Sanitar Co., Ltd.'s (TPE:1817) Stock Is Going Strong: Have Financials A Role To Play?

Sanitar (TPE:1817) has had a great run on the share market with its stock up by a significant 14% over the last three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Particularly, we will be paying attention to Sanitar's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Sanitar

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Sanitar is:

13% = NT$213m ÷ NT$1.7b (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.13 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Sanitar's Earnings Growth And 13% ROE

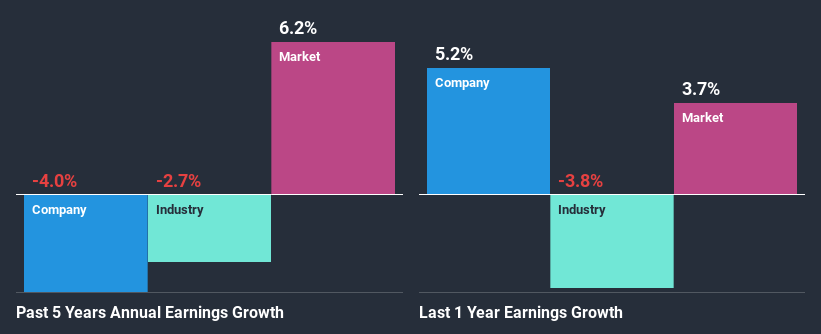

To start with, Sanitar's ROE looks acceptable. On comparing with the average industry ROE of 3.4% the company's ROE looks pretty remarkable. As you might expect, the 4.0% net income decline reported by Sanitar is a bit of a surprise. Therefore, there might be some other aspects that could explain this. Such as, the company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

As a next step, we compared Sanitar's performance with the industry and found thatSanitar's performance is depressing even when compared with the industry, which has shrunk its earnings at a rate of 2.7% in the same period, which is a slower than the company.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Sanitar is trading on a high P/E or a low P/E, relative to its industry.

Is Sanitar Using Its Retained Earnings Effectively?

With a high three-year median payout ratio of 66% (implying that 34% of the profits are retained), most of Sanitar's profits are being paid to shareholders, which explains the company's shrinking earnings. The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run. To know the 3 risks we have identified for Sanitar visit our risks dashboard for free.

In addition, Sanitar has been paying dividends over a period of nine years suggesting that keeping up dividend payments is preferred by the management even though earnings have been in decline.

Summary

On the whole, we do feel that Sanitar has some positive attributes. Although, we are disappointed to see a lack of growth in earnings even in spite of a high ROE. Bear in mind, the company reinvests a small portion of its profits, which means that investors aren't reaping the benefits of the high rate of return. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. You can do your own research on Sanitar and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

If you’re looking to trade Sanitar, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1817

Sanitar

Engages in the manufacture and distribution of sanitary porcelain products in Taiwan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Community Narratives