Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that NAK Sealing Technologies Corporation (TPE:9942) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for NAK Sealing Technologies

What Is NAK Sealing Technologies's Net Debt?

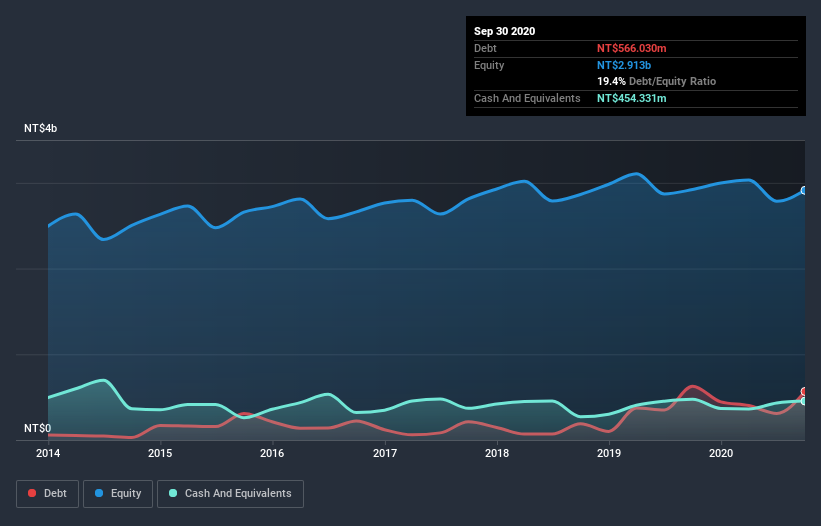

The image below, which you can click on for greater detail, shows that NAK Sealing Technologies had debt of NT$566.0m at the end of September 2020, a reduction from NT$627.4m over a year. On the flip side, it has NT$454.3m in cash leading to net debt of about NT$111.7m.

How Healthy Is NAK Sealing Technologies's Balance Sheet?

The latest balance sheet data shows that NAK Sealing Technologies had liabilities of NT$709.3m due within a year, and liabilities of NT$651.7m falling due after that. Offsetting this, it had NT$454.3m in cash and NT$940.2m in receivables that were due within 12 months. So it can boast NT$33.5m more liquid assets than total liabilities.

This state of affairs indicates that NAK Sealing Technologies's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the NT$5.60b company is struggling for cash, we still think it's worth monitoring its balance sheet.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

NAK Sealing Technologies has net debt of just 0.19 times EBITDA, suggesting it could ramp leverage without breaking a sweat. But the really cool thing is that it actually managed to receive more interest than it paid, over the last year. So it's fair to say it can handle debt like a hotshot teppanyaki chef handles cooking. On the other hand, NAK Sealing Technologies's EBIT dived 19%, over the last year. If that rate of decline in earnings continues, the company could find itself in a tight spot. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since NAK Sealing Technologies will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, NAK Sealing Technologies produced sturdy free cash flow equating to 60% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Happily, NAK Sealing Technologies's impressive interest cover implies it has the upper hand on its debt. But we must concede we find its EBIT growth rate has the opposite effect. Looking at all the aforementioned factors together, it strikes us that NAK Sealing Technologies can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with NAK Sealing Technologies (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade NAK Sealing Technologies, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NAK Sealing Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:9942

NAK Sealing Technologies

Manufactures and sells oil seals and technical sealing products in Taiwan, China, rest of Asia, Europe, America, and Africa.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives