Advertisement

- Taiwan

- /

- Electrical

- /

- TWSE:1609

These 4 Measures Indicate That Ta Ya Electric Wire & Cable (TWSE:1609) Is Using Debt Extensively

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Ta Ya Electric Wire & Cable Co., Ltd. (TWSE:1609) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Ta Ya Electric Wire & Cable

What Is Ta Ya Electric Wire & Cable's Debt?

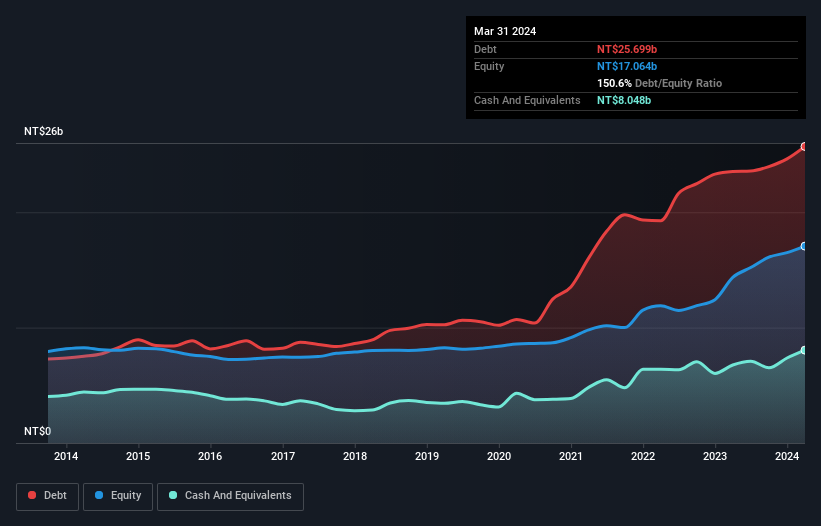

As you can see below, at the end of March 2024, Ta Ya Electric Wire & Cable had NT$25.7b of debt, up from NT$23.5b a year ago. Click the image for more detail. However, it also had NT$8.05b in cash, and so its net debt is NT$17.7b.

How Strong Is Ta Ya Electric Wire & Cable's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ta Ya Electric Wire & Cable had liabilities of NT$15.4b due within 12 months and liabilities of NT$15.6b due beyond that. Offsetting these obligations, it had cash of NT$8.05b as well as receivables valued at NT$5.34b due within 12 months. So it has liabilities totalling NT$17.7b more than its cash and near-term receivables, combined.

Ta Ya Electric Wire & Cable has a market capitalization of NT$41.8b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a net debt to EBITDA ratio of 6.8, it's fair to say Ta Ya Electric Wire & Cable does have a significant amount of debt. But the good news is that it boasts fairly comforting interest cover of 3.2 times, suggesting it can responsibly service its obligations. The silver lining is that Ta Ya Electric Wire & Cable grew its EBIT by 120% last year, which nourishing like the idealism of youth. If that earnings trend continues it will make its debt load much more manageable in the future. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ta Ya Electric Wire & Cable can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Ta Ya Electric Wire & Cable burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Ta Ya Electric Wire & Cable's conversion of EBIT to free cash flow and net debt to EBITDA definitely weigh on it, in our esteem. But the good news is it seems to be able to grow its EBIT with ease. When we consider all the factors discussed, it seems to us that Ta Ya Electric Wire & Cable is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Ta Ya Electric Wire & Cable has 6 warning signs (and 1 which is potentially serious) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Ta Ya Electric Wire & Cable might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1609

Ta Ya Electric Wire & Cable

Engages in the manufacture and sale of electric wires and cables in Taiwan and rest of Asia.

Mediocre balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor