- Taiwan

- /

- Electrical

- /

- TWSE:1605

Here's Why We Don't Think Walsin Lihwa's (TPE:1605) Statutory Earnings Reflect Its Underlying Earnings Potential

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. Today we'll focus on whether this year's statutory profits are a good guide to understanding Walsin Lihwa (TPE:1605).

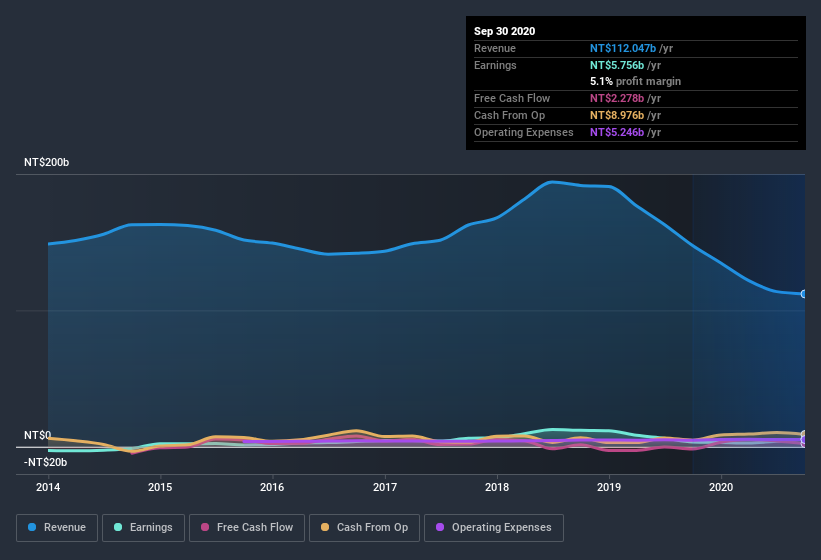

While Walsin Lihwa was able to generate revenue of NT$112.0b in the last twelve months, we think its profit result of NT$5.76b was more important. Below, you can see that both its revenue and its profit have fallen over the last three years.

View our latest analysis for Walsin Lihwa

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. This article will focus on the impact unusual items have had on Walsin Lihwa's statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Walsin Lihwa.

How Do Unusual Items Influence Profit?

To properly understand Walsin Lihwa's profit results, we need to consider the NT$2.0b gain attributed to unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On Walsin Lihwa's Profit Performance

Arguably, Walsin Lihwa's statutory earnings have been distorted by unusual items boosting profit. Because of this, we think that it may be that Walsin Lihwa's statutory profits are better than its underlying earnings power. The good news is that, its earnings per share increased by 67% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Case in point: We've spotted 3 warning signs for Walsin Lihwa you should be aware of.

Today we've zoomed in on a single data point to better understand the nature of Walsin Lihwa's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you’re looking to trade Walsin Lihwa, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Walsin Lihwa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:1605

Walsin Lihwa

Manufactures and sells wires and cables, and stainless steel products in Asia, the United States, Europe, and internationally.

Slight with imperfect balance sheet.

Similar Companies

Market Insights

Community Narratives