Advertisement

- Taiwan

- /

- Retail Distributors

- /

- TWSE:1439

Ascent Development's (TWSE:1439) Solid Earnings May Rest On Weak Foundations

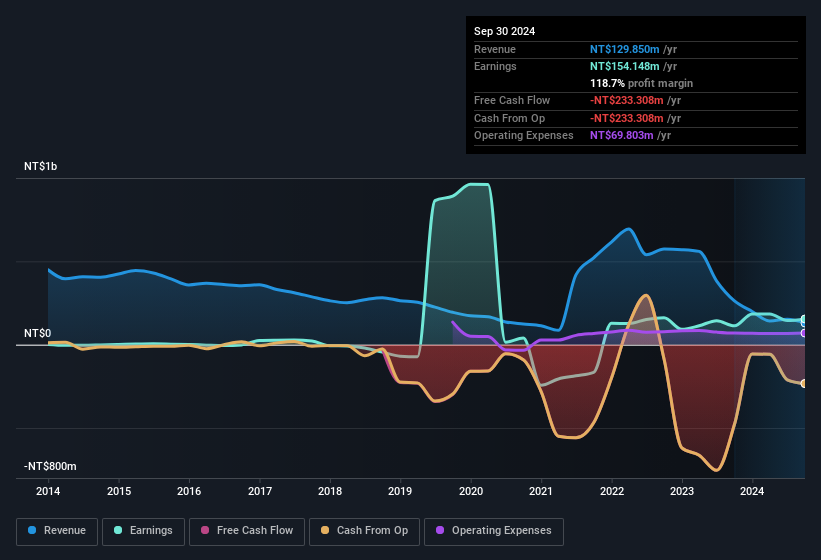

Ascent Development Co., Ltd.'s (TWSE:1439) healthy profit numbers didn't contain any surprises for investors. We believe that shareholders have noticed some concerning factors beyond the statutory profit numbers.

View our latest analysis for Ascent Development

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Ascent Development's profit received a boost of NT$12m in unusual items, over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And that's as you'd expect, given these boosts are described as 'unusual'. Ascent Development had a rather significant contribution from unusual items relative to its profit to September 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ascent Development.

Our Take On Ascent Development's Profit Performance

As we discussed above, we think the significant positive unusual item makes Ascent Development's earnings a poor guide to its underlying profitability. For this reason, we think that Ascent Development's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The good news is that, its earnings per share increased by 37% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you want to do dive deeper into Ascent Development, you'd also look into what risks it is currently facing. For instance, we've identified 3 warning signs for Ascent Development (1 shouldn't be ignored) you should be familiar with.

Today we've zoomed in on a single data point to better understand the nature of Ascent Development's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1439

Ascent Development

Sells wool tops, carbonized wool, scoured wool, shrink-resistant wool tops products in Taiwan.

Good value with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative