Advertisement

- Taiwan

- /

- Hospitality

- /

- TPEX:2755

Should You Be Impressed By YoungQin International's (GTSM:2755) Returns on Capital?

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. With that in mind, the ROCE of YoungQin International (GTSM:2755) looks decent, right now, so lets see what the trend of returns can tell us.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for YoungQin International:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.11 = NT$84m ÷ (NT$1.1b - NT$323m) (Based on the trailing twelve months to September 2020).

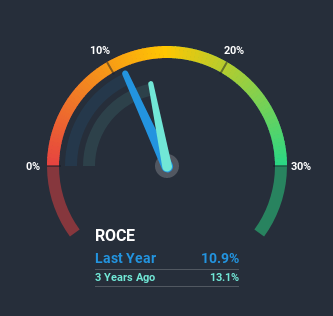

Thus, YoungQin International has an ROCE of 11%. In absolute terms, that's a satisfactory return, but compared to the Hospitality industry average of 5.6% it's much better.

Check out our latest analysis for YoungQin International

Historical performance is a great place to start when researching a stock so above you can see the gauge for YoungQin International's ROCE against it's prior returns. If you'd like to look at how YoungQin International has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

While the returns on capital are good, they haven't moved much. The company has employed 58% more capital in the last three years, and the returns on that capital have remained stable at 11%. 11% is a pretty standard return, and it provides some comfort knowing that YoungQin International has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

One more thing to note, even though ROCE has remained relatively flat over the last three years, the reduction in current liabilities to 30% of total assets, is good to see from a business owner's perspective. Effectively suppliers now fund less of the business, which can lower some elements of risk.The Key Takeaway

The main thing to remember is that YoungQin International has proven its ability to continually reinvest at respectable rates of return. And the stock has followed suit returning a meaningful 34% to shareholders over the last year. So while investors seem to be recognizing these promising trends, we still believe the stock deserves further research.

Like most companies, YoungQin International does come with some risks, and we've found 2 warning signs that you should be aware of.

While YoungQin International may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you decide to trade YoungQin International, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:2755

YoungQin International

Engages in the restaurant and bakery business in Taiwan and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor