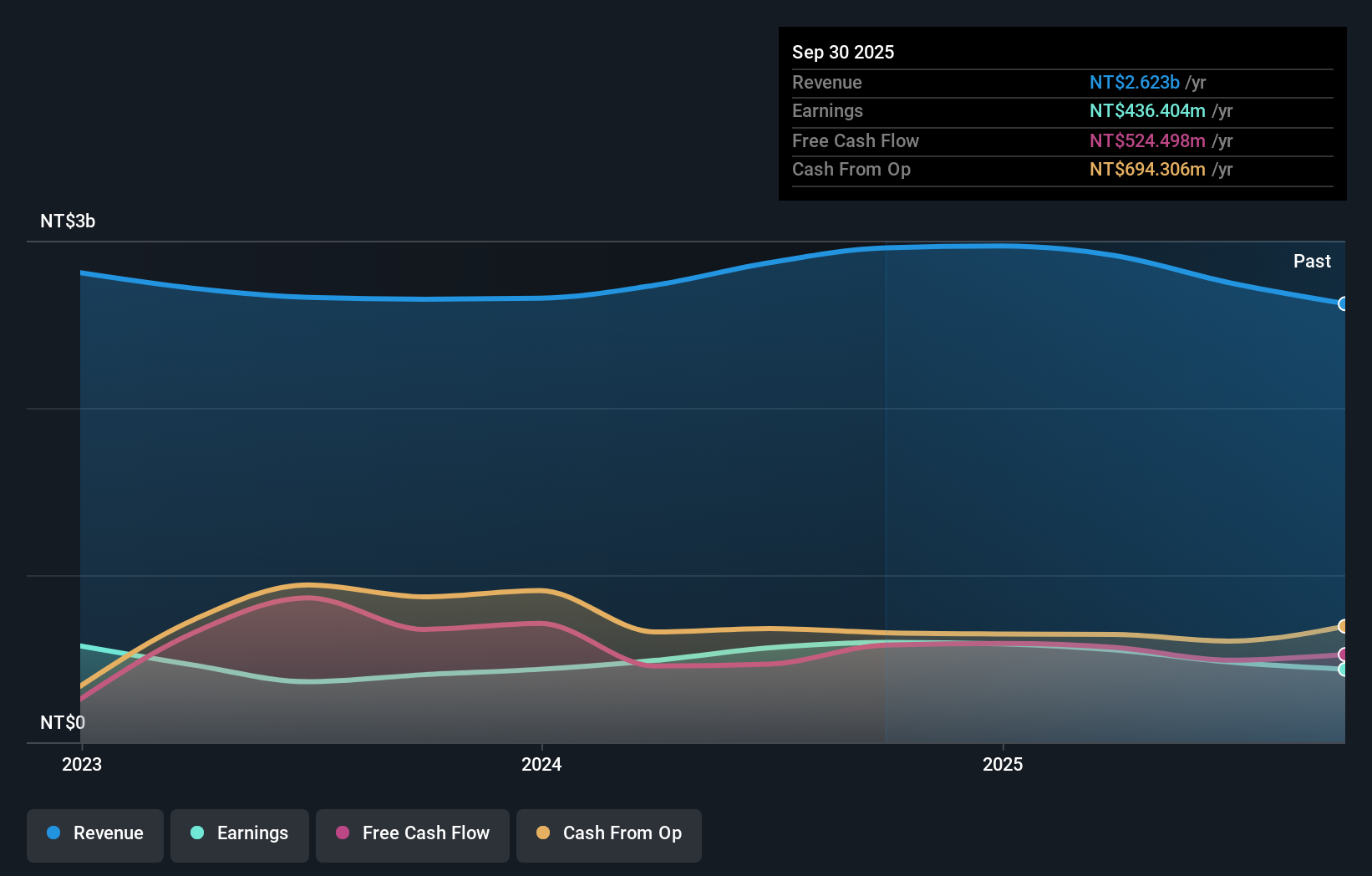

Forcelead Technology (TPEX:6996)

Simply Wall St Value Rating: ★★★★★★

Overview: Forcelead Technology Corp. is an IC design company focused on the research, development, and sale of display driver chips and touch integrated driver chips both in Taiwan and internationally, with a market cap of NT$9.46 billion.

Operations: Forcelead Technology generates revenue primarily from its semiconductor segment, amounting to NT$2.96 billion.

Forcelead Technology, a small player in the semiconductor industry, has shown impressive financial health with earnings growth of 47.7% over the past year, outpacing the industry's 5.9%. The company is debt-free and offers high-quality earnings, with a price-to-earnings ratio of 15.8x below Taiwan's market average of 20.8x. Recent quarterly results highlight sales at TWD 784 million and net income reaching TWD 165 million, both improved from last year’s figures. Earnings per share also rose to TWD 4.34 from TWD 3.49 previously, indicating robust operational performance and potential for continued growth in revenue forecasted at over 16% annually.

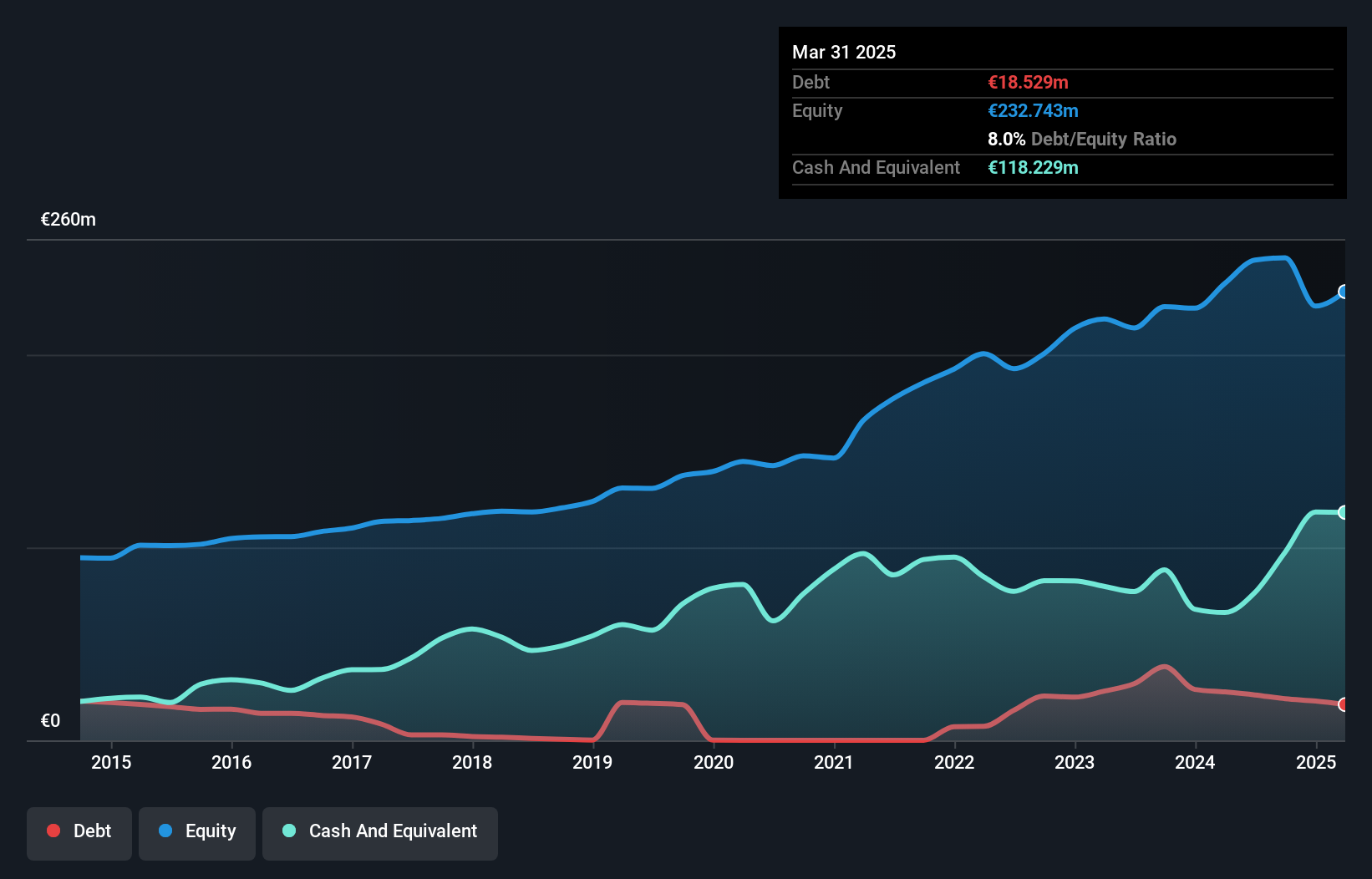

Eckert & Ziegler (XTRA:EUZ)

Simply Wall St Value Rating: ★★★★★★

Overview: Eckert & Ziegler SE specializes in the production and distribution of isotope technology components globally, with a market capitalization of approximately €900.94 million.

Operations: Eckert & Ziegler generates revenue primarily from its Medical and Isotope Products segments, with the latter contributing €150.79 million. The company faces a deduction of €10.70 million due to eliminations in its financial reporting.

Eckert & Ziegler, a notable player in isotope technology, has seen its debt to equity ratio improve from 13.5% to 8.6% over five years, indicating a stronger balance sheet. The company's earnings grew by 10.1% last year and are expected to continue rising at an annual rate of 5.16%. Despite net income dropping from €9.38 million to €5.35 million in the latest quarter, sales increased from €65.9 million to €70.11 million year-over-year, showcasing resilience amid challenges. Trading significantly below its fair value estimate by about 61%, Eckert & Ziegler remains an intriguing prospect for investors seeking undervalued opportunities in the medical equipment sector.

- Get an in-depth perspective on Eckert & Ziegler's performance by reading our health report here.

Explore historical data to track Eckert & Ziegler's performance over time in our Past section.

Where To Now?

- Take a closer look at our Undiscovered Gems With Strong Fundamentals list of 4667 companies by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wholetech System Hitech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:3402

Wholetech System Hitech

Provides system integration services in Taiwan, China, Japan, and Singapore.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion