Advertisement

- Turkey

- /

- Wireless Telecom

- /

- IBSE:TCELL

3 Global Stocks Estimated To Be Trading Up To 46.5% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by mixed performance across major indices and ongoing economic uncertainties, investors are increasingly focused on identifying opportunities amid elevated valuations and cautious monetary policies. In this environment, finding stocks that are trading below their intrinsic value can present compelling investment prospects, as they may offer potential for growth when broader market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Unimot (WSE:UNT) | PLN128.00 | PLN255.57 | 49.9% |

| STEICO (XTRA:ST5) | €20.20 | €40.18 | 49.7% |

| Samyang Foods (KOSE:A003230) | ₩1382000.00 | ₩2750940.82 | 49.8% |

| Raksul (TSE:4384) | ¥1150.00 | ¥2271.14 | 49.4% |

| Nippon Thompson (TSE:6480) | ¥705.00 | ¥1407.82 | 49.9% |

| JINS HOLDINGS (TSE:3046) | ¥6210.00 | ¥12258.81 | 49.3% |

| Exel Composites Oyj (HLSE:EXL1V) | €0.392 | €0.78 | 49.9% |

| Corporativo Fragua. de (BMV:FRAGUA B) | MX$539.50 | MX$1067.18 | 49.4% |

| Bonesupport Holding (OM:BONEX) | SEK198.20 | SEK394.13 | 49.7% |

| Allcore (BIT:CORE) | €1.33 | €2.66 | 49.9% |

Here's a peek at a few of the choices from the screener.

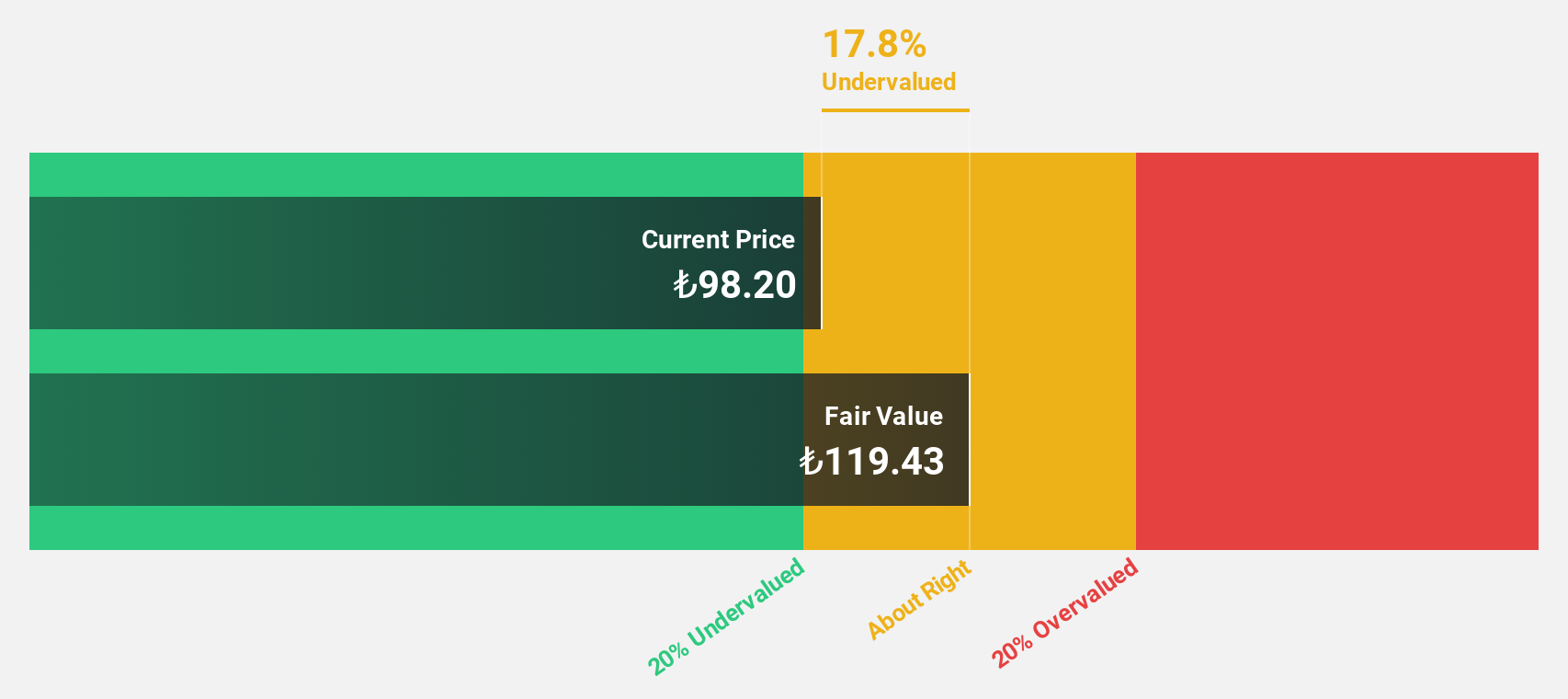

Turkcell Iletisim Hizmetleri (IBSE:TCELL)

Overview: Turkcell Iletisim Hizmetleri A.S., along with its subsidiaries, offers converged telecommunication and technology services across Turkey, Belarus, the Turkish Republic of Northern Cyprus, and the Netherlands, with a market cap of TRY210.46 billion.

Operations: The company's revenue segments include Turkcell Turkey, which generated TRY159.86 billion, and Techfin, contributing TRY10.54 billion.

Estimated Discount To Fair Value: 39.7%

Turkcell Iletisim Hizmetleri is trading significantly below its estimated fair value, presenting a potentially undervalued opportunity based on cash flows. The company forecasts robust earnings growth of 48.7% annually, outpacing the Turkish market. Despite lower profit margins compared to last year, strategic partnerships like the one with Google Cloud could enhance Turkcell's digital capabilities and revenue streams. However, an unstable dividend track record and low future return on equity remain concerns for investors.

- The analysis detailed in our Turkcell Iletisim Hizmetleri growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Turkcell Iletisim Hizmetleri.

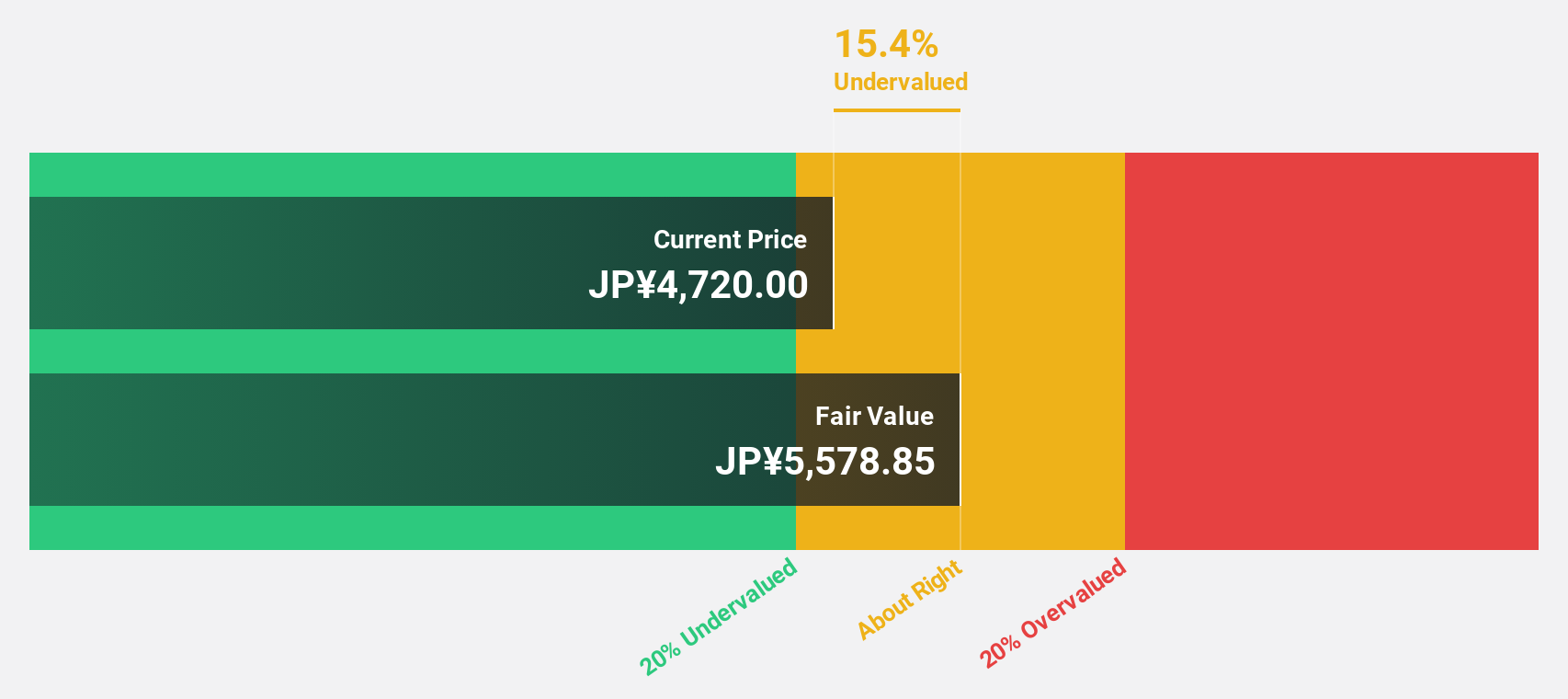

TORIDOLL Holdings (TSE:3397)

Overview: TORIDOLL Holdings Corporation operates and manages restaurants both in Japan and internationally, with a market cap of ¥389.01 billion.

Operations: TORIDOLL Holdings Corporation generates revenue from its restaurant operations across Japan and international markets.

Estimated Discount To Fair Value: 21.9%

TORIDOLL Holdings is trading at ¥4,538, which is 21.9% below its estimated fair value of ¥5,809.54, highlighting a potential undervaluation based on cash flows. The company anticipates significant earnings growth of 31.41% annually over the next three years and revenue growth of 6.9%, outpacing the JP market's average. However, a low forecasted return on equity and large one-off items affecting financial results may pose challenges for investors assessing long-term value.

- Our expertly prepared growth report on TORIDOLL Holdings implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of TORIDOLL Holdings with our detailed financial health report.

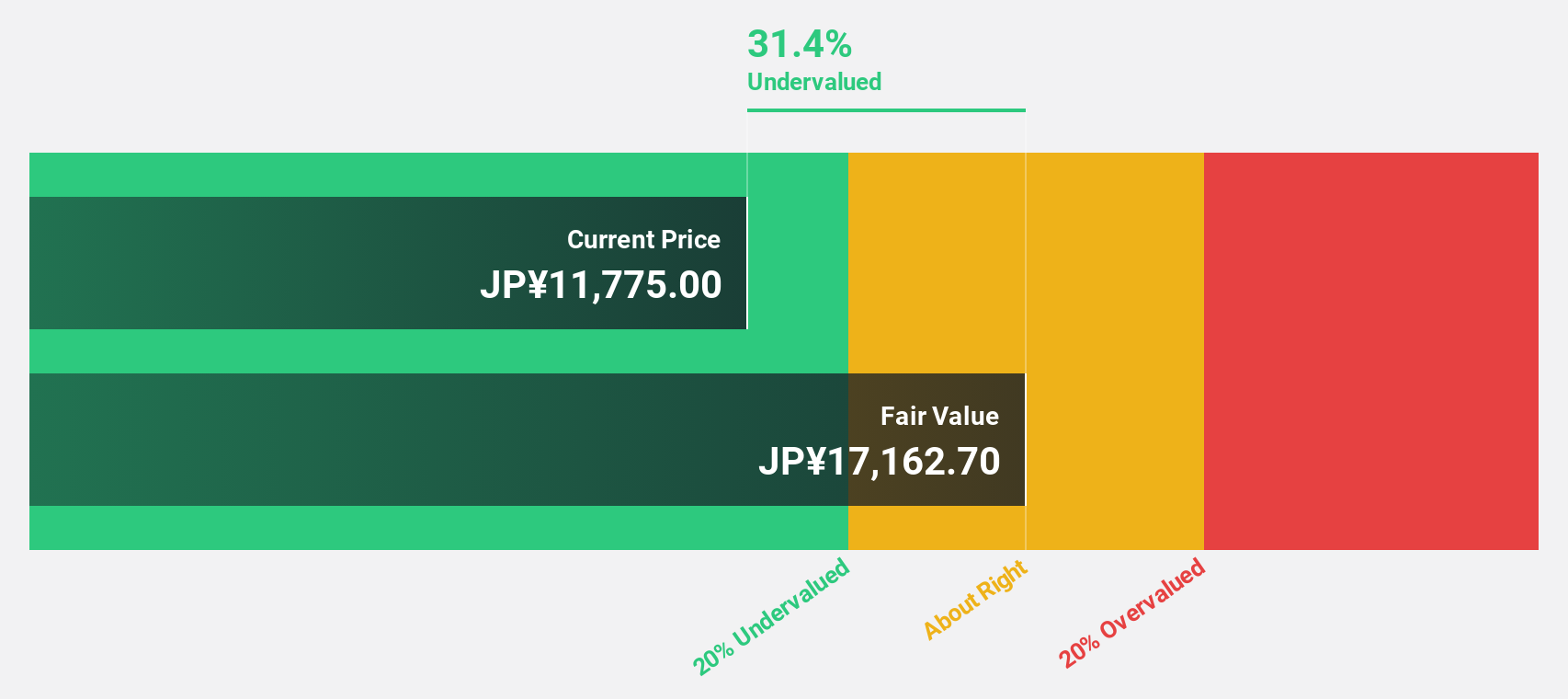

Visional (TSE:4194)

Overview: Visional, Inc., along with its subsidiaries, offers human resources platform solutions in Japan and has a market cap of ¥400.84 billion.

Operations: Visional, Inc. generates revenue through its human resources platform solutions in Japan.

Estimated Discount To Fair Value: 46.5%

Visional, Inc. is trading at ¥10,460, significantly below its estimated fair value of ¥19,544.39, suggesting it may be undervalued based on cash flows. The company forecasts earnings growth of 14% annually and revenue growth of 13.8%, both surpassing the JP market averages. Recent inclusion in the FTSE All-World Index could enhance visibility among investors. However, while analysts expect a price rise of 22.6%, potential investors should consider broader market conditions and company-specific risks.

- Our comprehensive growth report raises the possibility that Visional is poised for substantial financial growth.

- Take a closer look at Visional's balance sheet health here in our report.

Summing It All Up

- Click through to start exploring the rest of the 506 Undervalued Global Stocks Based On Cash Flows now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Turkcell Iletisim Hizmetleri might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:TCELL

Turkcell Iletisim Hizmetleri

Provides converged telecommunication and technology services in Turkey, Belarus, Turkish Republic of Northern Cyprus, and the Netherlands.

Undervalued with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor