Advertisement

- Taiwan

- /

- Electrical

- /

- TWSE:1513

Chung-Hsin Electric and Machinery Manufacturing Corp. (TWSE:1513) Stocks Shoot Up 29% But Its P/E Still Looks Reasonable

Chung-Hsin Electric and Machinery Manufacturing Corp. (TWSE:1513) shareholders have had their patience rewarded with a 29% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 61% in the last year.

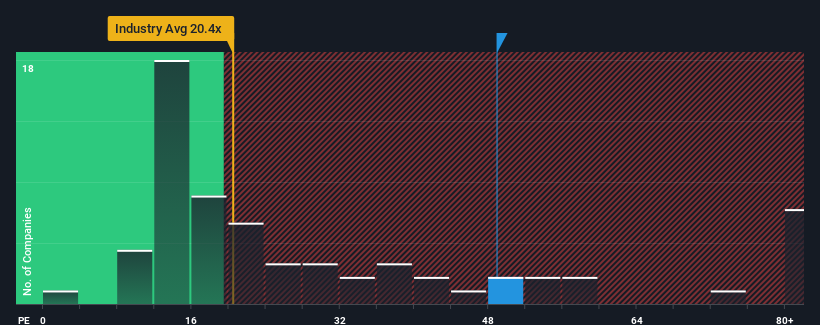

After such a large jump in price, Chung-Hsin Electric and Machinery Manufacturing may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 48.9x, since almost half of all companies in Taiwan have P/E ratios under 21x and even P/E's lower than 15x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings that are retreating more than the market's of late, Chung-Hsin Electric and Machinery Manufacturing has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Chung-Hsin Electric and Machinery Manufacturing

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Chung-Hsin Electric and Machinery Manufacturing's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 34%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 55% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 125% over the next year. That's shaping up to be materially higher than the 22% growth forecast for the broader market.

In light of this, it's understandable that Chung-Hsin Electric and Machinery Manufacturing's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Chung-Hsin Electric and Machinery Manufacturing's P/E

Chung-Hsin Electric and Machinery Manufacturing's P/E is flying high just like its stock has during the last month. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Chung-Hsin Electric and Machinery Manufacturing's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 4 warning signs for Chung-Hsin Electric and Machinery Manufacturing that you need to take into consideration.

Of course, you might also be able to find a better stock than Chung-Hsin Electric and Machinery Manufacturing. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1513

Chung-Hsin Electric and Machinery Manufacturing

Chung-Hsin Electric and Machinery Manufacturing Corp.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor