Advertisement

- Taiwan

- /

- Tech Hardware

- /

- TPEX:3483

Discovering None's Hidden Gems with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets react to the policy uncertainties of the incoming Trump administration, small-cap stocks have experienced mixed performance, with indices like the Russell 2000 showing a decline. In this environment, identifying promising opportunities requires a focus on companies with strong fundamentals and potential resilience amid economic fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Transcorp Power | 46.33% | 114.79% | 152.92% | ★★★★★☆ |

| Thai Energy Storage Technology | 9.49% | -1.42% | 1.73% | ★★★★★☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

| Tethys Petroleum | NA | 29.98% | 44.48% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Shenzhen Uniconn Technology (SZSE:301631)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shenzhen Uniconn Technology Co., Ltd. focuses on the research, design, production, sale, and service of electrical connection components in China with a market cap of CN¥4.77 billion.

Operations: Shenzhen Uniconn Technology generates revenue primarily through the sale of electrical connection components. The company's cost structure includes expenses related to research, design, production, and sales activities. It has reported a gross profit margin of 35.4% in recent financial periods.

Shenzhen Uniconn Technology recently completed an IPO, raising CNY 1.19 billion, which could bolster its financial position. The company reported sales of CNY 3.07 billion and net income of CNY 259.89 million for the year ending December 2023, with basic earnings per share at CNY 5.31. Its net debt to equity ratio stands at a satisfactory level of 5.5%, indicating prudent financial management. Despite being illiquid, earnings growth over the past year reached an impressive 29.1%, outpacing the electrical industry average of just 0.8%. Trading significantly below estimated fair value suggests potential undervaluation opportunities for investors seeking growth prospects in this sector.

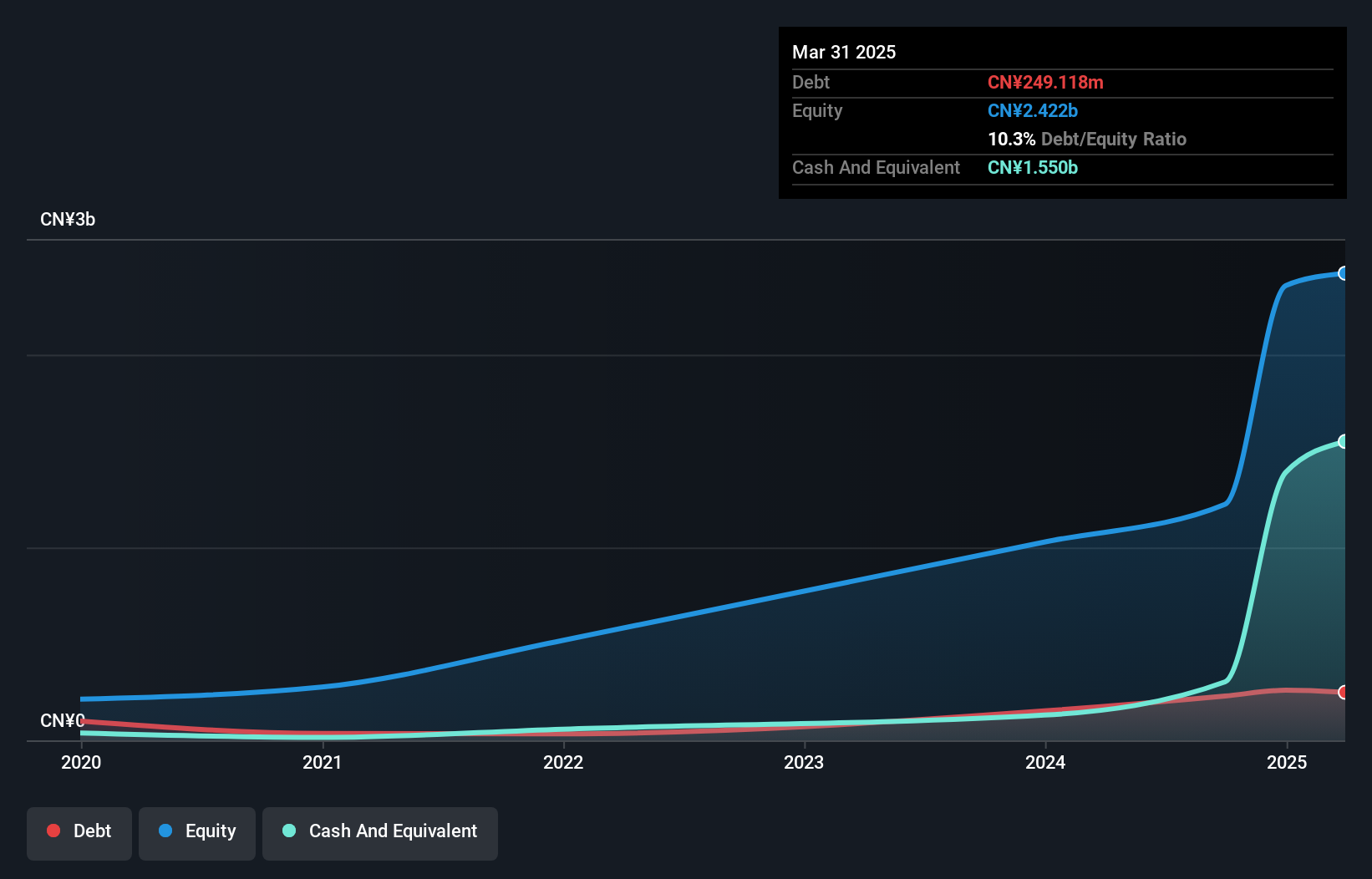

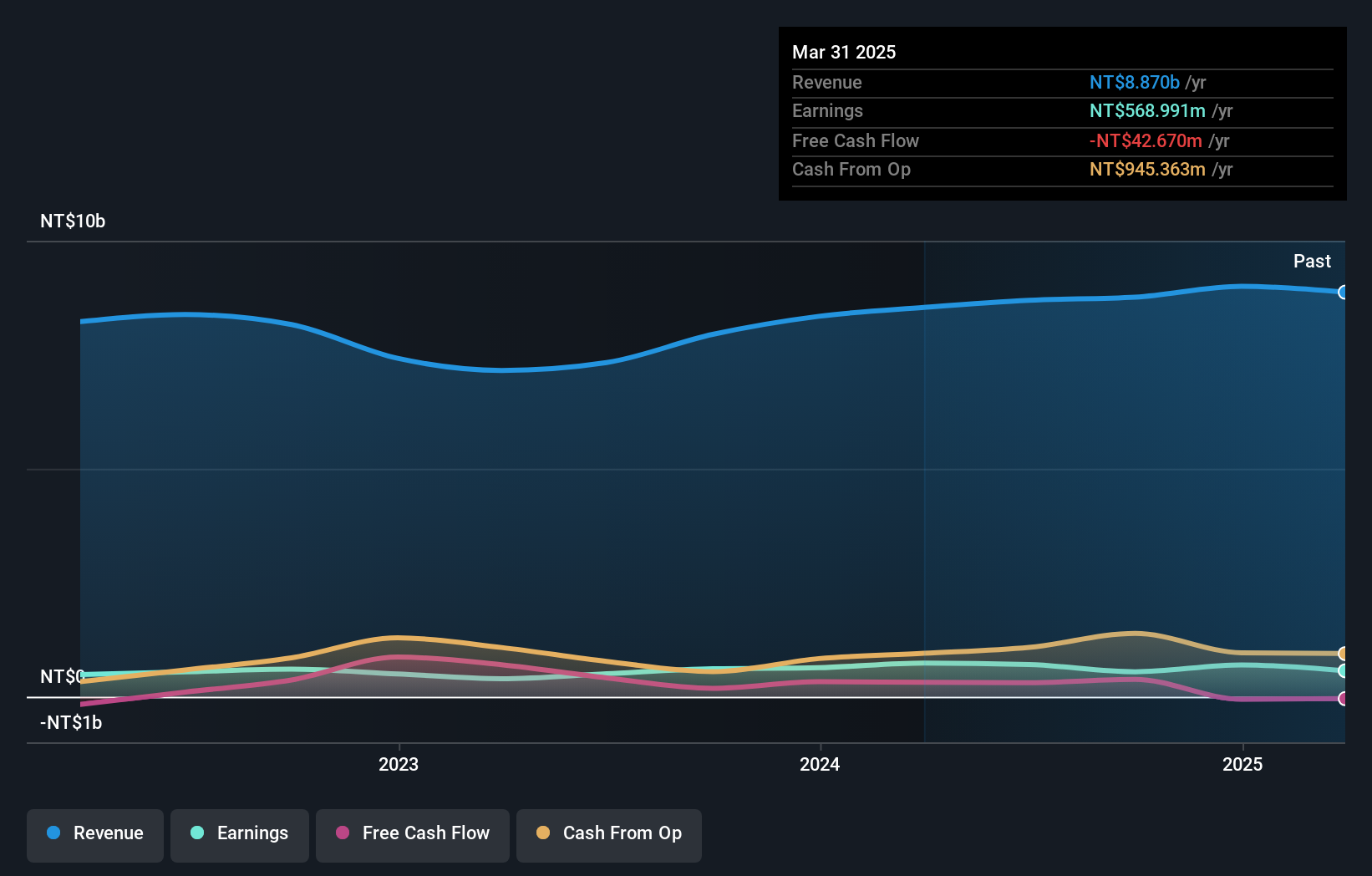

Forcecon Technology (TPEX:3483)

Simply Wall St Value Rating: ★★★★★★

Overview: Forcecon Technology Co., Ltd. focuses on the research, development, production, and sale of thermal management products in Taiwan and internationally, with a market cap of NT$13.23 billion.

Operations: Forcecon Technology generates revenue primarily from its subsidiaries, with significant contributions from Suzhou Juli Electric Motor Co., Ltd. (NT$5.43 billion) and Chongqing Liyao Technology Co., Ltd. (NT$2.87 billion). The company faces a notable financial adjustment and write-off of NT$6.45 billion, impacting overall financial results.

Forcecon Technology, a nimble player in the tech space, has shown impressive earnings growth of 39.8% over the past year, outpacing the industry average of 9.9%. This growth is backed by high-quality earnings and a solid financial position with more cash than its total debt. Over five years, its debt-to-equity ratio improved from 50% to 22.6%, indicating prudent financial management. Despite shareholder dilution in the past year, Forcecon remains attractive as it trades at nearly 40% below estimated fair value. With positive free cash flow and no concerns over interest coverage or cash runway, it seems poised for continued performance improvement.

- Click here to discover the nuances of Forcecon Technology with our detailed analytical health report.

Evaluate Forcecon Technology's historical performance by accessing our past performance report.

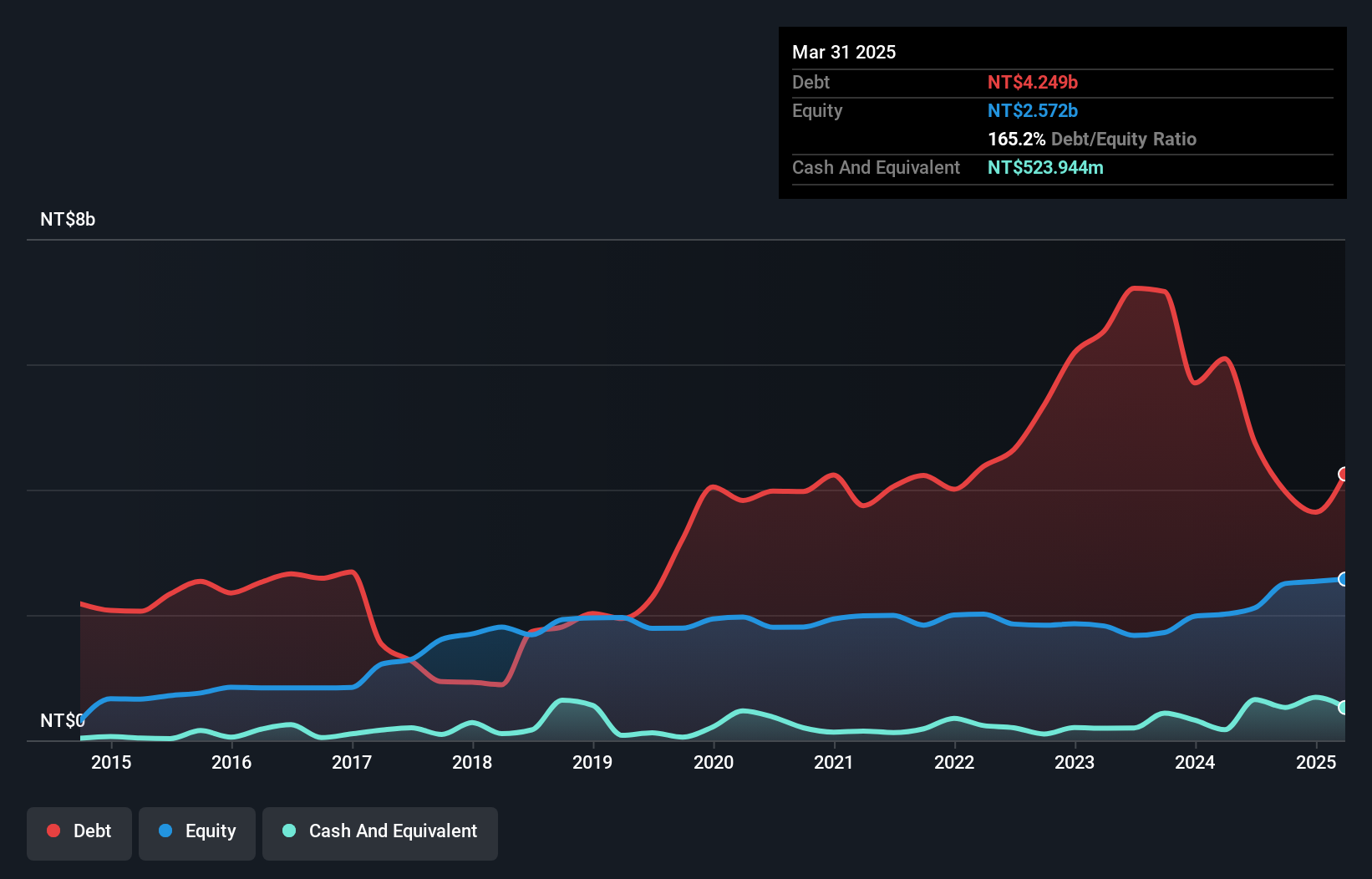

Fu Yu Property (TPEX:4907)

Simply Wall St Value Rating: ★★★★★☆

Overview: Fu Yu Property Co., Ltd. focuses on the development, rental, and sale of residential buildings in Taiwan with a market cap of NT$8.27 billion.

Operations: Fu Yu Property generates revenue primarily from the development, rental, and sale of residential buildings in Taiwan. The company has a market cap of NT$8.27 billion.

Fu Yu Property, a smaller player in the real estate sector, has recently showcased impressive growth. The company's earnings surged by 3,539%, significantly outpacing the industry's 52% increase over the past year. Despite a high net debt to equity ratio of 46.8%, Fu Yu's interest payments are well-covered at 2,548 times by EBIT. Recent expansions include acquiring land in Taichung City and Hsinchu County for residential projects totaling TWD 602 million and TWD 608 million respectively. With sales reaching TWD 1.7 billion this quarter compared to TWD 882 million last year, Fu Yu appears poised for continued momentum.

- Dive into the specifics of Fu Yu Property here with our thorough health report.

Examine Fu Yu Property's past performance report to understand how it has performed in the past.

Turning Ideas Into Actions

- Delve into our full catalog of 4627 Undiscovered Gems With Strong Fundamentals here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:3483

Forcecon Technology

Engages in the research, development, production, and sale of thermal management products in Taiwan and internationally.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor