Advertisement

Did Ho Tung Chemical's (TPE:1714) Share Price Deserve to Gain 37%?

When you buy and hold a stock for the long term, you definitely want it to provide a positive return. But more than that, you probably want to see it rise more than the market average. Unfortunately for shareholders, while the Ho Tung Chemical Corp. (TPE:1714) share price is up 37% in the last five years, that's less than the market return. Looking at the last year alone, the stock is up 19%.

See our latest analysis for Ho Tung Chemical

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

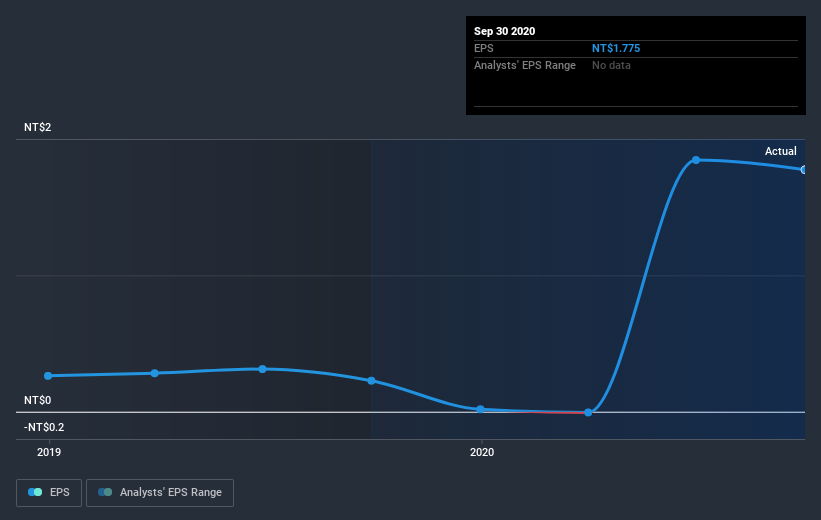

Over half a decade, Ho Tung Chemical managed to grow its earnings per share at 82% a year. The EPS growth is more impressive than the yearly share price gain of 6% over the same period. So one could conclude that the broader market has become more cautious towards the stock. The reasonably low P/E ratio of 5.16 also suggests market apprehension.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

This free interactive report on Ho Tung Chemical's earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

What about the Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Ho Tung Chemical's total shareholder return (TSR) and its share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Dividends have been really beneficial for Ho Tung Chemical shareholders, and that cash payout contributed to why its TSR of 46%, over the last 5 years, is better than the share price return.

A Different Perspective

Ho Tung Chemical provided a TSR of 19% over the last twelve months. But that was short of the market average. The silver lining is that the gain was actually better than the average annual return of 8% per year over five year. This suggests the company might be improving over time. Is Ho Tung Chemical cheap compared to other companies? These 3 valuation measures might help you decide.

But note: Ho Tung Chemical may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on TW exchanges.

If you’re looking to trade Ho Tung Chemical, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Ho Tung Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1714

Ho Tung Chemical

Develops, manufactures, processes, and sells various chemical products in Taiwan, China, Southeast Asia, and internationally.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|25.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|6.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|25.9% undervalued

KA

Community Contributor