Advertisement

- Taiwan

- /

- Trade Distributors

- /

- TPEX:8415

Is The Market Rewarding Brighton-Best International (Taiwan) Inc. (GTSM:8415) With A Negative Sentiment As A Result Of Its Mixed Fundamentals?

With its stock down 8.0% over the past three months, it is easy to disregard Brighton-Best International (Taiwan) (GTSM:8415). It is possible that the markets have ignored the company's differing financials and decided to lean-in to the negative sentiment. Long-term fundamentals are usually what drive market outcomes, so it's worth paying close attention. Particularly, we will be paying attention to Brighton-Best International (Taiwan)'s ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Brighton-Best International (Taiwan)

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Brighton-Best International (Taiwan) is:

3.2% = NT$480m ÷ NT$15b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.03 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Brighton-Best International (Taiwan)'s Earnings Growth And 3.2% ROE

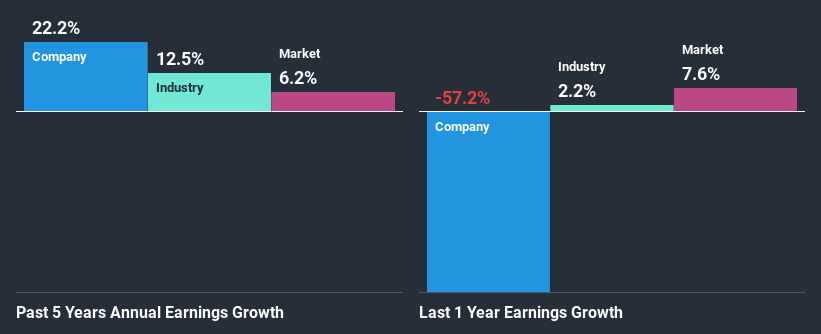

At first glance, Brighton-Best International (Taiwan)'s ROE doesn't look very promising. We then compared the company's ROE to the broader industry and were disappointed to see that the ROE is lower than the industry average of 9.9%. Despite this, surprisingly, Brighton-Best International (Taiwan) saw an exceptional 22% net income growth over the past five years. So, there might be other aspects that are positively influencing the company's earnings growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

We then compared Brighton-Best International (Taiwan)'s net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 12% in the same period.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Brighton-Best International (Taiwan) is trading on a high P/E or a low P/E, relative to its industry.

Is Brighton-Best International (Taiwan) Making Efficient Use Of Its Profits?

Brighton-Best International (Taiwan)'s very high three-year median payout ratio of 165% suggests that the company is paying more to its shareholders than what it is earning. Despite this, the company's earnings grew significantly as we saw above. With that said, it could be worth keeping an eye on the high payout ratio as that's a huge risk. To know the 3 risks we have identified for Brighton-Best International (Taiwan) visit our risks dashboard for free.

Moreover, Brighton-Best International (Taiwan) is determined to keep sharing its profits with shareholders which we infer from its long history of nine years of paying a dividend.

Summary

Overall, we have mixed feelings about Brighton-Best International (Taiwan). Although the company has shown a pretty impressive growth in earnings, yet the low ROE and the low rate of reinvestment makes us skeptical about the continuity of that growth, especially when or if the business comes to face any threats. Up till now, we've only made a short study of the company's growth data. To gain further insights into Brighton-Best International (Taiwan)'s past profit growth, check out this visualization of past earnings, revenue and cash flows.

When trading Brighton-Best International (Taiwan) or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Brighton-Best International (Taiwan) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:8415

Brighton-Best International (Taiwan)

Brighton-Best International (Taiwan) Inc.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor