Advertisement

As global markets navigate a busy earnings season and mixed economic signals, small-cap stocks have shown resilience amid broader market volatility. With major indices like the S&P MidCap 400 and Russell 2000 demonstrating relative strength compared to their large-cap counterparts, investors are increasingly looking towards lesser-known opportunities that may offer promising potential. In this environment, identifying a good stock involves examining companies with strong fundamentals that can withstand economic uncertainties and capitalize on emerging trends.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Marítima de Inversiones | NA | 86.64% | 24.51% | ★★★★★★ |

| Wisynco Group | 12.60% | 14.26% | 17.20% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Cardig Aero Services | NA | 6.60% | 69.79% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Compañía Electro Metalúrgica | 72.83% | 12.17% | 19.18% | ★★★★☆☆ |

| BOSQAR d.d | 94.35% | 39.99% | 23.94% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

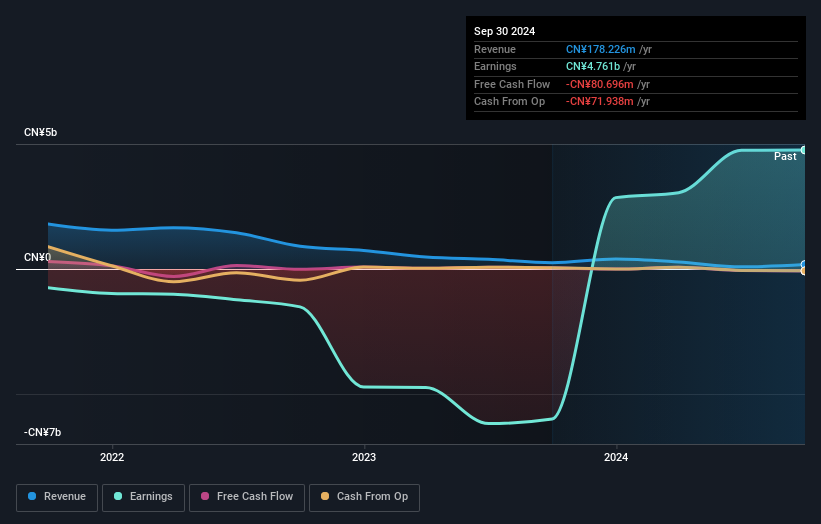

Wuhan Ddmc Culture&SportsLtd (SHSE:600136)

Simply Wall St Value Rating: ★★★★★☆

Overview: Wuhan Ddmc Culture&Sports Co., Ltd. is engaged in the film, television, and sports industries both within China and internationally, with a market capitalization of CN¥3.61 billion.

Operations: The company generates revenue through its involvement in the film, television, and sports sectors. Its financial performance is marked by a notable net profit margin trend.

Wuhan Ddmc Culture&Sports Ltd., a relatively smaller entity, has shown notable financial shifts recently. The company reported a net loss of CN¥28.51 million for the nine months ending September 2024, improving from CN¥1.94 billion the previous year, indicating potential stabilization despite sales dropping to CN¥154.65 million from CN¥376.29 million year-on-year. Its debt-to-equity ratio impressively decreased from 79.8% to 3.3% over five years, showcasing effective debt management strategies and more cash than total debt further bolsters its financial position despite challenges like substantial shareholder dilution recently impacting equity value.

- Take a closer look at Wuhan Ddmc Culture&SportsLtd's potential here in our health report.

Understand Wuhan Ddmc Culture&SportsLtd's track record by examining our Past report.

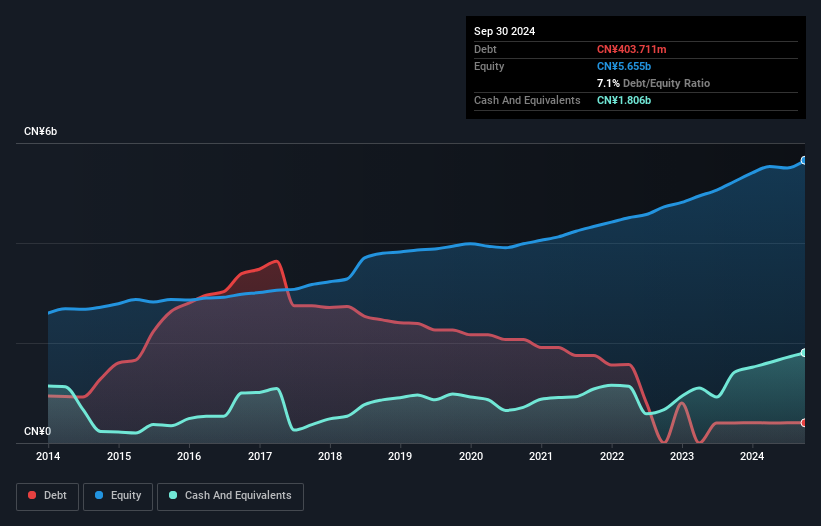

Jilin Expressway (SHSE:601518)

Simply Wall St Value Rating: ★★★★★★

Overview: Jilin Expressway Co., Ltd. operates in the investment, development, construction, operation, management, and maintenance of toll roads in Jilin Province with a market cap of CN¥5.41 billion.

Operations: The primary revenue streams for Jilin Expressway Co., Ltd. are derived from its toll road operations in Jilin Province. The company focuses on managing costs effectively to optimize profitability, with a noteworthy trend in its net profit margin over recent periods.

Jilin Expressway, a smaller player in the infrastructure sector, shows promise with earnings growth of 16.5% over the past year, outpacing the industry's 3.1%. The company is trading at a notable 30.9% below its estimated fair value, suggesting potential undervaluation. Over five years, Jilin's debt to equity ratio impressively shrank from 57.5% to just 0.4%, reflecting strong financial management and reduced leverage risk. Recent reports indicate stable net income at CNY 389 million for nine months ending September 2024, consistent with last year's figures despite slightly lower sales of CNY 869 million compared to CNY 938 million previously.

- Click to explore a detailed breakdown of our findings in Jilin Expressway's health report.

Explore historical data to track Jilin Expressway's performance over time in our Past section.

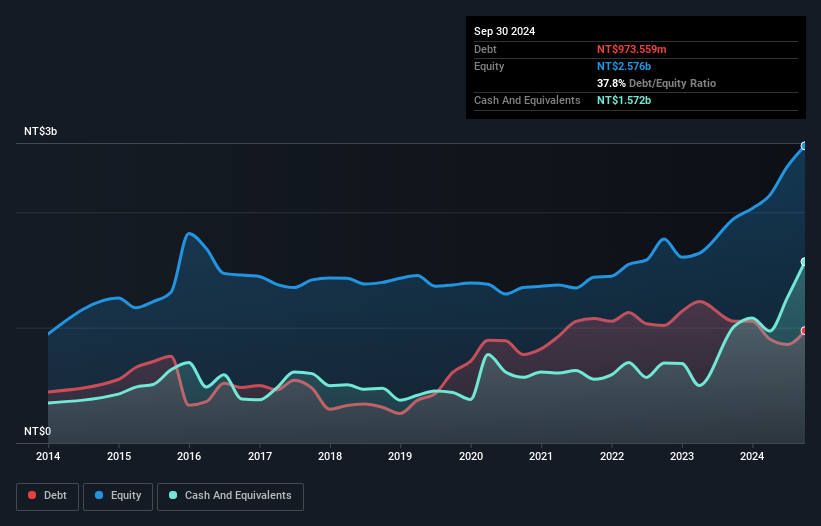

Bonny Worldwide (TWSE:8467)

Simply Wall St Value Rating: ★★★★★☆

Overview: Bonny Worldwide Limited, along with its subsidiaries, specializes in the manufacture and sale of OEM and ODM carbon fiber rackets and related sporting goods, with a market cap of NT$14.45 billion.

Operations: The company's primary revenue stream is from the research and development, design, manufacturing, and sales of carbon fiber products, generating NT$2.30 billion.

Bonny Worldwide, a compact player in the market, has shown impressive financial strides with earnings growth of 46.2% over the past year, outpacing the Leisure industry's -38.1%. The company is trading at 15.2% below its estimated fair value and boasts high-quality earnings while maintaining more cash than total debt despite a rise in its debt to equity ratio from 31.4% to 35.7%. Recent inclusion in the S&P Global BMI Index underscores its growing prominence, while Q3 results highlight significant sales and net income increases compared to last year, reflecting robust operational performance amidst volatile share price movements.

- Dive into the specifics of Bonny Worldwide here with our thorough health report.

Examine Bonny Worldwide's past performance report to understand how it has performed in the past.

Next Steps

- Dive into all 4709 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bonny Worldwide might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:8467

Bonny Worldwide

Engages in the manufacture and sale of OEM and ODM carbon fiber rackets and related sporting goods.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor