Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Rodex Fasteners Corp. (GTSM:5015) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Rodex Fasteners

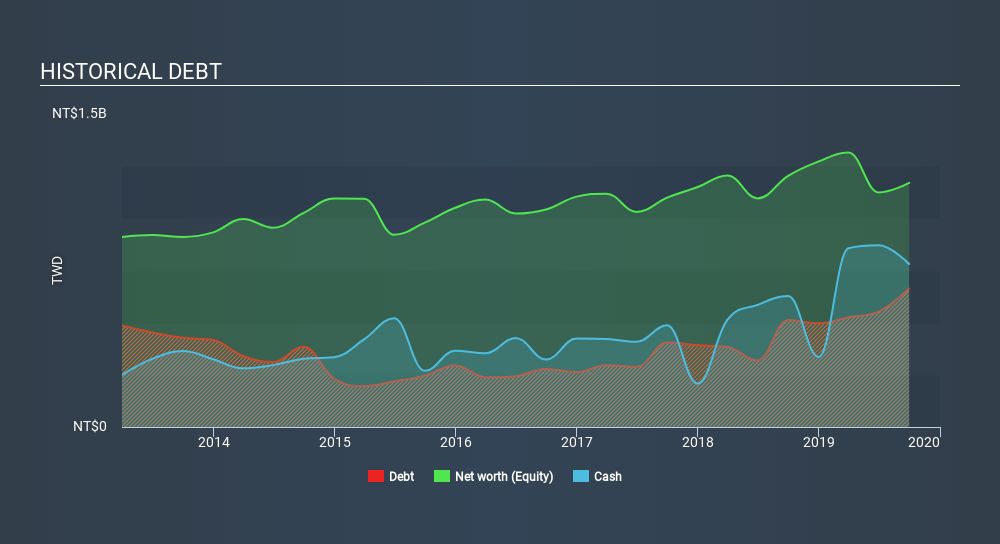

What Is Rodex Fasteners's Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2019 Rodex Fasteners had NT$663.7m of debt, an increase on NT$513.2m, over one year. However, its balance sheet shows it holds NT$780.8m in cash, so it actually has NT$117.1m net cash.

How Healthy Is Rodex Fasteners's Balance Sheet?

We can see from the most recent balance sheet that Rodex Fasteners had liabilities of NT$866.3m falling due within a year, and liabilities of NT$54.1m due beyond that. Offsetting these obligations, it had cash of NT$780.8m as well as receivables valued at NT$304.0m due within 12 months. So it actually has NT$164.4m more liquid assets than total liabilities.

This short term liquidity is a sign that Rodex Fasteners could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Rodex Fasteners boasts net cash, so it's fair to say it does not have a heavy debt load!

In fact Rodex Fasteners's saving grace is its low debt levels, because its EBIT has tanked 83% in the last twelve months. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Rodex Fasteners will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Rodex Fasteners may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Rodex Fasteners recorded free cash flow worth a fulsome 90% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Summing up

While it is always sensible to investigate a company's debt, in this case Rodex Fasteners has NT$117.1m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of NT$156m, being 90% of its EBIT. So we don't have any problem with Rodex Fasteners's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Consider risks, for instance. Every company has them, and we've spotted 3 warning signs for Rodex Fasteners you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TPEX:5015

Rodex Fasteners

Engages in the manufacture and sale of stainless wire and precision-made screws worldwide.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor