- Taiwan

- /

- Specialty Stores

- /

- TWSE:2207

Here's Why We Think Hotai MotorLtd (TPE:2207) Is Well Worth Watching

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Hotai MotorLtd (TPE:2207). Even if the shares are fully valued today, most capitalists would recognize its profits as the demonstration of steady value generation. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

See our latest analysis for Hotai MotorLtd

Hotai MotorLtd's Earnings Per Share Are Growing.

As one of my mentors once told me, share price follows earnings per share (EPS). It's no surprise, then, that I like to invest in companies with EPS growth. Over the last three years, Hotai MotorLtd has grown EPS by 8.7% per year. That's a pretty good rate, if the company can sustain it.

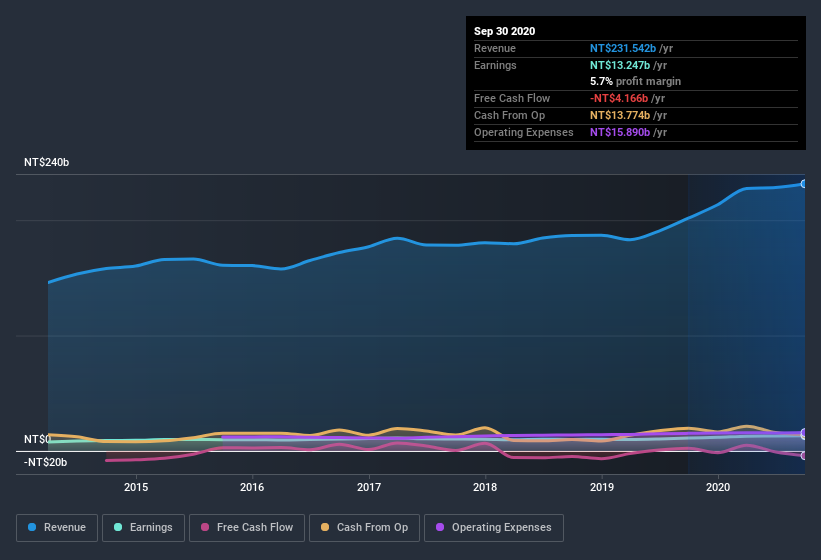

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). I note that Hotai MotorLtd's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. Hotai MotorLtd maintained stable EBIT margins over the last year, all while growing revenue 15% to NT$232b. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

While profitability drives the upside, prudent investors always check the balance sheet, too.

Are Hotai MotorLtd Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a NT$327b company like Hotai MotorLtd. But we do take comfort from the fact that they are investors in the company. Given insiders own a small fortune of shares, currently valued at NT$1.8b, they have plenty of motivation to push the business to succeed. That's certainly enough to make me think that management will be very focussed on long term growth.

Is Hotai MotorLtd Worth Keeping An Eye On?

As I already mentioned, Hotai MotorLtd is a growing business, which is what I like to see. If that's not enough on its own, there is also the rather notable levels of insider ownership. That combination appeals to me, for one. So yes, I do think the stock is worth keeping an eye on. We should say that we've discovered 1 warning sign for Hotai MotorLtd that you should be aware of before investing here.

Although Hotai MotorLtd certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

When trading Hotai MotorLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hotai MotorLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2207

Hotai MotorLtd

Hotai Motor Co.,Ltd., together with its subsidiaries, exports and imports, trades, and sells vehicles, automobile air conditioners, and related parts in Taiwan and Mainland China.

Proven track record with mediocre balance sheet.