Advertisement

Analysts Just Shipped A Captivating Upgrade To Their SCI Pharmtech, Inc. (TPE:4119) Estimates

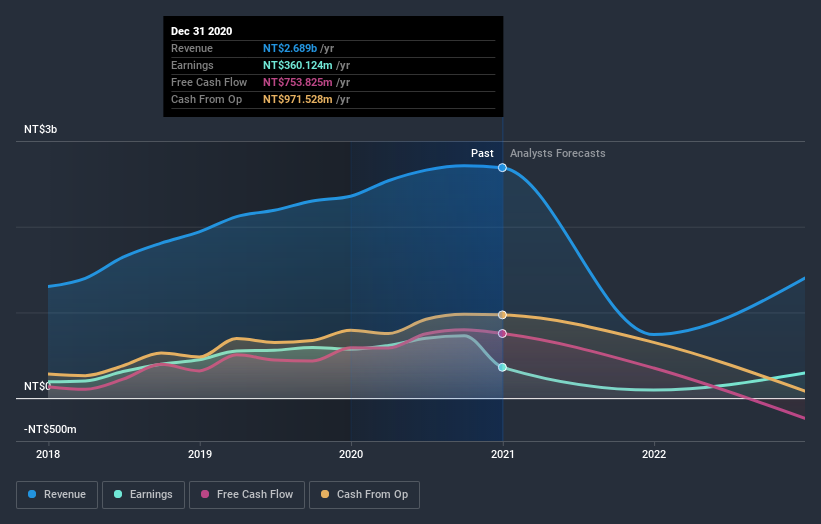

SCI Pharmtech, Inc. (TPE:4119) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

After the upgrade, the consensus from SCI Pharmtech's three analysts is for revenues of NT$742m in 2021, which would reflect a concerning 72% decline in sales compared to the last year of performance. Statutory earnings per share are supposed to crater 74% to NT$1.18 in the same period. Previously, the analysts had been modelling revenues of NT$609m and earnings per share (EPS) of NT$0.56 in 2021. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for SCI Pharmtech

With these upgrades, we're not surprised to see that the analysts have lifted their price target 11% to NT$89.33 per share. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on SCI Pharmtech, with the most bullish analyst valuing it at NT$95.00 and the most bearish at NT$82.00 per share. This is a very narrow spread of estimates, implying either that SCI Pharmtech is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 72% annualised revenue decline to the end of 2021. That is a notable change from historical growth of 10% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 17% annually for the foreseeable future. It's pretty clear that SCI Pharmtech's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at SCI Pharmtech.

Analysts are clearly in love with SCI Pharmtech at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as its declining profit margins. For more information, you can click through to our platform to learn more about this and the 3 other flags we've identified .

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading SCI Pharmtech or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:4119

SCI Pharmtech

Together with its subsidiary, engages in the research and development, manufacture, and sale of active pharmaceutical ingredients, intermediates, and specialty chemicals in Italy, the United States, Japan, Germany, Taiwan, Switzerland, China, and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor