Advertisement

Uncovering January 2025's Undiscovered Gems with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a mixed start to the year, with major indices like the S&P 500 and Nasdaq Composite showing resilience despite economic headwinds such as a declining Chicago PMI and revised GDP forecasts, investors are keenly observing small-cap stocks for potential opportunities. In this environment, identifying stocks with strong fundamentals and growth potential can be particularly rewarding, especially as these companies may benefit from broader market trends or specific sector tailwinds.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| SHL Consolidated Bhd | NA | 16.14% | 19.01% | ★★★★★★ |

| Bahnhof | NA | 8.70% | 14.93% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| National General Insurance (P.J.S.C.) | NA | 11.69% | 30.36% | ★★★★★☆ |

| Onde | 21.84% | 8.04% | 2.79% | ★★★★★☆ |

| Infinity Capital Investments | NA | 9.92% | 22.16% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

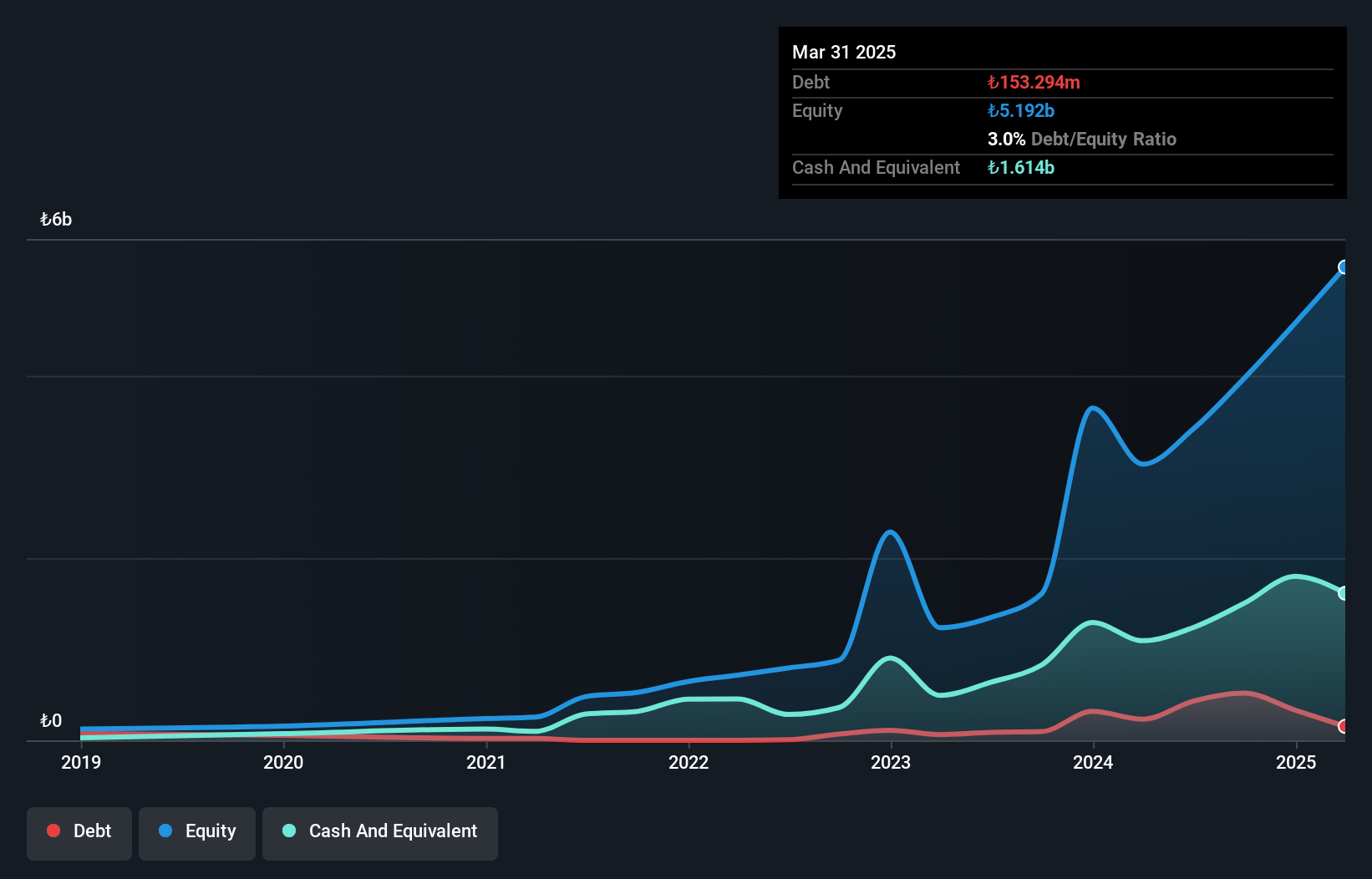

Kalekim Kimyevi Maddeler Sanayi Ve Ticaret Anonim Sirketi (IBSE:KLKIM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kalekim Kimyevi Maddeler Sanayi Ve Ticaret Anonim Sirketi operates in the building materials and chemicals sector both within Turkey and internationally, with a market capitalization of TRY15.24 billion.

Operations: Kalekim generates revenue primarily from ceramic applications, contributing TRY3.17 billion, and concrete, cement chemicals and raw materials at TRY1.26 billion. The paint-plaster segment adds TRY402.96 million, while waterproofing contributes TRY316.51 million to the overall revenue mix.

Kalekim's recent performance highlights its potential as a promising player in the chemicals sector. With earnings soaring by 166.9% over the past year, it outpaced the industry average of -10.5%. The company reported a net income of TRY 240.98 million for Q3 2024, compared to a net loss of TRY 53.57 million last year, showcasing significant improvement. Its price-to-earnings ratio stands at 18.4x, which is competitive within its industry context. Additionally, Kalekim has successfully reduced its debt-to-equity ratio from 45.6% to just 13% over five years, indicating prudent financial management and positioning it well for future growth prospects with forecasted annual earnings growth of around 22%.

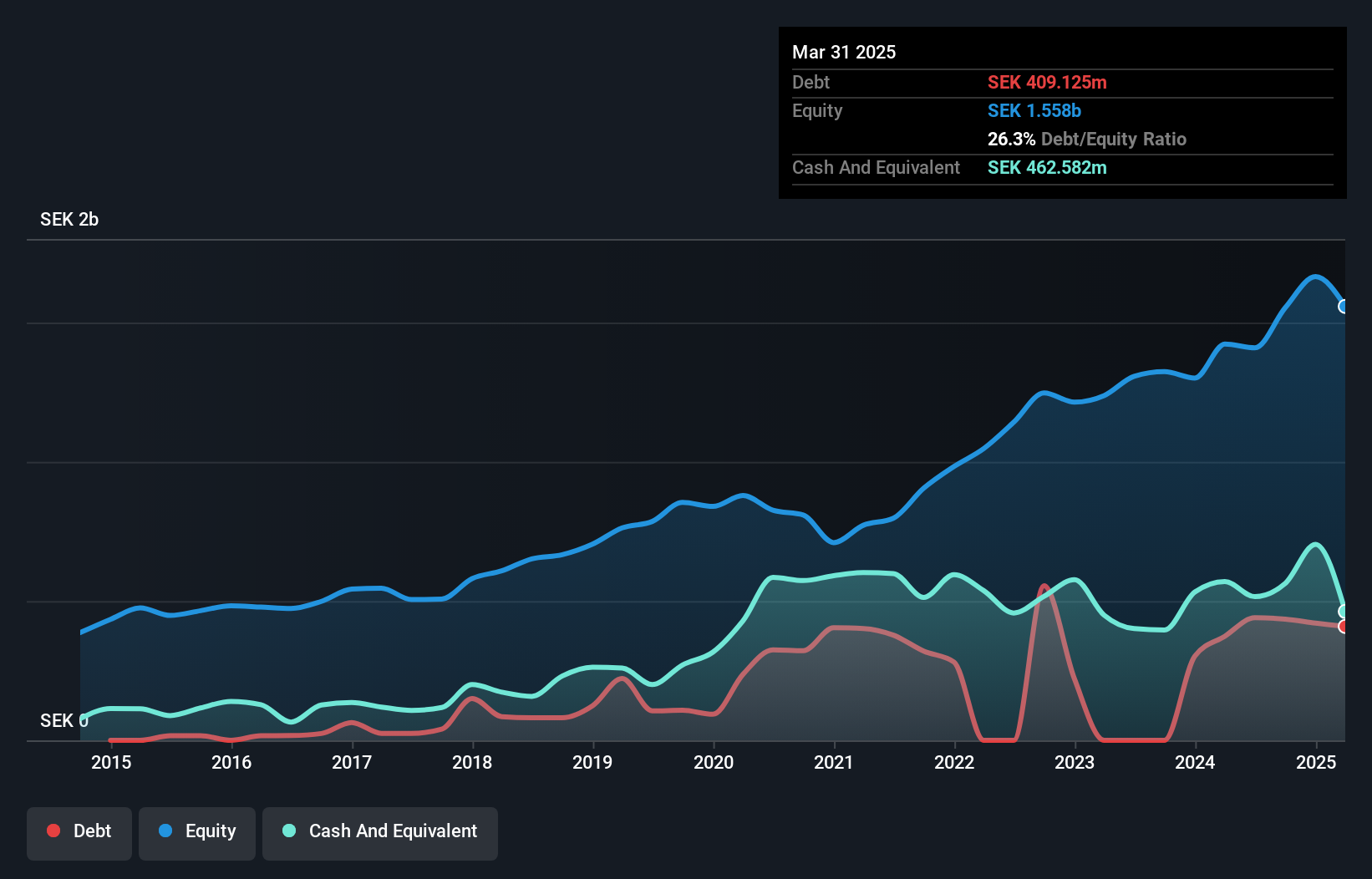

BTS Group (OM:BTS B)

Simply Wall St Value Rating: ★★★★★☆

Overview: BTS Group AB (publ) is a professional services firm with a market capitalization of approximately SEK5.35 billion.

Operations: BTS Group AB generates revenue primarily from its operations in North America, Europe, and other markets, with BTS North America contributing SEK1.53 billion and BTS Europe SEK558.39 million. The company also earns from Advantage Performance Group (APG) at SEK157.62 million. Segment adjustments account for a reduction of SEK298.25 million in the overall revenue calculation.

BTS Group, a nimble player in the professional services field, has been on a financial rollercoaster. Over the past year, earnings skyrocketed by 138.8%, significantly outpacing the industry average of 26.9%. Despite this growth, a substantial one-off gain of SEK222.6M skewed recent results. The company is trading at 20.3% below its estimated fair value and boasts robust interest coverage with EBIT covering interest payments 9.6 times over. While cash exceeds total debt levels, their debt-to-equity ratio climbed from 12.6% to 28% over five years, indicating increased leverage amidst plans for larger acquisitions ahead.

- Get an in-depth perspective on BTS Group's performance by reading our health report here.

Understand BTS Group's track record by examining our Past report.

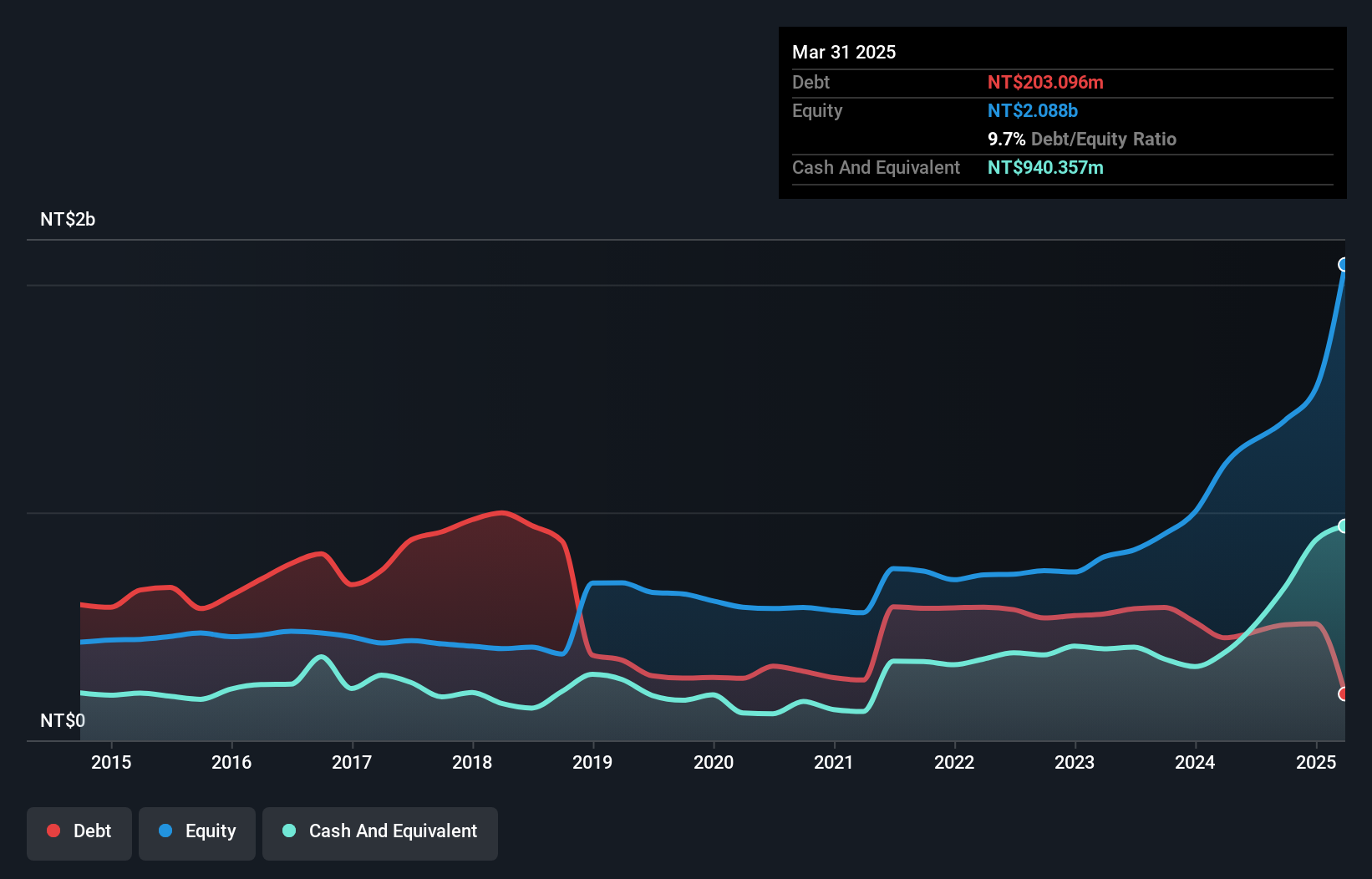

Wiselink (TPEX:8932)

Simply Wall St Value Rating: ★★★★★★

Overview: Wiselink Co., Ltd. is a global manufacturer and marketer of zippers with a market capitalization of NT$15.34 billion.

Operations: Wiselink generates revenue primarily from the Taiwan Area (NT$397.80 million), Mainland China (NT$475.96 million), and Other Asia Pacific Regions (NT$595.45 million). The company faces a cancellation of intersegment transactions amounting to NT$175.17 million, impacting its overall revenue figures.

Wiselink's recent performance highlights its growth potential, with earnings surging 630.2% over the past year, outpacing the Luxury industry's 13.9%. The company is trading at a significant discount of 40.8% below estimated fair value, suggesting potential undervaluation. Wiselink's debt-to-equity ratio improved from 42.5% to 36.1% over five years, indicating better financial management and more cash than total debt supports this stability. Recent developments include a new Sustainable Development Committee and a follow-on equity offering of four million shares, which may impact shareholder value in the short term but could support long-term initiatives.

Seize The Opportunity

- Gain an insight into the universe of 4672 Undiscovered Gems With Strong Fundamentals by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kalekim Kimyevi Maddeler Sanayi Ve Ticaret Anonim Sirketi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:KLKIM

Kalekim Kimyevi Maddeler Sanayi Ve Ticaret Anonim Sirketi

Operates in the construction chemicals sector in Turkey and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor