Advertisement

- Taiwan

- /

- Real Estate

- /

- TWSE:2530

Delpha ConstructionLtd (TWSE:2530) Will Pay A Smaller Dividend Than Last Year

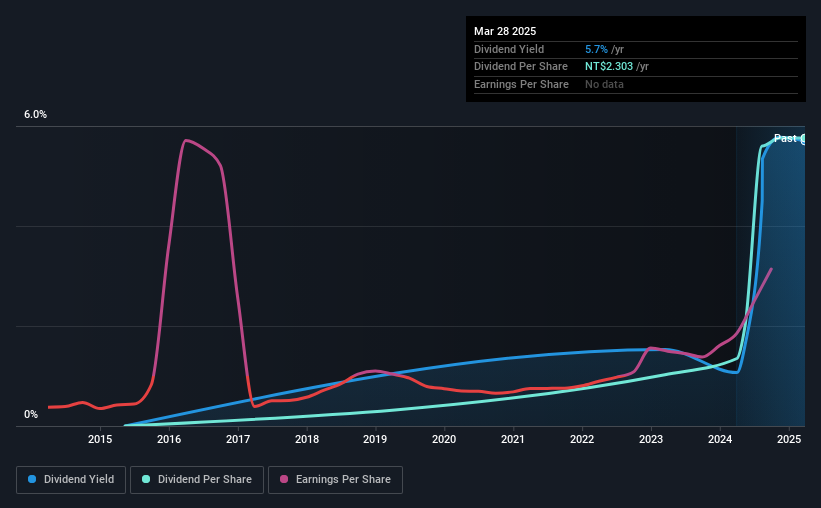

Delpha Construction Co.,Ltd. (TWSE:2530) is reducing its dividend from last year's comparable payment to NT$0.4192 on the 23rd of May. However, the dividend yield of 5.7% is still a decent boost to shareholder returns.

Delpha ConstructionLtd's Projected Earnings Seem Likely To Cover Future Distributions

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Prior to this announcement, Delpha ConstructionLtd's dividend was making up a very large proportion of earnings, and the company was also not generating any cash flow to offset this. We think that this practice can make the dividend quite risky in the future.

Over the next year, EPS could expand by 76.6% if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio will be 46%, which would make us comfortable with the sustainability of the dividend, despite the levels currently being quite high.

See our latest analysis for Delpha ConstructionLtd

Delpha ConstructionLtd Is Still Building Its Track Record

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. Since 2023, the annual payment back then was NT$0.411, compared to the most recent full-year payment of NT$2.3. This means that it has been growing its distributions at 137% per annum over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

Delpha ConstructionLtd's Dividend Might Lack Growth

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. We are encouraged to see that Delpha ConstructionLtd has grown earnings per share at 77% per year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which Delpha ConstructionLtd hasn't been doing.

The Dividend Could Prove To Be Unreliable

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. While we generally think the level of distributions are a bit high, we wouldn't rule it out as becoming a good dividend payer in the future as its earnings are growing healthily. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for Delpha ConstructionLtd (of which 1 makes us a bit uncomfortable!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2530

Delpha ConstructionLtd

Delpha Construction Co.,Ltd. constructs commercial buildings in Taiwan.

Fair value with acceptable track record.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets