Advertisement

As global markets navigate a complex landscape marked by cautious Federal Reserve commentary and economic uncertainty, smaller-cap indexes have been particularly impacted, reflecting investor concerns about the durability of recent market trends. Amidst this backdrop, identifying stocks with strong potential can be challenging yet rewarding; such opportunities often arise from companies that demonstrate resilience and adaptability in the face of broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Mendelson Infrastructures & Industries | 32.64% | 6.72% | 15.39% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Payton Industries | NA | 9.27% | 15.41% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Nikko | 33.49% | 5.29% | -7.39% | ★★★★★☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| Malam - Team | 102.85% | 10.82% | -10.47% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Inversiones Doalca SOCIMI | 16.56% | 6.15% | 10.19% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

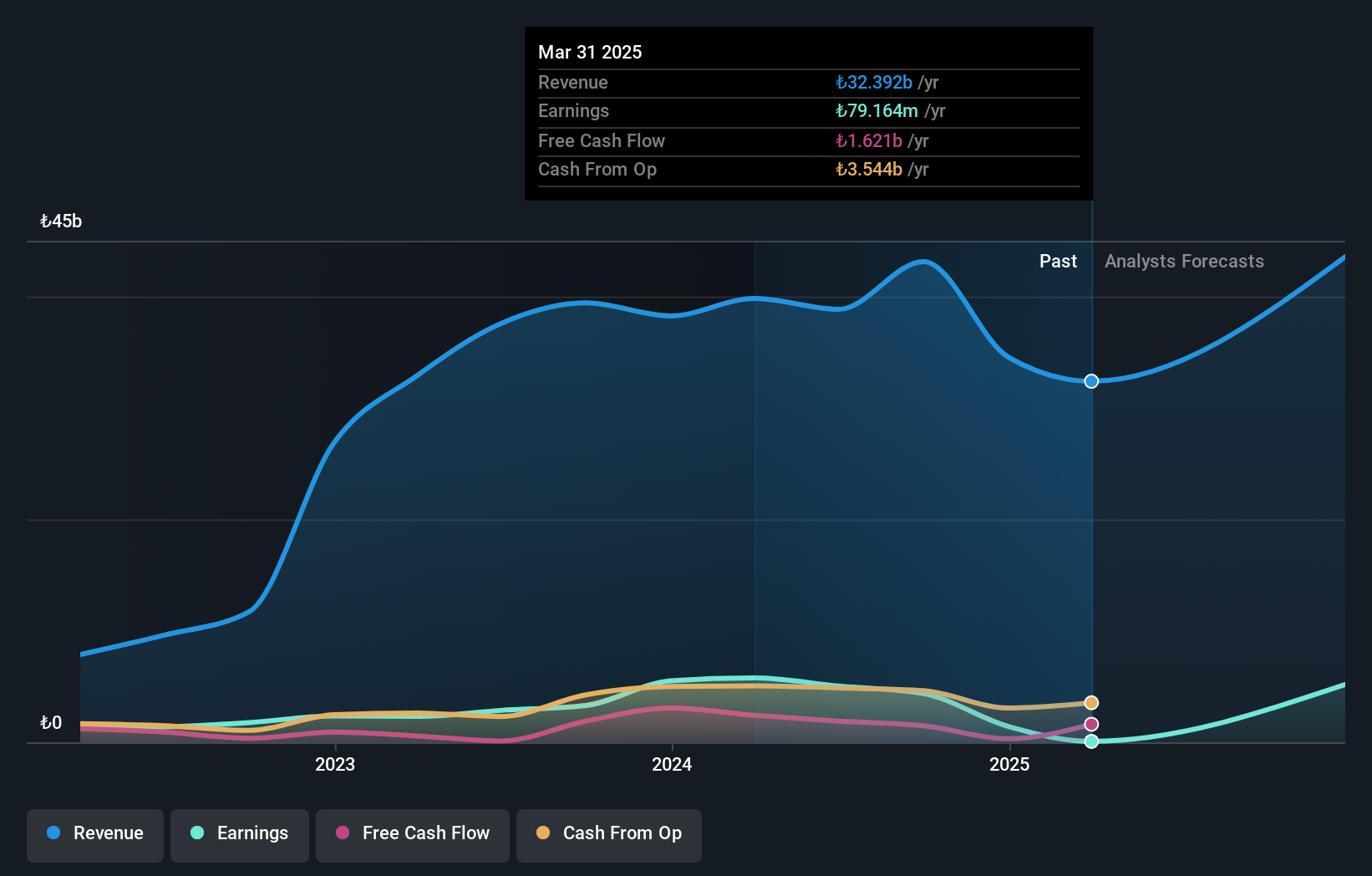

Brisa Bridgestone Sabanci Lastik Sanayi ve Ticaret (IBSE:BRISA)

Simply Wall St Value Rating: ★★★★★★

Overview: Brisa Bridgestone Sabanci Lastik Sanayi ve Ticaret A.S. is a leading tire manufacturing company with a market capitalization of TRY26.78 billion, focusing on producing and distributing vehicle tires.

Operations: Brisa generates revenue primarily from vehicle tires, amounting to TRY24.87 billion. The company's financial performance is highlighted by its net profit margin trends over recent periods.

Brisa Bridgestone Sabanci, a notable player in the tire industry, has shown a significant reduction in its debt to equity ratio from 351.5% to 81.5% over five years, reflecting improved financial health. Despite reporting a net loss of TRY 307 million for Q3 2024 compared to net income of TRY 704 million the previous year, its earnings have grown at an impressive average rate of 53.7% annually over the past five years. The company's price-to-earnings ratio stands at an attractive 8.8x against the market's 15.7x, suggesting potential undervaluation despite recent challenges in sales and profitability.

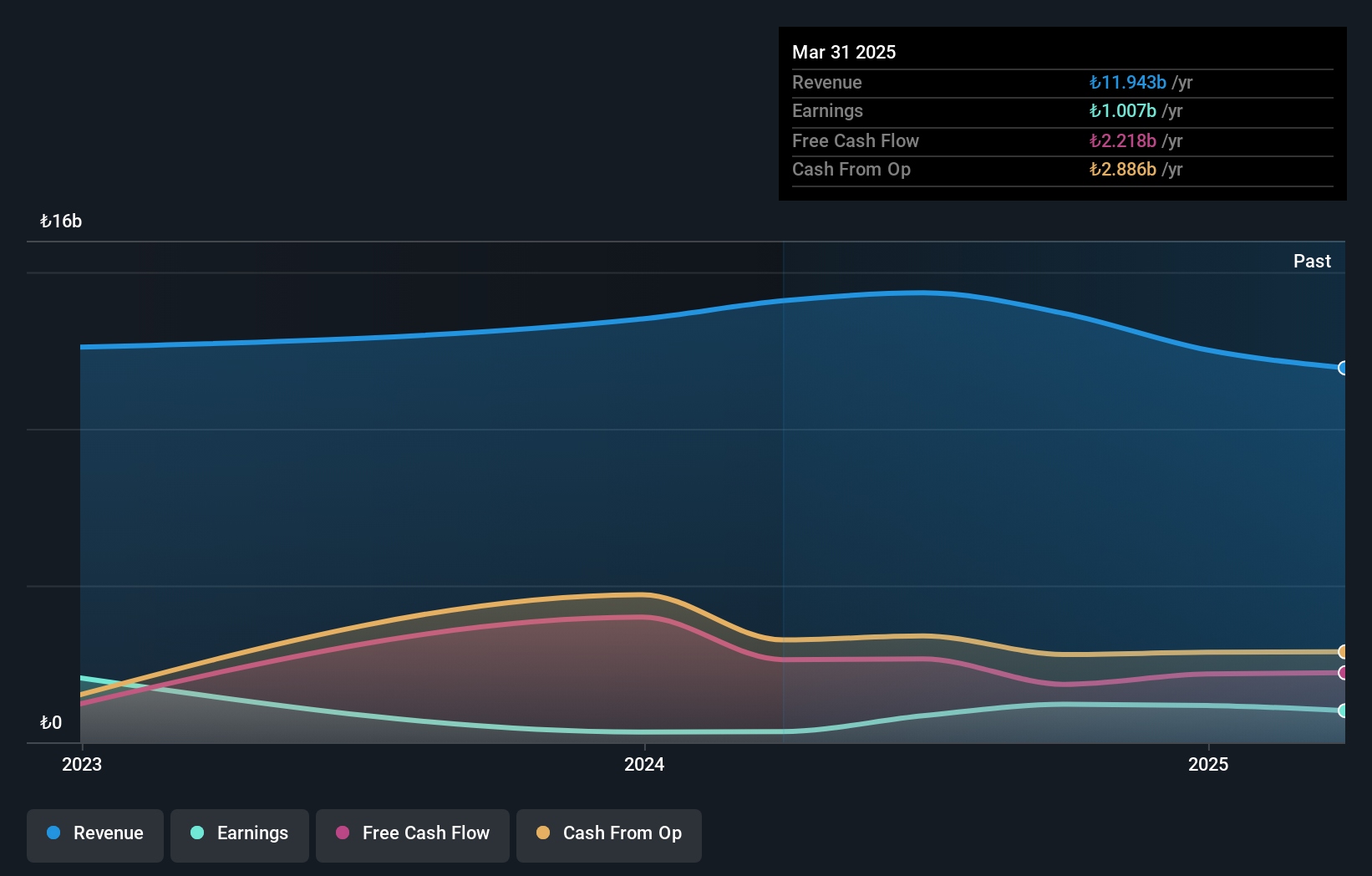

Lila Kagit Sanayi Ve Ticaret (IBSE:LILAK)

Simply Wall St Value Rating: ★★★★★☆

Overview: Lila Kagit Sanayi Ve Ticaret A.S. is a company that produces and sells roll papers primarily in Turkey, with a market capitalization of TRY14.93 billion.

Operations: Lila Kagit generates revenue primarily from its Paper & Paper Products segment, amounting to TRY8.75 billion. The company's gross profit margin is a notable aspect of its financial performance.

Lila Kagit, a small cap player in the household products sector, showcases notable financial resilience. Despite a 14% drop in revenue over the past year, earnings surged by 57%, outpacing industry growth of 23.8%. The company reported TRY 351 million net income for Q3 2024 against a TRY 14.53 million loss last year, reflecting improved profitability with basic earnings per share rising to TRY 0.59 from a loss of TRY 0.03 per share. With its price-to-earnings ratio at an attractive level of 13.9x compared to the market's average and more cash than debt, Lila Kagit seems well-positioned financially amidst challenges.

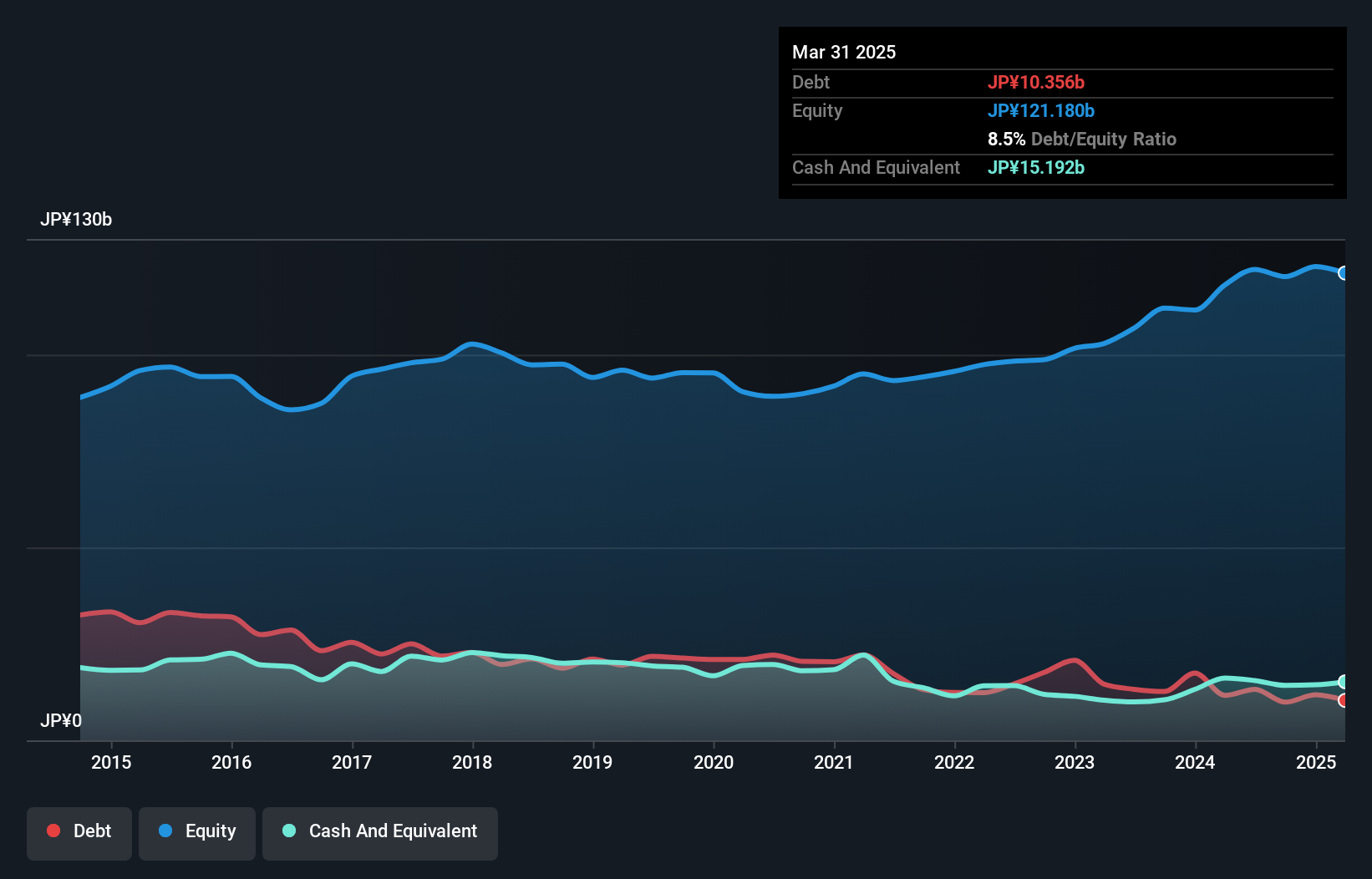

Kurabo Industries (TSE:3106)

Simply Wall St Value Rating: ★★★★★★

Overview: Kurabo Industries Ltd. operates in textile, chemical, technology, food and service, and real estate sectors both in Japan and internationally with a market cap of ¥99.71 billion.

Operations: Kurabo Industries generates revenue through its diversified operations in textiles, chemicals, technology, food and service, and real estate sectors. The company has a market capitalization of ¥99.71 billion.

Kurabo Industries, a notable player in its sector, is trading at 51.4% below its estimated fair value, suggesting potential undervaluation. Over the past year, earnings have surged by 60.1%, outpacing the luxury industry average of 13.1%. The company's debt-to-equity ratio has improved significantly from 22.4% to 8.2% over five years, highlighting effective debt management strategies. Recent activities include a share repurchase program aimed at enhancing shareholder returns and capital efficiency with plans to buy back up to 7.34% of issued shares for ¥6 billion (US$40 million). Additionally, dividends were increased to JPY 60 per share this quarter from JPY 40 last year, reflecting strong financial health and commitment to shareholder value enhancement.

Key Takeaways

- Dive into all 4627 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kurabo Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3106

Kurabo Industries

Engages in textile, chemical, technology, food and service, and real estate businesses in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor