Advertisement

Is Weakness In KMC (Kuei Meng) International Inc. (GTSM:5306) Stock A Sign That The Market Could be Wrong Given Its Strong Financial Prospects?

It is hard to get excited after looking at KMC (Kuei Meng) International's (GTSM:5306) recent performance, when its stock has declined 8.9% over the past month. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. In this article, we decided to focus on KMC (Kuei Meng) International's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for KMC (Kuei Meng) International

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for KMC (Kuei Meng) International is:

23% = NT$1.3b ÷ NT$5.7b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. So, this means that for every NT$1 of its shareholder's investments, the company generates a profit of NT$0.23.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

KMC (Kuei Meng) International's Earnings Growth And 23% ROE

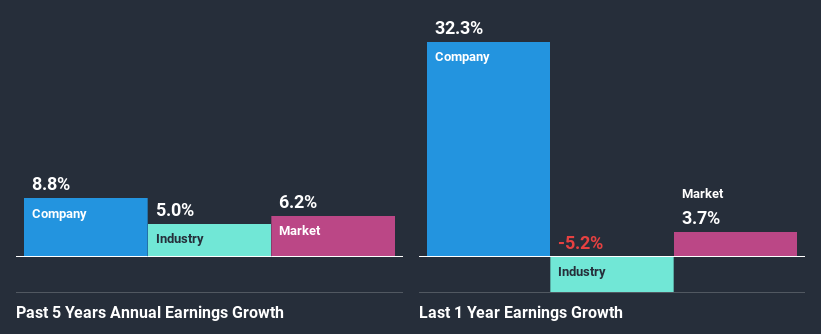

Firstly, we acknowledge that KMC (Kuei Meng) International has a significantly high ROE. Second, a comparison with the average ROE reported by the industry of 15% also doesn't go unnoticed by us. This probably laid the groundwork for KMC (Kuei Meng) International's moderate 8.8% net income growth seen over the past five years.

We then compared KMC (Kuei Meng) International's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 5.0% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is 5306 fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is KMC (Kuei Meng) International Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 55% (or a retention ratio of 45%) for KMC (Kuei Meng) International suggests that the company's growth wasn't really hampered despite it returning most of its income to its shareholders.

Additionally, KMC (Kuei Meng) International has paid dividends over a period of eight years which means that the company is pretty serious about sharing its profits with shareholders. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 59%. As a result, KMC (Kuei Meng) International's ROE is not expected to change by much either, which we inferred from the analyst estimate of 21% for future ROE.

Summary

In total, we are pretty happy with KMC (Kuei Meng) International's performance. Especially the high ROE, Which has contributed to the impressive growth seen in earnings. Despite the company reinvesting only a small portion of its profits, it still has managed to grow its earnings so that is appreciable. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

When trading KMC (Kuei Meng) International or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KMC (Kuei Meng) International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:5306

KMC (Kuei Meng) International

Manufactures and sells various types of chains, motorcycle components, and vehicle components in Asia, Europe, and the United States.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor